There are few financial anxieties as sharp as expecting a direct deposit that never arrives. It’s like a pizza delivery that’s an hour late. You refresh your bank app every 10 minutes. Your stomach tightens. You’re calculating which bills you can delay if this doesn’t hit by 5 PM.

You start to get concerned.

Why Hasn’t My Direct Deposit Gone Through Yet?

Why Is My Direct Deposit Late?

When your rent check is due tomorrow and your car payment auto-draft is set for tonight, that anxiety escalates fast. You call HR. They put you on hold. You start googling “overdraft protection” and “payday loans.”

As a financial planner for over 25 years, I’ve fielded this frantic call more times than I can count. The good news: in 99% of cases, the money isn’t lost. It’s sitting in a queue at your employer’s bank (the ODFI, or Originating Depository Financial Institution), waiting for the next ACH processing window, or it’s already been transmitted to the Federal Reserve but hasn’t yet posted to your bank (the RDFI, or Receiving Depository Financial Institution). What’s stuck can be unstuck.

The key is knowing exactly who to call and what to say.

This is not just a list of reasons your deposit might be late. This is a prioritized, step-by-step action plan to give you control. Let’s get your money where it belongs.

Key Takeaways Ahead

Your 3-Step Action Plan When Your Direct Deposit is Late Michael Ryan Money P.A.T. Protocol™

Over my career, I developed a simple sequence for clients to follow that cuts through the panic and gets answers.

I call it my P.A.T. Protocol™: Paystub, Administrator, Trace.

1. Paystub: Be Your Own Detective

Before you call anyone, investigate for 60 seconds. Pull up your pay stub. Is the net pay amount correct? Is the pay date today?

This step alone once solved a “late” deposit for a client in mid-2024. He discovered his bonus was paid separately, changing the net amount and causing confusion.

Also, log into your bank app and confirm there are no “pending” deposits.

2. Administrator (HR/Payroll): Make the Critical Call

Your employer initiates the payment, so they have the most information. Do not just ask, “Where’s my money?”

💡 Michael Ryan Money Tip

When you call HR, use this exact phrase: “I’m calling to confirm the settlement date for the most recent payroll batch and to request the ACH trace number for my transaction.” That trace number is the golden ticket; it’s the FedEx tracking number for your money within the banking system.

3. Trace (Your Bank): The Final Step

Only call your bank if Step 2 confirms the deposit was sent correctly.

My contrarian advice: Don’t call the main customer service line. Call your local branch and ask for the branch manager. They often have more agency to track down a payment internally, especially if you provide them with the ACH trace number.

Why Hasn’t My Direct Deposit Gone Through Yet? Anatomy of a Digital Traffic Jam

Your deposit travels through the Automated Clearing House (ACH) network, a batch processing system governed by NACHA rules. Think of it like airport security: your money doesn’t fly direct. It queues at your employer’s bank, gets bundled with thousands of other transactions, then moves through Federal Reserve processing windows (1 AM, 1 PM, 5 PM ET daily). A delay means your payment missed a processing window or got held up in one of these batches. Here are the most common bottlenecks:

- The Holiday Hangover:

The ACH network sleeps on weekends and Federal Reserve holidays.

As of December 2025, FedNow (the Federal Reserve’s instant payment system launched in 2023) is still in limited adoption. Only 700+ financial institutions participate, covering just 13% of U.S. deposit accounts. Most employers still batch payroll through ACH because it’s cheaper ($0.03 per transaction vs. FedNow’s $0.045). Until FedNow reaches critical mass, weekend and Federal Reserve holiday delays remain standard. - The “Cutoff Time” Calamity:

Every employer’s bank has a cutoff time (e.g., 5 PM) to submit the payroll file. I had a client whose pay was always a day late because his company’s bookkeeper, working on the West Coast, consistently submitted the file two hours after the East Coast bank’s cutoff. - The Single-Digit Disaster:

One wrong digit in the account or bank routing number on your direct deposit authorization form sends your money into limbo. It will eventually bounce back to your employer, but this “reclamation” process can take days. Need help finding those numbers?

- Feel free to also read my recent article on How Long Does It Take For a Check To Clear?

- Also, check our guide on how to read a check.

When a Direct Deposit Delay is More Serious: Employer Issues and Your Legal Rights

What if your employer is intentionally paying you late? That’s not a banking problem; it’s a legal battle waiting to happen. The Fair Labor Standards Act (FLSA) is a federal law that requires employers to pay employees on their regularly scheduled payday.

📉 Bad Advice

Don’t just wait and hope your employer will “figure it out.” If you suspect your employer is having financial trouble or is intentionally withholding wages, you must act to protect yourself. Document every communication in writing. For more details on your rights, read our full article on what to do when you don’t receive a paycheck.

If your employer is consistently late with your payroll direct deposit, you can file a wage complaint with the U.S. Department of Labor.

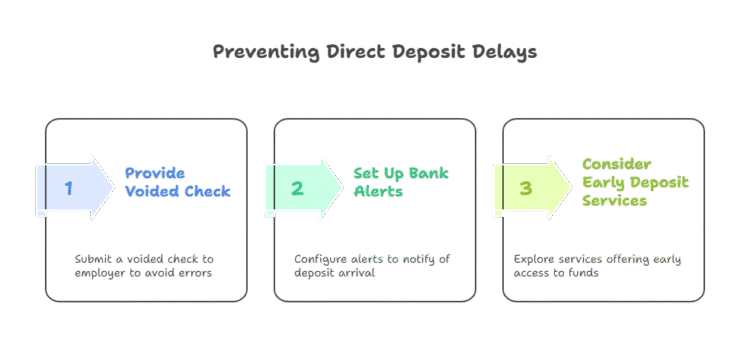

How to Prevent Future Direct Deposit Delays

Set up bank alerts. Set up automatic transfers. Set yourself up for financial peace.

- Use a Voided Check: When setting up direct deposit, provide a voided check to your employer to eliminate typos.

- Set Up Bank Alerts: Most banks allow you to set up a text or email alert that notifies you the moment a deposit hits your account.

- Consider Early Direct Deposit Services: Some modern financial institutions, like the one in our Chime Review, offer early direct deposit, making your funds available up to two days early.

Late Direct Deposit Frequently Asked Questions

Can a bank hold a direct deposit?

Yes, but it’s rare for typical payroll. Under federal law, banks can place holds on deposits, but payroll direct deposits are generally required to be made available on the next business day. Holds are more common for new accounts, large or unusual deposits, or if the account has a history of being overdrawn.

What is the cutoff time for direct deposits?

This refers to your *employer’s* bank cutoff time. Most banks have an evening cutoff (e.g., 5 PM PT) for processing ACH files for the next day. If your employer submits the payroll file after that time, your deposit will be delayed by at least one business day.

I’m a new employee. Why is my first direct deposit late?

This is very common. Many payroll systems run a “pre-note” or test transaction on new accounts, which can take several days. Because of this, many companies issue the first paycheck as a paper check to avoid delays. Always confirm the process for your first paycheck with your HR department.

Final Word From Michael Ryan Money

A late direct deposit is stressful, but it’s almost always a solvable problem. By following the P.A.T. Protocol™ – checking your own info, contacting your employer, and then contacting your bank – you can move from a state of panic to a state of control.

Remember to be specific, use the right terminology, and know your rights.

Explore next steps like how holidays, payroll errors, or incorrect account info affect payment timing. Now, try searching for: direct deposit on holidays, employer payroll processing delays, or fixing bank info mistakes.

What to Read Next

Now that you’ve tackled your late deposit, let’s talk about building a buffer so a small delay doesn’t derail your finances. The best defense is a good offense.

➡️ Read Our Guide: How to Build an Emergency Fund and Why It’s Your #1 Priority

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.