For retirees who are charitably inclined, there is no single greater tool for tax and Medicare premium savings than the Qualified Charitable Distribution (QCD). Yet, it remains one of the most misunderstood and underutilized strategies in retirement finance.

This is what I saw in nearly 3 decades advising people. Too many retirees continue to write checks to their favorite charities while simultaneously taking a taxable Required Minimum Distribution (RMD) from their IRA. Not realizing they are leaving thousands of dollars on the table.

As a financial planner, I saw this one simple shift in giving strategy, from the checkbook to the IRA, save my clients more money than any complex investment maneuver. It’s not just a way to get a tax deduction for your donation; it’s a way to make the donation itself practically pay for itself by eliminating a cascade of other taxes and penalties.

This is especially true when it comes to IRMAA. A well-timed QCD can be your secret weapon to surgically reduce your income and prevent yourself from falling over the costly IRMAA “cliffs.” This guide will show you the mechanics, the math, and the massive opportunity you have every year after age 70½.

⚡ Key Takeaways

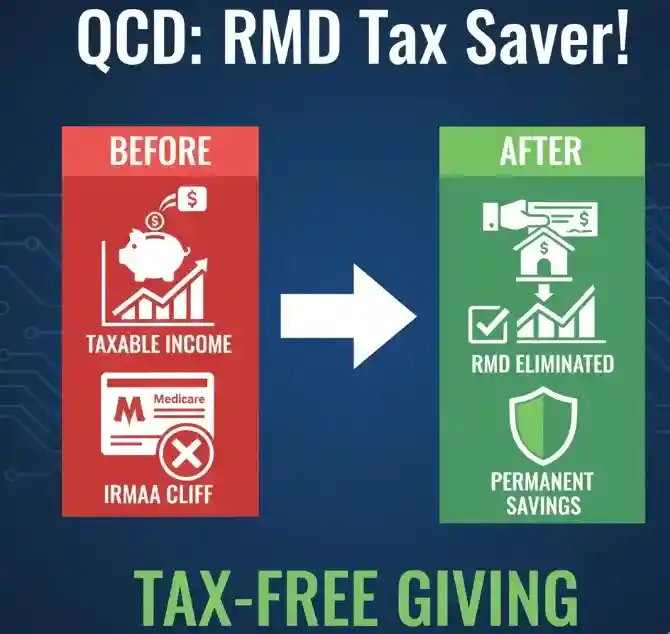

- A QCD is a Direct Transfer: A QCD is a distribution paid directly from your IRA to a qualified charity. Because you never personally receive the money, it is excluded from your income, which is far more powerful than a standard tax deduction.

- It Satisfies Your RMD: For those 73 and older, a QCD counts dollar-for-dollar toward your Required Minimum Distribution for the year, allowing you to fulfill your mandatory withdrawal obligation without adding a penny to your taxable income.

- It’s a MAGI Reduction Tool: By excluding the distribution from your income, a QCD directly lowers your Adjusted Gross Income (AGI), which in turn lowers your Modified Adjusted Gross Income (MAGI)—the number used to calculate your IRMAA surcharges.

- The ROI Can Be Staggering: When a QCD helps you avoid an IRMAA cliff, the combined savings from income tax and Medicare premiums can represent a 40-50%+ return on the first dollars you give, effectively making your donation government-subsidized.

Key Takeaways Ahead

How a QCD Works: The Mechanics of a Powerful Strategy

Understanding a QCD is simple. Instead of taking your RMD, depositing it in your bank account, and then writing a check to charity, you instruct your IRA custodian (like Fidelity, Schwab, or Vanguard) to send the money directly to the charity on your behalf.

For a full breakdown of RMDs themselves, see our guide on the new RMD tables.

The QCD rules are straightforward:

- You must be age 70½ or older on the day of the distribution.

- The funds must come from a pre-tax IRA (Traditional, Rollover, SEP, or SIMPLE). 401(k)s are not eligible.

- The distribution must go directly to a qualified 501(c)(3) charity. Donor-advised funds and private foundations are not eligible. [IRS.gov]

- The maximum you can transfer via QCD annually is $111,000 per person for 2026 (this amount is now indexed to inflation thanks to the SECURE 2.0 Act).

💡 Michael Ryan Money Tip

The distinction between the QCD eligibility age (70½) and the RMD start age (currently 73) is a critical planning point. You have a multi-year window to make tax-free charitable gifts and reduce your IRA balance before your RMDs even begin, a strategy that pays massive dividends later.

The Real Power: QCD as an “Above-the-Line” Deduction

When you donate to charity with cash, you get a tax deduction *if* you itemize. This is a “below-the-line” deduction, meaning it only reduces your taxable income after your AGI has already been calculated. But a QCD is an “above-the-line” *exclusion*. The money never even shows up in your AGI in the first place. This is a far more powerful benefit because your AGI is the basis for many other financial hurdles in retirement, including the IRMAA cliffs.

💡 Master Your RMDs & Eliminate IRMAA

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Learn to use QCDs like a pro.

- → Avoid common RMD & IRMAA mistakes.

- → Get proven tax-saving retirement strategies.

Get insights on QCDs & IRMAA delivered every week — before the costly mistakes happen.

📬 No spam. Unsubscribe.

The ROI of a QCD: Calculating Your True Savings

When you are on the cusp of an IRMAA bracket, a QCD provides a spectacular return on investment. Let’s calculate the true net cost of that $10,000 donation for the couple in the story.

- Federal Income Tax Savings: Their RMD income is in the 22% tax bracket. By excluding $10,000 from income, they saved $2,200 in federal taxes.

- State Income Tax Savings: Let’s assume a 5% state tax rate. They saved an additional $500.

- IRMAA Premium Savings: By getting back under the threshold, they saved $974.40 in Medicare surcharges (Part B only for 2026).

Total Savings: $2,200 + $500 + $974.40 = $3,674.40.

Net Cost of their $10,000 Donation: $10,000 – $3,674.40 = $6,325.60.

Their $10,000 gift to a cause they love only cost them $6,325.60 out of pocket. That’s a 37% return on their charitable “investment.” This is a level of tax efficiency you simply cannot achieve any other way. For more ways to lower your Medicare costs, see our master guide on how to avoid IRMAA.

Read Deeper on Retirement Tax Planning

- What to Do With RMDs You Don’t Need – Explore other strategic options for your required distributions beyond just spending them.

- 7 IRMAA Mistakes Even CPAs Can Make – Discover the common blind spots that can lead to unintentional Medicare surcharges.

- Fidelity’s Guide to QCDs – Read another authoritative perspective on the rules and benefits of QCDs from a major custodian.

Frequent Reader Questions About QCDs and IRMAA

Can I take the RMD myself and then give it to charity for the same benefit?

No. This is the most common mistake. If the money from your IRA touches your personal bank account, it is considered a taxable distribution and will be included in your AGI. The transfer MUST go directly from your IRA custodian to the charity to qualify as a QCD.

Can my spouse and I both do a QCD?

Yes. If you both have your own IRAs and are both over age 70½, you can each make a QCD up to the annual limit of $111,000 (for 2026). This allows a married couple to exclude up to $222,000 from their income if they are charitably inclined.

How do I prove I did a QCD to the IRS?

Your IRA custodian will send you a Form 1099-R for the total amount distributed from your IRA, and it will not distinguish between the QCD and other withdrawals. It is your responsibility to report the total distribution on your tax return and then subtract the QCD amount, noting “QCD” next to the line item. You must also get a written acknowledgment of the donation from the charity.

Your Next Steps: QCD For IRMAA or Not?

The Qualified Charitable Distribution (QCD) is not just a kind gesture; it is the most tax-efficient method available for retirees to give charitably while simultaneously managing their RMDs and aggressively reducing their tax liability. This simple strategic shift can save thousands in income tax and may permanently eliminate Medicare premium surcharges.

Before your next charitable donation, take these steps:

- Check your IRA custodian’s QCD instructions (Fidelity, Schwab, etc.) and

- Use my IRMAA calculator to project where your MAGI will land this year.

- Remember, the transfer must go directly from the IRA to the charity.

Join thousands of readers just like you for weekly money wins. Here’s how to act this week: Take action now to implement this simple shift and start turning your charitable giving into a powerful, government-subsidized tax-saving tool.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.