Let me start with this: I have immense respect for Certified Public Accountants. A great CPA is a master of the tax code, a historian of your financial past. As well as an essential partner in ensuring you pay what you owe, and not a penny more. But the accountants primary mission is, by definition, retrospective. They are experts at optimizing your tax situation for the year that just ended.

And that is precisely where the IRMAA problem begins. And the common IRMAA mistakes I have seen people make over the years.

As a financial planner for almost 3 decades, I’ve seen the painful aftermath of this professional blind spot time and again. A client comes in, thrilled that their CPA saved them $5,000 on their tax bill. Only to get a letter from the Social Security Administration two years later informing them that their Medicare premiums have increased by $3,000 or more due to IRMAA surcharges.

They won the battle but lost the war.

This article covers the most common IRMAA mistakes to avoid. Seven practical errors that can raise your Medicare premiums two years from now, and how to fix them. IRMAA isn’t a tax problem; IRMAA is a future-income problem. And requires forward-looking planning, not just historical reporting.

This guide highlights the seven common IRMAA mistakes that can happen when your tax strategy and your retirement income strategy aren’t speaking the same language. This isn’t about blaming your CPA; it’s about empowering you to ask the right questions to bridge the gap.

Key Takeaways Ahead

⚡ Key Takeaways

- Tax Prep is Reactive, IRMAA Planning is Proactive: Your CPA’s job is to accurately report last year’s income. An IRMAA planner’s job is to strategically manage this year’s income to protect your premiums two years from now.

- Small Income Items Have a Big Impact: Seemingly minor income sources like tax-exempt interest from municipal bonds or state tax refunds are invisible to your income tax bill but are added back in for the IRMAA calculation.

- A “Good Tax Move” Can Be a Bad IRMAA Move: Taking a large capital gain or doing a big Roth conversion to take advantage of a tax bracket might feel smart, but it can easily create an “income spike” that triggers years of surcharges.

- Missed Opportunities Are Costly: Failing to proactively use tools like Qualified Charitable Distributions (QCDs) before year-end is a common oversight that leaves retirees paying both higher taxes and higher premiums.

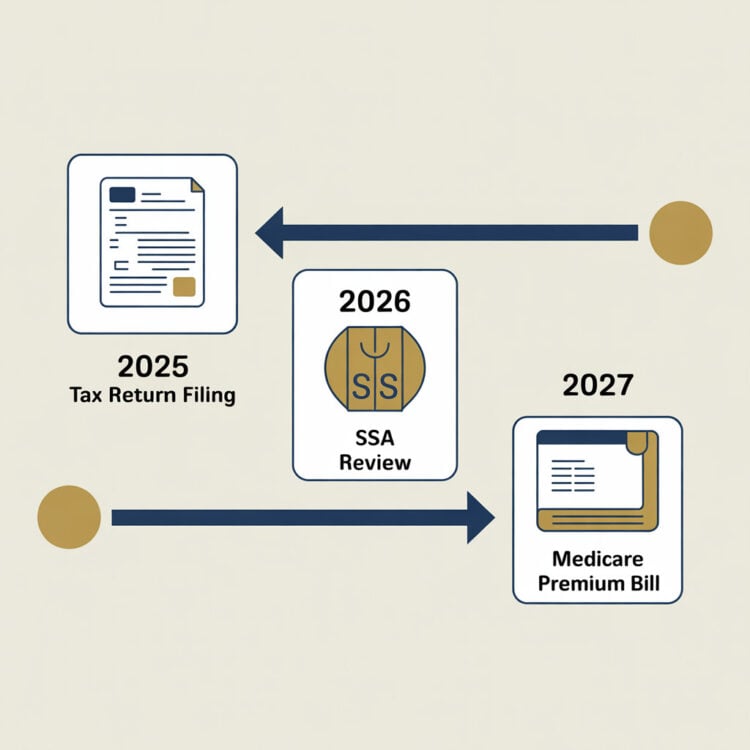

The Core Problem: The Two-Year Gap Between Tax Filing and Premiums

The entire IRMAA system is built on a two-year delay. Your 2026 Medicare premiums are set by the Modified Adjusted Gross Income (MAGI) on the tax return you file in early 2025 for the 2024 tax year. By the time your CPA is preparing that return, the “damage” is already done. The income has been earned, the transactions are complete, and the MAGI is set in stone.

For 2026, the standard Medicare Part B premium is $202.90 per month. However, if your 2024 MAGI exceeded $109,000 (single filers) or $218,000 (married filing jointly), you’ll pay IRMAA surcharges on top of this base amount. The total monthly Part B premium for high-income beneficiaries ranges from $284.10 to $689.90 depending on income level. Source: CMS 2026 Medicare Parts A & B Premiums and DeductiblesMAGI for IRMAA purposes is your Adjusted Gross Income (AGI) plus tax-exempt interest (SSA POMS HI 01101.010)..

A tax preparer can’t change the past. This is why you, as the CEO of your retirement, must understand the forward-looking implications of your financial decisions throughout the year.

IRMAA Mistakes to Avoid; A Quick Checklist

- Model your MAGI before making any major financial moves (like selling a property or taking a large withdrawal).

- Use Qualified Charitable Distributions (QCDs) to satisfy your RMDs if you are over age 70½ and charitably inclined.

- If you plan to do a large Roth conversion, consider splitting it across multiple tax years to stay under the IRMAA cliffs.

💡 Avoid Costly Tax Blind Spots & Protect Your Retirement

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Sidestep common IRMAA triggers.

- → Learn forward-looking tax strategies.

- → Get planner insights your CPA might miss.

Get planner insights on IRMAA delivered each week — the ones costing you the most.

📬 No spam. Unsubscribe.

Mistake #1: Ignoring “Invisible” Income Like Tax-Exempt Interest

This is the classic IRMAA “gotcha.” You and your CPA might have structured a bond portfolio to generate tax-exempt income from municipal bonds. It feels great to see that income hit your account without a tax bill attached. The problem? For the IRMAA calculation, that tax-exempt interest is added back to your Adjusted Gross Income (AGI). It’s a key part of your MAGI.

📊 Quick Stat

Your Modified Adjusted Gross Income (MAGI) for IRMAA purposes is your AGI + Tax-Exempt Interest + certain foreign earned income. That middle piece is the one that surprises nearly everyone. For a full breakdown of the specific income cliffs, see our complete guide to the current year IRMAA brackets.

Mistake #2: Missing the Proactive QCD Opportunity

A Qualified Charitable Distribution (QCD) allows IRA owners aged 70½ and older to donate up to $111,000 (for 2026) directly to charity, while RMDs now generally begin at age 73.(IRS guidance) The beauty of a QCD is that the distribution counts toward your Required Minimum Distribution (RMD) but is excluded from your taxable income. A CPA preparing your taxes in March of next year can only report what you did.

They can’t go back in time and tell you to make a QCD before the December 31st deadline. For official rules, see the IRS guidance on QCDs.

The result: The client takes their full RMD as taxable income, increasing their MAGI and potentially triggering IRMAA, when they could have satisfied their RMD tax-free and stayed under the threshold.

💡 Avoid Costly Tax Blind Spots & Protect Your Retirement

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Sidestep common IRMAA triggers.

- → Learn forward-looking tax strategies.

- → Get planner insights your CPA might miss.

Get planner insights on IRMAA delivered each week — the ones costing you the most.

📬 No spam. Unsubscribe.

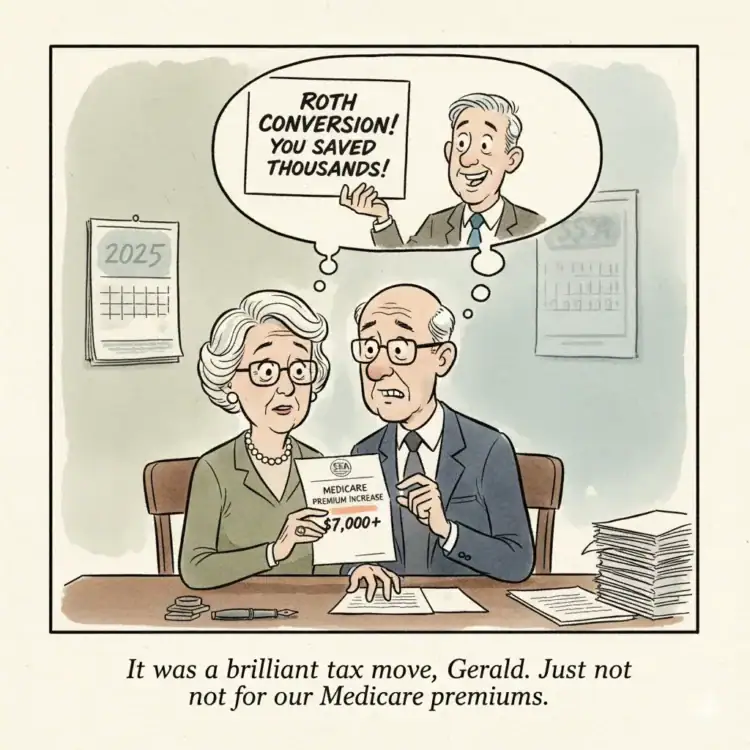

Mistake #3: Poor Roth Conversion Timing

Roth conversions are a brilliant long-term tax strategy, but they are pure rocket fuel for your MAGI in the year of the conversion. A tax-focused professional might see you have room in the 22% or 24% tax bracket and advise you to “fill it up” with a large conversion.

Mistake #4: Triggering a “Capital Gains Bomb”

Similar to a Roth conversion, a large capital gain from selling a rental property, a business, or a highly appreciated stock can be a major IRMAA trigger. A CPA might focus on strategies like tax-loss harvesting to reduce the net gain, which is a great tax-reduction move. But they may not run the projection to see if the remaining gain.

Even if taxed at lower long-term capital gains rates, is enough to cause a significant one-time income spike that triggers IRMAA two years from now.

Mistake #5: Misunderstanding the IRMAA Appeal Process

When a client experiences a true “life-changing event” like retirement, divorce, or death of a spouse, they have the right to appeal their IRMAA determination. However, many tax preparers are not specialists in the Social Security appeals process. They might not know to proactively advise a client to file Form SSA-44, or they may be unsure of what documentation is required.

For eligibility and forms, see the Social Security Administration’s guidance on IRMAA appeals (SSA.gov).

⚠️ Myth Busted

A common mistake is thinking you can appeal IRMAA because of a large, one-time income event like a Roth conversion. This is incorrect. The SSA only recognizes a specific list of life-changing events. A voluntary conversion or investment sale does not qualify. This is why proactive planning is your only defense. [cite: SSA.gov]

Mistake #6: Forgetting About State Tax Refunds

This is another minor detail that can have a surprising impact. If you itemized your deductions on your federal return and deducted your state income taxes, any state tax refund you receive in the following year is considered taxable income by the IRS.

And yes, it gets added to your MAGI calculation for IRMAA. While rarely a huge amount, it can be just enough to push someone over the edge of an IRMAA bracket. This is especially relevant for retirees considering a move to states with no income tax.

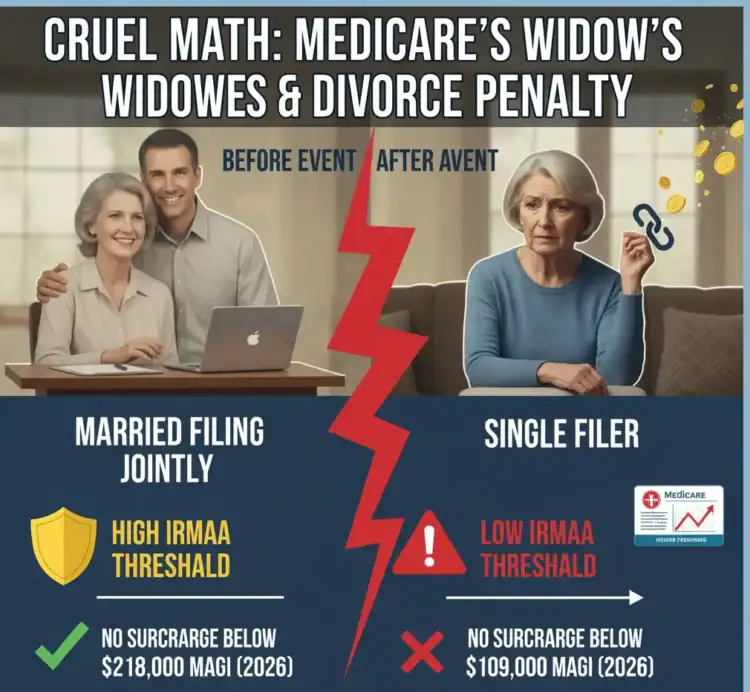

Mistake #7: Overlooking Spousal Income & The “Widow’s Penalty”

Tax planning for a married couple is often done from a household perspective. But IRMAA can get complicated when spouses have vastly different incomes or when one spouse passes away.

A CPA might not be focused on the devastating impact of the “Widow’s Penalty,” where a surviving spouse is forced onto the ‘Single’ filer status with much lower IRMAA thresholds, causing their premiums to spike unexpectedly. Understanding your rights to Social Security survivor benefits is a critical part of this planning.

Proactive solutions to mitigate this penalty include:

- Proactively funding a Roth IRA while both spouses are alive to create an income source that is MAGI-free for the surviving spouse.

- Utilize a Qualified Longevity Annuity Contract (QLAC) to delay RMDs until age 85, keeping income lower for the surviving spouse when the penalty hits hardest.

💡 Avoid Costly Tax Blind Spots & Protect Your Retirement

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Sidestep common IRMAA triggers.

- → Learn forward-looking tax strategies.

- → Get planner insights your CPA might miss.

Get planner insights on IRMAA delivered each week — the ones costing you the most.

📬 No spam. Unsubscribe.

Frequent Reader Questions

What are the most common IRMAA mistakes to avoid?

The most common IRMAA mistakes to avoid include: ignoring tax-exempt interest, doing large Roth conversions in a single year, missing QCD opportunities, selling appreciated assets without modeling MAGI, and underestimating spousal or survivor effects. Model each major transaction against IRMAA thresholds two years out.

Is my CPA responsible for my IRMAA surcharges?

No. A CPA’s legal responsibility is to prepare an accurate tax return based on the financial events that have already occurred. Their role is generally not defined as a forward-looking financial planner who projects the future consequences of your income on government benefits.

Can my CPA file an IRMAA appeal for me?

Yes, a CPA can help you complete and file Form SSA-44, especially in gathering the necessary proof of income reduction. However, you are the one who must sign the form and are ultimately responsible for its accuracy.

When should I talk to a financial planner versus a CPA about IRMAA?

Talk to a financial planner during the year to create proactive strategies for managing your income (like Roth conversions and withdrawal plans). Talk to your CPA at tax time to ensure all income is reported correctly and to help you document any life-changing events that may have occurred.

Master Your IRMAA Strategy

- Learn the core strategies to avoid surcharges – Go beyond the appeal and discover proactive ways to manage your income and keep your Medicare premiums low for good.

- Understand the IRMAA appeal process – If you’ve already had a life-changing event, this guide walks you through the steps to file Form SSA-44.

- Review the IRS Guide for Seniors – See the official IRS rules on what constitutes taxable income for retirees in Publication 554.

How to Work With Your CPA to Avoid These Mistakes

The solution isn’t to fire your CPA. It’s to become an informed client who bridges the gap between tax prep and financial planning.

- Bring IRMAA Up Proactively: Before year-end, ask your CPA: “Can we project my MAGI for this year and see how it might impact my Medicare premiums two years from now?”

- Discuss Major Transactions in Advance: Never sell a major asset or do a large Roth conversion without modeling the IRMAA impact first. Ask: “How will this sale affect my MAGI?”

- Confirm Charitable Giving Strategy: If you are over 70½ and charitably inclined, specifically ask your CPA about using a Qualified Charitable Distribution (QCD) from your IRA, or if an HSA distribution for qualified expenses could be used to lower your taxable income.

- Share Your Full Financial Picture: Make sure your CPA is aware of all sources of income, including things that might not be on your W-2, like tax-exempt interest.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.