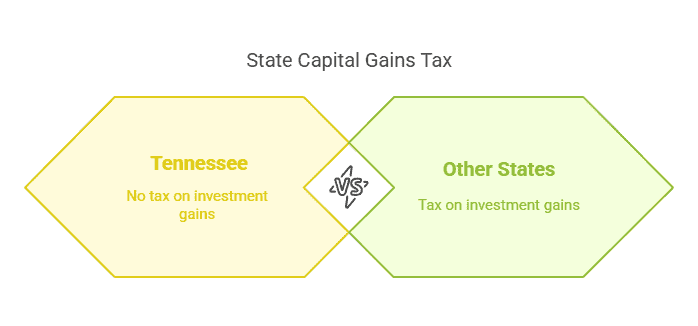

On January 1, 2021, Tennessee officially eliminated the TN Hall Income Tax, which previously taxed certain investment income. This move positioned Tennessee among the few states without any form of personal income tax, including taxes on capital gains.

Honestly, that’s a pretty big deal – a state where you get to keep every penny of your investment gains at the state level? Yeah, that’s something worth paying attention to.

I had a client in Chattanooga who sold her investment property in late 2025, and she was genuinely shocked when she realized that at the state level, she owed nothing. However, it’s essential to stay on top of federal tax obligations – the IRS still wants its cut.

Estimate Your Federal Capital Gains Tax (as a TN Resident)

While Tennessee boasts no state capital gains tax on your investments or primary home sale (for tax years 2021 and beyond!), federal obligations remain.

Use this estimator to get a ballpark of your current federal capital gains bill

Federal Capital Gains Tax Estimator (Tennessee Residents)

Step 1: What are you selling?

The Tool Gave You Answers. The Newsletter Gives You Moves.

IMPORTANT DISCLAIMER: This calculator provides an estimate for informational purposes only, using 2026 federal tax rates. Tennessee has zero state capital gains tax (as of 2021). This calculator does NOT account for: wash sale rules, alternative minimum tax, state/local taxes, NIIT calculations, or other complex situations. Always consult a qualified tax professional before making financial decisions. Tax brackets and rates change annually. Last updated: February 16, 2026.

This tool provides a rough estimate based on current federal rates and the info you enter. Look, tax laws change, and your individual situation – other income, deductions, credits – will affect your actual tax liability.

For precise calculations, specific advice on strategies like tax-loss harvesting, or understanding the Net Investment Income Tax (NIIT) in detail, always consult with a qualified tax professional. Understanding your federal tax liability is a key part of smart financial planning in Tennessee.

The Big News: Tennessee & State-Level Capital Gains Tax – What Changed?

Ever wonder why Tennessee suddenly became such a hotspot for investment income. Or why folks selling property here seem a bit more cheerful? One key piece of legislation flipped the switch. For years, Tennessee had something called the TN Hall Income Tax. This wasn’t a tax on all income, but it did hit some of their interest and dividend income.

Here’s what matters: the Hall income tax was fully repealed for tax years beginning on or after January 1, 2021. As the Tennessee Department of Revenue explains, Tennessee doesn’t have an individual income tax anymore, and the old Hall tax that hit interest and dividends? Gone. This repeal effectively shut down the last way the state could tax your investment gains.

For Tennessee Investors (Stocks, Bonds, Real Estate, Oh My!)

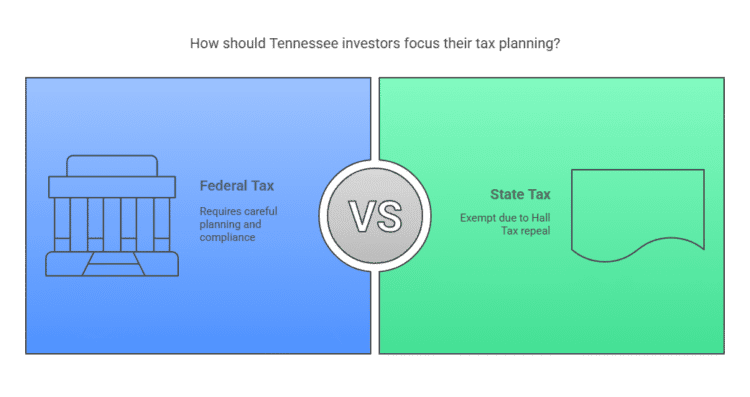

Building wealth through investments in Tennessee? Your state isn’t looking for a cut of the profits, but that means your federal game needs to be sharp. Just because you’re playing on a tax-friendly field doesn’t mean you can ignore the rulebook!

Mutual Fund Distributions: A Quick Note Post-Hall Tax

Used to get a state tax bill for those mutual fund ‘capital gains’ payouts? Good news on that front. Under the old Hall Tax rules, certain distributions from mutual funds that were classified as “capital gains” could be taxable at the state level.

However, with the Hall Tax repealed effective January 1, 2021, these types of distributions from mutual funds are now also exempt from Tennessee state tax for individuals (Tennessee Department of Revenue). Your focus for these, too, is solely on federal taxation.

Whether you’re into stocks, bonds, mutual funds, or real estate investing, your planning in Tennessee needs to be laser-focused on federal strategies.

So, No State Tax… But What About Uncle Sam? Understanding Federal Capital Gains Tax

Okay, so Nashville isn’t sending you a tax bill for your gains. Great! But does that mean you’re completely off the hook? Not so fast… This is where many people get tripped up. While Tennessee gives you a pass, the IRS still expects its share through federal capital gains tax.

Here’s the thing: federal rules still apply, and if you ignore them you’re setting yourself up for some unpleasant surprises come tax time.

A capital asset generally includes most things you own for personal use or investment, like stocks, bonds, your home, or investment properties. When you sell a capital asset for more than your adjusted basis, you have a capital gain.

One of my clients in Nashville delayed selling his appreciated stock by just two months, transitioning from a short-term to a long-term gain, and saved thousands in taxes. It’s a testament to how timing can be everything in tax planning.

Are you making the most of your holding periods? You can learn more about the basics of capital gains tax from a federal perspective on my site.

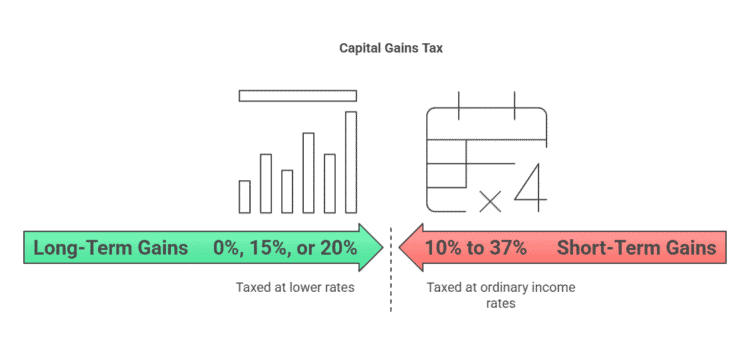

Long-Term vs. Short-Term Gains: Why Holding Periods Matter (Everywhere!)

Think patience doesn’t pay? When it comes to federal capital gains, waiting just one extra day can sometimes save you thousands on your tax bill. The IRS differentiates between:

- Long-Term Capital Gains:

Profit from assets you’ve held for more than one year. These are typically taxed at lower rates: 0%, 15%, or 20%, depending on your overall taxable income.

These brackets move each year with inflation, but for 2025-2026 most single filers in the middle-to-upper income ranges fall into the 15% bucket. (For the most current federal capital gains tax rates). - Short-Term Capital Gains:

Profit from assets you’ve held for one year or less. These are taxed at your ordinary income tax rates, which can range from 10% all the way up to 37%, depending on your income bracket.

The difference can be substantial. What if you sold stock A after 11 months versus 13 months? That small difference in holding period could shift a hefty tax bill from your higher ordinary income rate down to a more favorable long-term capital gains rate. This distinction is absolutely critical for investors everywhere, including Tennessee.

Selling Your Primary Residence in Tennessee

Tennessee homeowners can benefit significantly when selling their primary residence. Most homeowners are eligible for a significant federal exclusion on the capital gains from selling their primary residence. (HomeLight). If you’ve lived in your home for at least two of the past five years.

Here’s the deal:

- If you’re single, you can exclude up to $250,000 of gain.

- If you’re married filing jointly, you can exclude up to $500,000 of gain.

Combined with Tennessee’s lack of a state income tax, this can result in substantial savings. A couple from Knoxville sold their home in early 2025, realizing a $480,000 gain. Thanks to these provisions, they paid no capital gains tax at all. Not to Tennessee, and not to the feds. That’s what I call a sweet deal!

Is your home sale strategy aligned with these benIf you’re thinking about selling, make sure your strategy lines up with these rules. For more details, check out my guide on capital gains tax on home sales.efits? For more details, check out my guide on capital gains tax on home sales.

Historical Tennessee tax policy information

Investment Strategies for TenneInvestment Strategies for Tennessee Residents in 2026ssee Residents

Even without state taxes, federal taxes require careful planning. Remember, a penny saved from the IRS is a penny truly earned.

Consider these strategies:

- Tax-Loss Harvesting:

Offset gains with losses to reduce taxable income. This is a fundamental part of how to avoid paying capital gains tax at the federal level. - Strategic Holding Periods:

As we discussed, aim to hold appreciated assets for more than one year to qualify for those lower long-term capital gains rates. This can make a significant difference in your federal tax bill. - Timing Your Sales:

If you’re close to an income threshold that would bump you into a higher federal capital gains tax bracket (e.g., from 0% to 15%, or 15% to 20%), consider timing your sales across tax years to potentially stay in a lower bracket for some or all of your gains. - Charitable Donations:

Donating appreciated assets can provide deductions and avoid capital gains taxes. Many clients use donor advised funds for this. - Opportunity Zones:

Investing in designated opportunity zone areas can offer tax incentives (The Entrust Group often discusses various investment vehicles).

Relocating to Tennessee: Tax ImRelocating to Tennessee in 2026: Capital Gains Tax Implicationsplications

Moving to Tennessee can offer tax advantages, but timing is crucial. Ensure you establish residency before selling significant assets to avoid taxes from your previous state.

I had a client move from California in early 2025 and sell his business post-move – saved substantially on state taxes. This is particularly relevant for those with high net worth asset allocation considerations.

Conclusion: The Tennessee Takeaway on Capital Gains

So, what’s the bottom line for your bottom line when it comes to capital gains in Tennessee? It’s genuinely good news:So what does all this actually mean for you in Tennessee? Here’s the good news:

- State Relief: Tennessee does not have a state capital gains tax for individuals on the sale of investments or property, thanks to the Hall Tax repeal.

- Federal Focus: This means all your capital gains tax planning needs to center on federal rules, rates, and strategies.

- Homeowner Edge: For homeowners selling their primary residence, the generous federal exclusion combined with $0 state tax can mean keeping a very significant portion of your sale proceeds.

- Investor Strategies: Smart investors in Tennessee will use federal-level techniques like tax-loss harvesting, strategic holding periods, and charitable gifting of appreciated assets to minimize their overall tax bite.

Make sure your federal strategy is buttoned up. If you’re unsure about any of this, talk to a qualified financial advisor or tax professional who can help you navigate these rules.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.