For 30 years, you did everything right. As a federal employee you contributed diligently to your Thrift Savings Plan (TSP), you built up your FERS or CSRS pension. And you’ve counted on the promise of excellent health benefits through FEHB. But now, as you approach retirement, you’re about to collide with a little-known tax torpedo called IRMAA. And your federal benefits are sitting directly in its path.

As a financial planner for almost 30 years, I’ve seen countless federal employees get blindsided by this. They make a smart-sounding move with their TSP, only to receive a shocking letter from the Social Security Administration two years later informing them their Medicare premiums have doubled or tripled. This isn’t a penalty for being a successful saver; it’s a penalty for not understanding how the federal retirement system and Medicare interact.

This guide will give you the playbook that’s missing from standard government pamphlets. We’ll break down exactly how your TSP withdrawals trigger IRMAA, how to make the critical FEHB vs. Medicare decision, and the strategies you can use to protect your hard-earned retirement income.

Key Takeaways Ahead

⚡ Key Takeaways

- TSP Withdrawals Are a Tax Time Bomb: Every dollar you pull from your traditional TSP is taxed as ordinary income. This income directly increases your Modified Adjusted Gross Income (MAGI), which is what the SSA uses to calculate IRMAA surcharges two years later.

- Coordination is Non-Negotiable: Your decisions about TSP withdrawals, FEHB coverage, and when to enroll in Medicare Part B are not separate choices. They are one interconnected financial puzzle that must be solved together to avoid costly mistakes.

- The “Lump Sum Trap” is Real: Taking a large, one-time TSP distribution to pay off a mortgage or buy a car can feel liberating, but it can create a massive, temporary income spike that triggers the highest IRMAA brackets for two full years.

- FEHB Offers a Unique Choice: Unlike private-sector retirees, you have the option to keep FEHB as your primary insurance in retirement and potentially delay enrolling in Medicare Part B, which is a powerful (but complex) strategy for managing costs.

What is IRMAA and Why Are Federal Retirees Uniquely Exposed?

QLAC

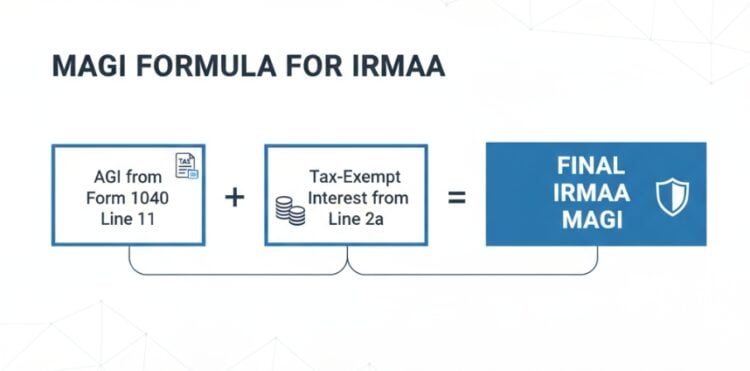

IRMAA (Income-Related Monthly Adjustment Amount) is a surcharge that higher-income retirees pay for Medicare Part B and Part D premiums. For 2026, the standard Medicare Part B premium is $202.90 per month, but those with higher incomes pay significantly more due to IRMAA surcharges. The Social Security Administration (SSA) determines if you owe this surcharge based on your tax return from two years prior—meaning your 2026 IRMAA is based on your 2024 income. In 2026, IRMAA applies to individuals with Modified Adjusted Gross Income (MAGI) above $109,000 (single filers) or $218,000 (married filing jointly), with total monthly Part B premiums ranging from $284.10 to $689.90 depending on income. For a detailed breakdown of the income levels, see our guide to the current IRMAA brackets and Medicare surcharges.

While IRMAA affects all retirees, federal employees face a unique triple threat:

- Large TSP Balances: Decades of saving have resulted in significant tax-deferred balances.

- Taxable Pensions: Your FERS or CSRS annuity is another source of taxable income.

- Complex Health Insurance Choices: The interaction between FEHB and Medicare adds a layer of complexity private-sector retirees don’t face.

💡 Michael Ryan Money Tip

The core of the problem is that every withdrawal from your traditional TSP is counted as income. For a full list of what is included in the calculation, see our guide on what income counts toward your IRMAA MAGI.

💡 Protect Your Federal Retirement from Hidden Traps

One clear financial move each week — straight from 28 years of seeing what goes wrong for federal employees.

- → Avoid costly TSP withdrawal mistakes.

- → Navigate FEHB & Medicare coordination.

- → Get proven strategies to lower your MAGI.

Get federal retirement insights delivered straight to your inbox each week.

📬 No spam. Unsubscribe.

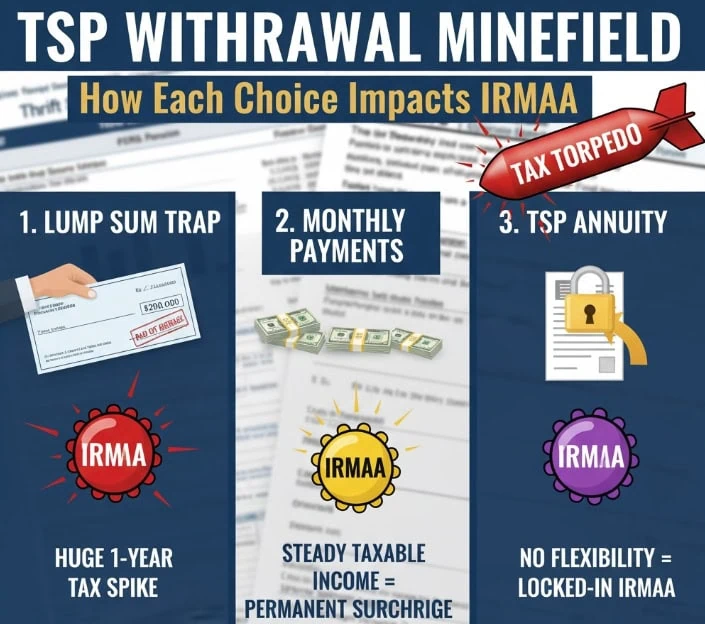

The TSP Withdrawal Minefield: How Each Choice Impacts IRMAA

Your TSP withdrawal options are flexible, but each one has a direct and significant impact on your future Medicare premiums.

1. The Lump-Sum Withdrawal: The Biggest IRMAA Trap

Taking a large, single payment from your TSP is the fastest way to trigger a massive IRMAA bill.

2. Monthly Payments: The Slow and Steady Surcharge

Choosing to receive a fixed monthly payment from your TSP provides predictable income, but it also creates a steady stream of taxable income that adds to your MAGI every single year. If this amount, combined with your pension and Social Security, pushes you over the threshold, it can lock you into paying IRMAA permanently.

3. The TSP Annuity: Locking in Your Fate

Using your TSP to purchase a life annuity creates an irreversible stream of income. While this provides maximum security, it also eliminates your flexibility. If the annuity payments, plus your other income, trigger IRMAA, you will have no way to adjust your withdrawals to get back under the threshold in future years.

💡 Protect Your Federal Retirement from Hidden Traps

One clear financial move each week — straight from 28 years of seeing what goes wrong for federal employees.

- → Avoid costly TSP withdrawal mistakes.

- → Navigate FEHB & Medicare coordination.

- → Get proven strategies to lower your MAGI.

Get federal retirement insights delivered straight to your inbox each week.

📬 No spam. Unsubscribe.

The Critical Choice: FEHB and Medicare Coordination

As a federal retiree, you have a choice that most others don’t: you can keep your FEHB plan in retirement. This creates a critical decision point around age 65.

Option 1: Keep FEHB and Enroll in Medicare Part A & B (Most Common)

In this scenario, Medicare becomes the primary payer and your FEHB plan acts as secondary coverage, often covering co-pays and deductibles that Medicare doesn’t.

Most federal retirees choose this route. However, you must pay the Medicare Part B premium, which is the premium subject to IRMAA.

Option 2: Keep FEHB and Only Enroll in Medicare Part A

If you or your spouse are still actively working for the federal government and covered by FEHB, you can delay enrolling in Medicare Part B without penalty.

In this case, FEHB remains your primary insurer. You (and thus any IRMAA) for as long as you have this active employment coverage.

⚠️ Myth Busted

Many federal retirees believe they don’t need Part B at all if they have FEHB. This is a dangerous misconception. If you are retired (not actively working) and you delay enrolling in Part B, you will face a lifetime late-enrollment penalty and your FEHB plan may significantly reduce its coverage, assuming Medicare is the primary payer. [OPM.gov]

3 Strategies to Mitigate IRMAA for Federal Retirees

The goal is not to fear your TSP, but to manage it intelligently.

Time Your Withdrawals Strategically

The two years between retiring (say, at 63) and starting Medicare (at 65) are a “golden window.” This is often a period of lower income. It can be the perfect time to make strategic Roth conversions or take needed withdrawals, paying tax in those lower-income years to avoid creating an income spike that will affect your premiums once you’re on Medicare.

Use the Roth TSP.

Contributions to the Roth TSP are made after-tax, but qualified withdrawals in retirement are 100% tax-free. This money is “invisible” to the IRMAA calculation.

The more you have in your Roth TSP, the less you will be forced to withdraw from your traditional TSP, giving you powerful control over your future MAGI.

Consider a Qualified Longevity Annuity Contract (QLAC).

Recent rule changes now allow you to use a portion of your TSP funds (up to $210,000 in 2026) to purchase a QLAC. This defers income (and taxes) until as late as age 85, which also reduces the RMDs you will have to take from your TSP, thereby lowering your MAGI in your 70s and early 80s.

Don’t let a simple lack of coordination between your hard-earned federal benefits turn into a costly retirement surprise. By understanding how the pieces fit together, you can create a withdrawal strategy that funds your retirement without unnecessarily inflating your Medicare costs.

Frequent Reader Questions

Do withdrawals from the Roth TSP count towards IRMAA?

No. Qualified (tax-free) distributions from a Roth TSP or a Roth IRA do not count as part of your Modified Adjusted Gross Income (MAGI) and therefore cannot trigger IRMAA surcharges. This makes the Roth TSP an incredibly powerful tool for managing future Medicare costs.

If I keep FEHB, do I have to enroll in Medicare Part D for prescriptions?

No. The prescription drug coverage offered by FEHB plans is considered “creditable coverage” by Medicare. This means it is at least as good as a standard Part D plan, so you can keep your FEHB drug plan and avoid the Part D late-enrollment penalty if you decide to switch later. [Medicare.gov]

Can I appeal an IRMAA determination caused by a large TSP withdrawal?

Generally, no. A large, voluntary withdrawal is not considered a “life-changing event” by the Social Security Administration. Appeals are typically reserved for events like death of a spouse, divorce, or work stoppage. This is why proactive planning to avoid the income spike is so critical. For more on the appeals process, read our guide to Form SSA-44.

Master Your Federal Retirement

- Learn the core strategies to avoid surcharges – Discover proactive ways to manage your income and keep your Medicare premiums low throughout retirement.

- Visit the official Thrift Savings Plan website – Access official forms, publications, and tools directly from the source to manage your TSP account.

- Explore FEHB and Medicare resources at OPM.gov – The Office of Personnel Management provides the definitive guides on how your federal health benefits coordinate with Medicare.

The Bottom Line on IRMAA for Federal Retirees

What the official guidebooks often miss is that your TSP, your greatest retirement asset, can become your biggest Medicare liability two years later, thanks to the IRMAA lookback rule. For federal retirees, a successful retirement isn’t just about saving diligently; it’s about strategically timing the de-accumulation of your assets to protect your benefits from this tax torpedo.

What This Means for You

- If you’re still working (5+ years from retirement): Your primary mission is to build your Roth TSP balance. Every tax-free dollar you have later is a dollar that is invisible to the IRMAA calculation.

- If you’re in the 1-3 year window before starting Medicare: This is your “golden window.” You must carefully model any large, necessary withdrawals or begin a Roth conversion strategy now, while your income is potentially lower.

- If you’re already retired and on Medicare: Your focus shifts to defense. Meticulously plan your annual TSP withdrawals to stay just under the IRMAA income cliffs, and consider using strategies like Qualified Charitable Distributions (QCDs) to satisfy your RMDs without increasing your MAGI.

Your Next Steps

Project your retirement income. Add your estimated FERS/CSRS pension, your Social Security benefit, and a conservative annual TSP withdrawal. See where that total lands relative to the current IRMAA brackets.

Identify your “golden window.” Pinpoint the exact years between your planned retirement date and your 65th birthday. This is your prime opportunity for strategic tax planning to mitigate future IRMAA.

Review your withdrawal sequence with a fee-only, fiduciary financial advisor who has specific experience navigating the complexities of federal employee benefits.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.