📘 Client Story: The Shock of a New Bill

I once worked with a client, let’s call her Carol. Her husband passed away in early 2024. Their joint income on their 2024 tax return had been around $160,000. In early 2026, Carol received her IRMAA notice for the year, and her Medicare Part B premium had nearly tripled. The notice was based on that $160,000 joint income from her 2024 return. But because she was now considered ‘Single’ for 2026, that income level pushed her deep into the IRMAA brackets. She was paying a penalty based on a life that no longer existed and an income she no longer had.

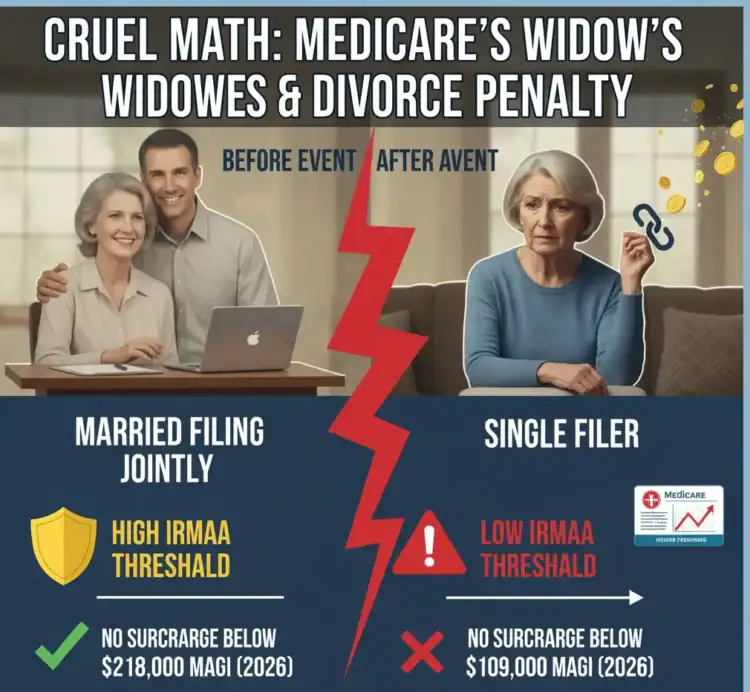

The Divorce Penalty

The logic is the same for a divorce. Your 2026 Medicare premiums are based on your 2024 tax return. If you were married in 2024, your MAGI reflects your joint income. After a divorce, your individual income is likely much lower. The SSA’s system, however, will continue to penalize you based on your ex-spouse’s income until you correct the record.

Filing an appeal is not as intimidating as it sounds. It’s a straightforward process of providing the SSA with new information.

- Get Form SSA-44

- Gather Your Evidence

- This is the most critical step. You need to prove two things: the life-changing event happened, and your income went down.

🚀 Your Document Checklist

- Proof of the Event (Provide One):

- For Death of a Spouse: A certified copy of the death certificate.

- For Divorce or Annulment: A copy of the final divorce decree, signed by the judge.

- Proof of Income Reduction (Provide One):

- If you stopped working: A letter from your former employer (on company letterhead) stating your retirement or termination date.

- If you reduced work hours: Recent pay stubs showing your new, lower pay rate.

- If you lost pension/annuity income: A statement from the payer showing the income has stopped or been reduced.

- If you are self-employed: A signed letter detailing the change in your business (e.g., “My income is projected to decrease due to the sale of my business assets.”).

💡 Michael Ryan Money Tip

From 25+ years of experience, here’s an insider tip: the SSA loves to see a copy of your filed Form 1040-ES (Estimated Tax) for the current year. It is one of the strongest forms of proof for a self-employed individual that you are projecting a new, lower income and are already paying taxes based on that new reality.

- Complete the Form. The form is only a few pages long.

- Step 1: Beneficiary Information: Fill in your personal details, including your Medicare number.

- Step 2: Life-Changing Event: Check the box for “Death of Spouse” or “Divorce or Annulment” and enter the date the event occurred.

- Step 3: Income Projection: This is where you estimate your new MAGI for the year of the event. (MAGI, or Modified Adjusted Gross Income, is your Adjusted Gross Income from your tax return plus any tax-exempt interest you earned). Use your current income statements to make a reasonable, good-faith estimate.

- Step 4: Sign and Date: Complete the form with your signature.

4. Submit Your IRMAA Appeal

You can mail or fax the completed Form SSA-44 and your supporting documents to your local Social Security office. You can also call the SSA to make an appointment or, in many cases, upload the completed form and documents online through your secure my Social Security account on SSA.gov.

What to Expect After You File

Once you submit your appeal, the process typically follows a clear timeline.

- Processing Time: It usually takes the SSA 4-8 weeks to review your appeal and make a decision.

- Paying Premiums: You MUST continue to pay the higher IRMAA premium while your appeal is pending. If you don’t, you risk losing your Medicare coverage.

- The Decision Letter: The SSA will mail you a formal determination letter. If your appeal is approved, it will state your new premium amount.

- The Refund: The SSA will then notify Medicare of the change. Medicare will automatically process a refund for all the premium surcharges you overpaid.

💡 Avoid Costly Medicare Mistakes

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Learn how to avoid common IRMAA triggers.

- → Understand the “Widow’s Penalty” fully.

- → Get strategies to lower your MAGI for good.

Get insights on IRMAA delivered straight to your inbox each week.

📬 No spam. Unsubscribe.

You Don’t Have to Do This Alone

As a retired financial planner who has guided hundreds of clients through this exact process, I know how overwhelming it can feel. This appeal is a critical first step.

- Want to learn more? For widows and widowers, understanding your new benefits is crucial. Read our complete guide on Social Security Survivor Benefits.

- Feeling stuck? If you’re a new widow, widower, or divorcée and want a professional to review your situation, our firm offers a no-obligation consultation.

Frequent Reader Questions

Can I appeal IRMAA online?

Yes, you can now appeal IRMAA oniine. While you can always mail, fax, or bring your documents to a local office, the Social Security Administration allows you to upload a completed Form SSA-44 and your supporting documents through a secure my Social Security account online.

This can often be the fastest and most efficient method.

How long do I have to file Form SSA-44? Is there a deadline?

There is no official deadline, but you should file as soon as you have evidence of the event (like the death certificate) and can estimate your new, lower income.

The sooner you file, the sooner your premium will be corrected and you can be refunded for any overpayments.

Do I have to file this appeal every year?

No. This is not an annual appeal. Once your appeal is approved, the SSA uses this new, lower income as your new baseline. You would only need to file again if you have another qualifying life-changing event in the future.

Will I definitely get a refund for the high premiums I already paid?

Yes. Once your appeal is approved, the SSA notifies Medicare, who will then automatically calculate the amount you overpaid since the date of your life-changing event. You will be refunded this full amount, though it can take 6-8 weeks after approval to receive it.

What if my income is still high after my divorce?

The appeal is only for situations where the life-changing event caused your income to drop below the IRMAA threshold you were assigned. If your new, individual income is still high enough to fall into an IRMAA bracket for a ‘Single’ filer, you will still be required to pay the appropriate surcharge.

Master Your IRMAA Strategy

The Bottom Line: This Is One Financial Battle You Can Win

Receiving that IRMAA notice during an already overwhelming time can feel like the final straw. It’s easy to feel powerless against a complex system. But remember what that letter really is: an automated penalty based on old data from a life you no longer live. It’s a bureaucratic error, not a final judgment.

In my near 30 years of practice, the clients who found the most immediate relief were the ones who took action on this right away. You now have the same playbook I’ve shared with them: you know the why, you have the form number, and you have the step-by-step plan.

Your next step isn’t to do more research or to worry for another week. It’s to download Form SSA-44, gather your two pieces of evidence, and submit your appeal. This is one of the rare financial problems with a clear, direct solution. Taking this action isn’t just about lowering a premium; it’s about taking back a piece of control over your financial life when it matters most.

It’s your money. Don’t let an automated mistake keep it.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.