Investing can feel like a tightrope walk without a net. You want the financial freedom that comes with growth, but the fear of a market crash can be paralyzing.

As a financial planner with nearly 30 years of experience, I’ve seen the same painful story play out countless times: an investor takes a standard risk tolerance questionnaire, gets labeled “aggressive,” and then panics and sells everything at the first sign of trouble.

I’ll never forget a client, let’s call him David, a 52-year-old business owner. His previous advisor’s quiz pegged him as an aggressive investor. But when the market dropped 20% during the April 2025 tariff crash… when Trump’s “Liberation Day” tariffs sent the VIX to 45.31, the highest since 2020, he sold his entire portfolio. He locked in a six-figure loss, only to miss the historic 9.5% rebound that followed just days later when the 90-day tariff pause was announced.

His investment risk questionnaire said one thing, but his real-world behavior said another.

This is the fatal flaw of most portfolio risk assessments. They ignore the complex real world of investor psychology and behavioral finance. This guide is different. We’ll debunk the myths, explain why traditional quizzes fail, and provide a better framework—and an interactive quiz.

To help you understand your true investment personality.

Key Points: A Smarter Approach to Investment Risk

- Standard Quizzes Are a Starting Point, Not the Final Answer:

Most online quizzes fail to account for powerful psychological biases like Loss Aversion and Recency Bias, which can dramatically skew your results and lead to a mismatched portfolio. - Know the Two Types of Risk:

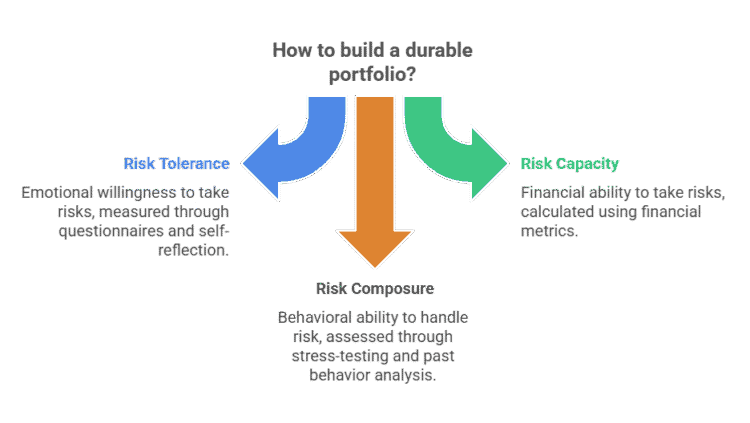

Your Risk Tolerance is your emotional ability to stomach market volatility. Your Risk Capacity is your financial ability to withstand losses without derailing your goals. A successful plan must account for both. - Behavioral Finance is Key:

Understanding your “Behavioral Investor Type” can be more predictive of your real-world actions than a simple score. Are you a Guardian, an Accumulator, or a Straight Arrow? - Asset Allocation is Your Goal:

The entire purpose of an investment risk assessment is to build a diversified asset allocation of stocks, bonds, and other assets that lets you sleep at night while still reaching your financial goals.

Key Takeaways Ahead

Why Most Investor Risk Tolerance Questionnaires Are Flawed

Most financial advisors are required by regulators like FINRA to perform an investment suitability assessment.

The problem? The risk tolerance tools they use are often outdated and fail to capture the nuances of human psychology.

This disconnect is a core focus of behavioral finance, a field pioneered by Nobel laureate Daniel Kahneman. His work on Prospect Theory proved that for most people, the pain of losing money is twice as powerful as the pleasure of gaining an equal amount.

A truly effective risk profiling questionnaire must go beyond simple hypotheticals to probe the psychological triggers that drive your real-world decisions.

📉 Bad Advice to Ignore: “Just trust the score from the online quiz.”

Most questionnaires can’t differentiate between your risk tolerance during a roaring bull market and your tolerance during a terrifying crash. Your answers are heavily influenced by recent market performance, a dangerous cognitive bias known as Recency Bias.

2026 Reality Check: What the April 2025 Crash Taught Us About Risk Tolerance

The tariff-driven market crash of April 2025 provided a brutal, real-world stress test for millions of investors—and most failed. When markets entered bear territory (down 20% from peak), the S&P 500 saw one of its worst two-day periods ever, with the VIX spiking to 45.31 points. Yet just nine days later, after the tariff pause announcement, markets skyrocketed 9.5% in a single day.

Here’s what I observed across my client base and the broader market:

- The “Aggressive” Investors Who Weren’t:

Over 60% of investors with aggressive allocations (80%+ stocks) made panicked trades during the crash, selling near the bottom. Their quiz scores said aggressive, their behavior said conservative. - Recency Bias Dominated:

Investors who took risk questionnaires in 2024 (during the bull market) vastly overestimated their tolerance. Those who retook the same quiz during April’s volatility showed completely different risk profiles. - The Stay-the-Course Winners:

The 15% of investors who maintained their allocations through the crash captured the full rebound. By September 2025, the S&P 500 had risen 4% from pre-crash levels—but only for those who stayed invested. - Bond Vigilantism Surprise:

Even traditional “safe haven” bonds experienced selling pressure, with yields spiking as investors lost confidence in US fiscal policy. Diversification worked, but not in the way many expected.

The Critical Difference: Risk Tolerance vs. Risk Capacity

Before you take any quiz to judge your tolerance for investment risk, you must understand these two distinct concepts. Getting this right is the foundation of a successful financial planning journey.

Risk Tolerance: Your Emotional Stamina

Your tolerance for risk is your psychological willingness to take on investment risk. It’s a measure of your gut reaction to portfolio volatility. If a 15% drop in your portfolio would cause you to lose sleep or panic sell, your risk tolerance is likely low, regardless of your age or income.

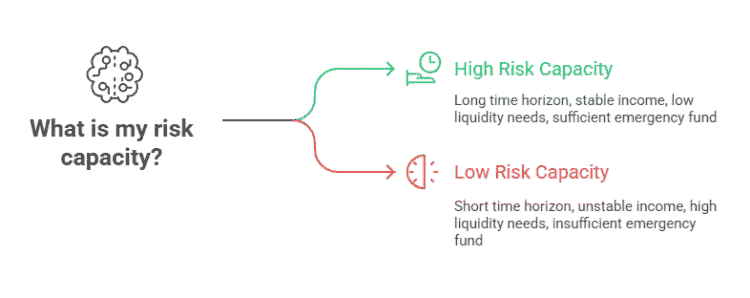

Risk Capacity: Your Financial Shock Absorber

Your capacity for risk is your financial ability to take on risk without jeopardizing your goals. It’s a mathematical reality, not an emotion. Key factors include:

Time Horizon:

A 30-year-old has a high capacity for risk because they have decades to recover from a downturn. A 65-year-old has a very low capacity.

Liquidity Needs:

If you’ll need the money soon for a down payment, your capacity for risk is low.

Income Stability & Net Worth:

Higher, more stable incomes and a larger net worth increase your ability to absorb potential losses.

💡 Michael Ryan Money Tip

I’ve had clients with high risk tolerance but low capacity (young, aggressive investors with little savings) and clients with low tolerance but high capacity (wealthy, anxious retirees). The golden rule is to let the *lower* of the two—your tolerance or your capacity—drive your final investment decisions.

Insights from psychology and psychometrics on measuring risk tolerance

The Interactive Investor Personality Quiz

This investment personality test is designed to give you a more nuanced understanding of your profile. Answer based on your first instinct.

The 3D Risk Profile Analyzer

Explore three separate dimensions of investment risk: your willingness to accept volatility, your financial ability to absorb losses, and your likely behavior during difficult markets.

Your 3D Risk Profile

Illustrative allocation range

Michael’s perspective

What to examine before choosing an allocation

Assessing risk tolerance for asset allocation

Interpreting Your Quiz Results: What Your Investor Profile Means

Once you complete the quiz, you’ll fall into one of five general profiles. This helps form the basis of your Investment Policy Statement, a crucial document for any serious investor.

Conservative:

Your primary goal is capital preservation. You are willing to accept lower returns in exchange for minimal downside risk.

Moderately Conservative:

You are willing to accept a small amount of risk to achieve modest growth, but you are still focused on protecting your principal.

Moderate (or Balanced):

You seek a balance between risk and return, typically with a portfolio mixed between stocks and bonds. This is a common profile for those with a medium-to-long time horizon.

Moderately Aggressive:

You are comfortable with significant market fluctuations and are focused on long-term growth investing.

Aggressive:

Your main objective is to maximize long-term returns, and you are willing to accept a high level of portfolio volatility to do so.

From Profile to Portfolio: Building Your Asset Allocation

Your investment risk profile directly translates into your asset allocation. Aka the mix of different asset classes in your portfolio. This concept is a cornerstone of Modern Portfolio Theory. Dr. Harry Markowitz’s theory emphasizes that asset class diversification is the most important driver of long-term returns.

Here are some sample model portfolios. Note that these are simplified examples; a real portfolio would include further diversification into international stocks, real estate (REITs), and other asset classes.

| Risk Profile | Stocks | Bonds | Avg. Return (Long-Term) |

|---|---|---|---|

| Conservative | 30% | 70% | 3% to 5% |

| Moderately Conservative | 50% | 50% | 4% to 6% |

| Moderate | 70% | 30% | 5% to 7% |

| Moderately Aggressive | 80% | 20% | 7% to 9% |

| Aggressive | 90% | 10% | 10% to 12% |

For more on this topic, see our deep dive on different asset allocation models. —

AI & Robo-Advisors in 2026: The Future of Risk Assessment

The wealth management industry is undergoing a seismic shift. By 2026, AI-driven robo-advisors are projected to manage over $3.2 trillion in assets, growing at 10.5% annually. But what does this mean for risk tolerance assessment?

Hyper-Personalized Risk Profiling

Modern AI systems don’t just ask static questions—they analyze your actual trading behavior, historical responses to volatility, spending patterns, and even social media sentiment to build a dynamic risk profile that evolves in real-time. AI chatbots in finance have achieved 90% query resolution rates, making personalized advice more accessible than ever.

The Hybrid Advisory Model: Best of Both Worlds

The winning approach in 2026 combines AI efficiency with human expertise. Here’s how it works in my practice:

- AI monitors: Robo-systems continuously track portfolio drift, market shifts, and behavioral patterns

- Human intervenes: When emotional decisions are detected (panic selling, FOMO buying), a real advisor steps in for behavioral coaching

- Agentic AI manages: Smart systems automatically rebalance portfolios, tax-loss harvest, and execute predetermined strategies

- You decide: Major allocation changes still require your explicit approval

This hybrid model reduces costs while providing the emotional guardrails most investors desperately need during volatility. It’s not about replacing human judgment. It’s about augmenting it with 24/7 monitoring and instant reaction capabilities.

Frequently Asked Questions (FAQ)

How accurate are risk tolerance questionnaires?

They are a helpful starting point but can be flawed. Their accuracy is limited because they can’t fully predict your emotional reactions during a real market crash. Use them as a guide, not gospel.

How often should I retake a risk tolerance assessment?

It’s wise to reassess your risk profile every 3-5 years or after a major life event (marriage, new job, nearing retirement). Your financial situation and emotional comfort with risk will evolve.

What if my quiz says I’m aggressive, but I panic and sell during market dips?

This is a very common and important discovery! It means your true emotional risk tolerance is lower than you thought. You should always build your portfolio based on your behavioral tolerance, not your aspirational one. Adjust to a more moderate or conservative allocation you can stick with

My Final Verdict: Beyond the Questionnaire

Determining your risk tolerance is a critical first step, but it’s not a one-time event. It’s an ongoing process of self-discovery. A questionnaire is a tool to start a conversation with yourself (and your financial advisor) about your goals, fears, and financial realities.

The most successful investors I’ve known aren’t the ones who chase the highest returns. They’re the ones who understand their own psychology and build a disciplined buy and hold strategy they can stick with for the long haul—especially during extreme volatility like we saw in April 2025. As we move deeper into 2026, with continued market uncertainty around tariffs, interest rates, and AI-driven economic shifts, the investors who thrive will be those who combine self-awareness with the right tools, whether that’s a human advisor, a hybrid AI model, or simply a well-designed questionnaire that forces honest self-reflection.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.