Visualizing the financial impact of strategic planning is crucial to understanding IRMAA surcharges. The table below breaks down exactly how specific planning decisions reduced MAGI and eliminated unnecessary Medicare premiums, resulting in significant long-term savings.

| Item | Scenario A (No Plan) |

Scenario B (Jane’s Plan) |

Savings |

|---|---|---|---|

| Filing Status | Single | Single | N/A |

| MAGI | $112,000 | $105,000 | −$7,000 |

| IRMAA Tier | Tier 1 Surcharge | Standard Base | Tier Drop ✓ |

| Part B Cost | $284.10/mo | $202.90/mo | +$975/yr |

| Part D Cost | Plan + $14.50/mo | Plan Base | +$174/yr |

| Total 5-Year Savings | Paying Surcharge | Base Premium | ~$5,745 |

To avoid overpaying like in Scenario A, check your Modified Adjusted Gross Income (MAGI) against the latest 2026 brackets immediately to see if you are approaching a cliff.

Retirement planning is full of theory. But theory doesn’t pay the bills. Strategy does.

Today, you will see exactly how one retiree Jane, a 72-year-old retired teacher eliminated a $2,400 annual Medicare surcharge using 5 proven tax strategies. This isn’t a hypothetical. It is a blueprint you can copy, starting today.

Most retirees think Medicare premiums are fixed. They aren’t. That’s where the Michael Ryan Money Medicare IRMMA Recovery Plan comes in.

Jane thought she was doing everything right. She had a pension, Social Security, and a healthy IRA. Then she received her Initial Determination Notice from the Social Security Administration.

Because her income sources “stacked” on top of each other… Pension plus Social Security plus Required Minimum Distributions (RMDs). Her Modified Adjusted Gross Income (MAGI) spiked. She crossed the IRMAA surcharge cliff by just $1,500. That small overage triggered a penalty that cost her $2,400 a year.

She was paying a “success penalty” for saving in her Traditional IRA.

But Jane didn’t just pay it. We built a 5-step recovery plan to restore her base Medicare premium.

📊 Is Jane’s Scenario Similar to Yours?

Before diving into the fix, let’s diagnose your situation. Check all that apply:

- [ ] I am age 65+ and enrolled in Medicare Part B (or will be within 2 years).

- [ ] My MAGI is within $15,000 of an IRMAA income threshold.

- [ ] I take Required Minimum Distributions (RMDs) or will start at age 73.

- [ ] I have a pension or annuity income that stacks on my Social Security.

- [ ] I experienced a Life-Changing Event (Retirement, Divorce, Death of Spouse) in the last 2 years.

The Verdict:

- 0-2 checked: Focus on prevention (Strategies 2-4).

- 3-4 checked: You are in Jane’s zone—read all five strategies.

- 5 checked: You are a perfect candidate for this recovery plan.

Key Takeaways Ahead

The “Income Stack” Trigger: Why Jane’s Numbers Collided

The root of the problem wasn’t that Jane was “too rich.” It was that her income sources collided on IRS Form 1040.

The Income Stack:

- Pension: $45,000 (Fixed, taxable).

- Social Security: $32,000 (85% taxable).

- RMDs: $35,000 (Fully taxable withdrawal from Traditional IRA).

Total MAGI: ~$112,000.

In 2026, the first IRMAA surcharge threshold for a single filer is $109,000 of Modified Adjusted Gross Income (MAGI). Because of the two-year lookback rule, 2026 premiums are based on 2024 income. Jane’s 2024 MAGI was $112,000—roughly $3,000 over the threshold.

Here is the brutal math of the IRMAA cliff: A “cliff” means that if you go even $1 over the threshold, you pay the higher IRMAA premium on every month—not just on the dollars above the line. Because Jane exceeded the limit by $3,000, the Centers for Medicare & Medicaid Services (CMS) applied the full Tier 1 surcharge to every month of her premiums. In Jane’s case study, this worked out to roughly $1,150 per year in added premiums.

⚡ Jane’s Savings Snapshot: The ROI of Planning

Visualizing the financial impact of strategic planning is crucial to understanding IRMAA surcharges. The table below breaks down exactly how specific planning decisions reduced MAGI and eliminated unnecessary Medicare premiums, resulting in significant long-term savings.

| Item | Scenario A (No Plan) |

Scenario B (Jane’s Plan) |

Savings |

|---|---|---|---|

| Filing Status | Single | Single | N/A |

| MAGI | $112,000 | $105,000 | -$7,000 |

| IRMAA Tier | Tier 1 Surcharge | Standard Base | Tier Drop |

| Part B Cost | $284.50/mo | $202.90/mo (est) | +$979/yr |

| Part D Cost | Plan + $13.70/mo | Plan Base | +$164/yr |

| Total 5-Year Savings | Paying Surcharge | Base Premium | +~$5,700+ |

To avoid overpaying like in comparison A, check your Modified Adjusted Gross Income (MAGI) against the latest 2026 brackets immediately to see if you are approaching a cliff.

Get retirement tax strategies delivered straight to your inbox each week.

📬 No spam. Unsubscribe.

💡 STOP OVERPAYING MEDICARE & KEEP YOUR PENSION

One clear financial move each week — straight from 28 years of helping retirees avoid costly traps.

- → Timely alerts on hidden retirement taxes like IRMAA.

- → Proven strategies to lower your MAGI and protect income.

- → Actionable steps to execute before IRS deadlines pass.

The 5-Step IRMAA Rescue Plan (Choose Your Weapon)

We didn’t accept the IRMAA surcharge. We engineered a way out for the following tax year (remember, Medicare premiums use a 2-year lookback period).

Which IRMAA Recovery Strategy Fits You?

- Strategy 1 (QCD): You’re 70½+, charitable, and have an IRA.

- Strategy 2 (Roth): You have 5+ years until RMDs or “room” in your tax bracket.

- Strategy 3 (Pension Timing): You control your annuity start date.

- Strategy 4 (Tax-Loss Harvesting): You have a taxable brokerage account with losses.

- Strategy 5 (SSA-44): You had a Life-Changing Event (Retirement/Divorce).

Strategy 1: The QCD “Income Eraser”

Jane gives $3,000 annually to her church and the local animal shelter. Previously, she wrote checks from her bank account—using after-tax dollars that did nothing to lower her MAGI.

The Shift:

A Qualified Charitable Distribution (QCD) lets IRA owners who are age 70½ or older send money directly from their IRA to a qualified charity. When the custodian sends the funds straight to the charity, that amount can count toward your Required Minimum Distribution but does not get included in your taxable income. Jane, at age 72, qualified for this strategy. She now directs her IRA custodian to send $3,000 directly to her church and the local animal shelter each year.

The Math:

In Jane’s case, redirecting her $3,000 annual charitable giving as a QCD meant $3,000 of her RMD no longer showed up in Adjusted Gross Income, which lowered her IRMAA-related MAGI.

- Result: MAGI dropped from $112,000 to $109,000. She was right on the line.

➡️ Deep Dive: Using QCDs to Lower IRMAA Exposure

Strategy 2: The Roth “RMD Shrinker”

We realized Jane had “room” in the 22% tax bracket before hitting the next surcharge tier.

The Strategy:

Instead of leaving money in her Traditional IRA to grow (and create larger future RMDs), we initiated micro-Roth conversions of $5,000 per year.

The Benefit:

Jane pays income tax on the conversion now, but this action permanently removes those assets from the RMD calculation. This stops the “RMD creep” that would otherwise push her into Tier 2 or Tier 3 later in retirement.

What if I’m already on Medicare?

You can still convert. Use a Roth conversion calculator to find the “sweet spot”—converting enough to reduce future RMDs without spiking your current premium.

Strategy 3: The Pension “Delay Valve”

Jane had the option to trigger a small secondary annuity payout she inherited.

The Move:

We delayed the start date by two years.

Why?

This kept her current income lower while we aggressively converted her IRA to Roth. By the time the annuity payments commenced, her RMDs were lower, ensuring the total “income stack” remained below the IRMAA surcharge threshold.

Strategy 4: The Tax-Loss “Offset”

Jane held a taxable brokerage account with bond funds that had lost value due to interest rate hikes.

The Harvest:

We sold the specific tax lots to realize a $3,000 capital loss.

The Deduction:

The IRS allows taxpayers to use up to $3,000 of net capital losses to offset ordinary income on Form 1040.

The Result:

This deduction directly lowered her MAGI by another $3,000. Now she was safely under the $109,000 cliff.

➡️ Learn How: Tax-Loss Harvesting for IRMAA Reduction

Strategy 5: The SSA-44 “Income Update” (The Immediate Fix)

The Social Security Administration allows you to request a reconsideration of your IRMAA if you’ve had a qualifying Life-Changing Event such as retirement (work stoppage), work reduction, marriage, divorce, death of a spouse, or loss of pension income. You do this using Form SSA-44 (Medicare Income-Related Monthly Adjustment Amount – Life-Changing Event). Jane’s full retirement early in the year qualified as a work stoppage, one of the specific Life-Changing Events recognized by the SSA.

The Action:

We filed Form SSA-44 (Medicare Income-Related Monthly Adjustment Amount – Life-Changing Event) immediately.

The Argument:

“Please use my current, lower income to calculate my premium, rather than my tax return from two years ago.”

The Win:

The Social Security Administration approved the request. Her premiums dropped that same year, saving her money immediately rather than waiting for the 2-year lag.

Pro Tip: Always mail your SSA-44 via Certified Mail with Return Receipt. Local offices handle millions of documents; get a tracking number to prove you filed on time.

➡️ Step-by-Step: The Complete Form SSA-44 Guide

🔄 Checkpoint: Can You Combine These Strategies?

Jane used Strategies 1-5 together because she had the “perfect storm” of charitable intent, IRA assets, and a qualifying life event. Most readers can stack at least two.

Quick Self-Check:

- If you’re 70½+: Start with Strategy 1 (QCDs). It is the most efficient way to lower AGI dollar-for-dollar.

- If you’re under 65: Prioritize Strategy 2 (Roth Conversions). Shrink the IRA before Medicare even starts.

- If you’re appealing: File Strategy 5 (SSA-44) first, then deploy 1-4 for future years to prevent recurrence.

Frequent Reader Questions

Can anyone use a QCD to lower Medicare premiums?

No. The taxpayer must be age 70½ or older. If you are 70, you must wait. However, you can plan for it. Since Jane was 72, she qualified perfectly. This strategy is the only way to satisfy an RMD without the funds appearing in your Adjusted Gross Income. [cite: IRS Publication 590-B]

Does the SSA-44 appeal form always work?

It only works if the beneficiary has experienced a specific Life-Changing Event listed on the form (Marriage, Divorce, Death of Spouse, Work Stoppage/Reduction, Loss of Pension). A retiree cannot file an appeal simply because they had high capital gains or a Roth conversion spike; that is not a valid reason for a reduction.

How do I know if I’m near a cliff?

Beneficiaries must track their Year-to-Date income. Look at your pay stubs, 1099s, and realized gains. Use an IRMAA Surcharge Calculator to project where your MAGI will land before December 31st.

The Bottom Line: Don’t Be a Victim of Your Own Financial Success

Jane isn’t a financial wizard. She is proof that IRMAA avoidance is systematic, not accidental.

By deploying five tax strategies in a specific sequence: QCDs, Roth conversions, pension timing, loss harvesting, and appeals—she turned a $2,400 annual liability into $0.

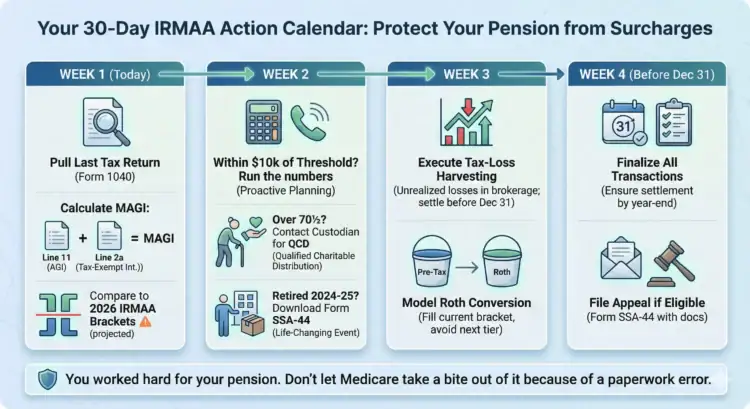

Your 30-Day IRMAA Action Calendar

Get retirement tax strategies delivered straight to your inbox each week.

📬 No spam. Unsubscribe.

💡 STOP OVERPAYING MEDICARE & KEEP YOUR PENSION

One clear financial move each week — straight from 28 years of helping retirees avoid costly traps.

- → Timely alerts on hidden retirement taxes like IRMAA.

- → Proven strategies to lower your MAGI and protect income.

- → Actionable steps to execute before IRS deadlines pass.

Week 1 (Today):

- Pull your last tax return (Form 1040).

- Calculate your MAGI: Line 11 (AGI) + Line 2a (Tax-Exempt Interest).

- Compare it to the 2026 IRMAA Brackets.

Week 2:

- If within $10,000 of a threshold: Run the numbers.

- If over 70½: Contact your IRA custodian to set up a QCD.

- If you retired in 2024-2025: Download Form SSA-44.

Week 3:

- Execute tax-loss harvesting if you have unrealized losses in a brokerage account (must settle before Dec 31).

- Model a Roth conversion to fill up your current bracket without crossing the next surcharge tier.

Week 4 (Before Dec 31):

- Finalize all transactions.

- File the appeal if eligible.

You worked hard for your pension. Don’t let Medicare take a bite out of it because of a paperwork error.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.