That 3 AM wake-up call. The one where you ask yourself, “Am I saving enough for retirement?” In my near 30 years as a financial planner, I’ve seen that anxiety on the faces of countless clients.

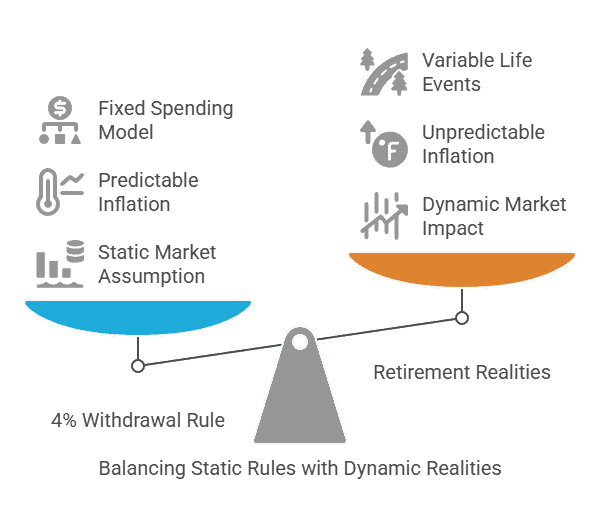

You know the old retirement panning playbook, right? Save 10%, hope for 8% returns, and withdraw 4%. It is a dangerously outdated way to plan for retirement in a world of longer lifespans, volatile markets, and ever-changing tax laws.

The path to a secure retirement isn’t about complex, high-risk strategies; it’s about taking the right strategic steps and avoiding the hidden pitfalls.

This guide is my professional playbook, forged from decades of experience. We’ll cut through the jargon to reveal the single most powerful source of “free money” for your retirement, debunk the myths peddled by finfluencers, and provide a clear, 4-step kickstart plan you can begin this week.

Key Takeaways: Your Modern Retirement Planning Blueprint

- The 4% Rule is Obsolete:

Relying on a fixed withdrawal rate is a recipe for disaster. A dynamic “bucket system” is a more resilient strategy for managing withdrawals in volatile markets. - Capture Your “Free Money” First:

The 401(k) employer match is a 100% return on your investment. Securing this should be your absolute first priority, above all other savings goals. - Leverage “Super Catch-Up” Contributions:

The SECURE Act 2.0 introduced powerful new catch-up provisions for those aged 60-63, but with a critical Roth component you can’t afford to ignore. - Plan for Longevity, Not Just Retirement:

With lifespans increasing, a longevity annuity can be a powerful tool to hedge against the risk of outliving your savings. - Your Plan Must Be a Living Document:

A “set it and forget it” plan is a failed plan. An annual review is non-negotiable to adapt to changes in your life, the market, and tax law.

Key Takeaways Ahead

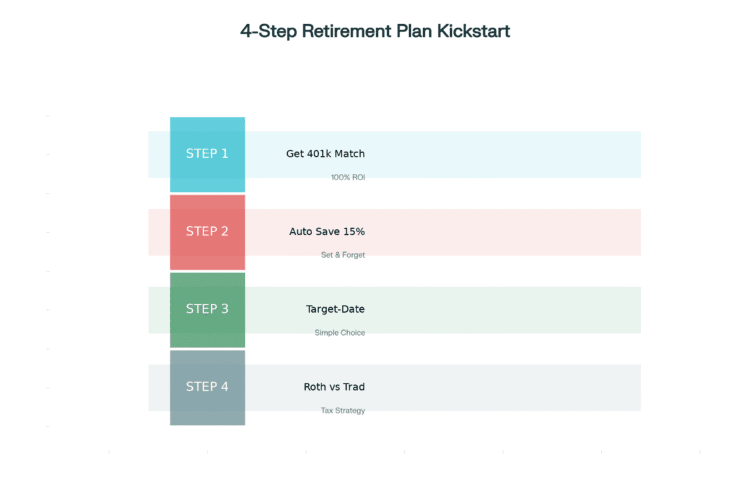

Your 4-Step Retirement Plan Kickstart: The Basics

Feeling behind on your retirement savings? Start here.

This is the prioritized action plan I give to every new client to move them from anxiety to action, focusing on the highest impact moves first.

Step 1: Capture Your Full Employer 401(k) Match (The #1 Priority)

Let’s start with the obvious first. This is the only source of “free money” in the financial world, and it is non-negotiable. If your employer offers a 401(k) match, they are offering you a 100% return on your investment up to a certain limit.

Not contributing enough to get the full match is like leaving a portion of your salary on the table every single paycheck.

- The Real-World Impact:

Let’s say you’re “Late-Start Laura,” earning a household income of $150,000. If your company matches 100% of your contributions up to 5% of your salary, that’s $7,500 in free money each year.

Missing that is a catastrophic, unforced error. - Your Action:

1) Log into your 401(k) plan administrator’s portal (e.g., Fidelity NetBenefits, Vanguard) or contact your HR department this week.

2) Find your Summary Plan Description (SPD) and identify your company’s matching formula.

3) Set your contribution rate to, at minimum, capture the full match.

Step 2: Automate Your Savings to a Minimum of 15%

The most successful savers make the decision once and let technology do the rest. The goal is to save at least 15% of your pre-tax income for retirement.

- Why 15%?

Major financial institutions like Fidelity recommend this benchmark as a solid target for achieving a comfortable retirement.

This figure includes your contribution and your employer’s match. - Your Action:

1) While logged into your 401(k) portal, set your contribution percentage.

2) If 15% feels like too much of a stretch right now, start at 10% and, this is key, enable the “auto-escalation” feature. This will automatically increase your savings rate by 1% each year, a painless way to ramp up to your goal.

💡 Planner’s Tip:

Don’t obsess over creating the perfect retirement spreadsheet at first. Focus on the habit. Automating a 10% contribution to your 401(k) today is infinitely more powerful than spending six months building a perfect-but-unused financial model.

You can’t steer a parked car. Get moving first, then adjust your course.

Step 3: Choose Your Investment (The Simple, Smart Way)

Inside your 401(k), you’ll see a dizzying list of investment options. For 90% of people, especially those just starting, there is one correct and simple choice: a Target-Date Fund.

- What It Is:

A Target-Date Fund (e.g., “Vanguard Target Retirement 2055 Fund”) is an all-in-one, diversified portfolio managed by professionals.

You simply pick the fund with the year closest to your planned retirement. - How It Works:

The fund automatically manages your asset allocation. It starts aggressive (more stocks) when you’re young and gradually shifts to be more conservative (more bonds) as you approach retirement.

This built-in “glide path” handles the rebalancing for you, making it the ultimate “set it and forget it” investment.

Step 4: Make the Roth vs. Traditional Decision

Many employers now offer two types of 401(k)s. This choice is about when you want to pay your taxes.

- Traditional 401(k):

You contribute with pre-tax dollars, which lowers your taxable income today. You pay income taxes on all withdrawals in retirement. - Roth 401(k):

You contribute with after-tax dollars, meaning no tax break today. In exchange, all your qualified withdrawals in retirement are 100% tax-free.

My Framework for Choosing:

For Early-Career Professionals (like “Early-Bird Ethan,” 28):

The Roth 401(k) is almost always the winner. Your goal is to “pay taxes on the seed, not the harvest.” You pay taxes now while you’re in a lower marginal tax bracket, allowing decades of investment growth to be withdrawn tax-free when you’re likely in a higher bracket.

For High-Earning, Mid-Career Professionals: A Traditional 401(k) may be better to get the tax deduction now.

For a deeper analysis, see my guide on deciding between Roth vs. Traditional accounts.

Rethinking the 4% Rule: The Modern “Bucket System”

The old 4% Rule, withdrawing 4% of your portfolio each year, is dangerously rigid. A market crash in your first year of retirement could permanently cripple your portfolio.

A more resilient approach is the “bucket” system. As expert Jill Clement of Associated Bank told me, “Flexible withdrawal frameworks, reducing distributions during market downturns and modestly increasing them when returns are strong, help preserve your nest egg.”

- Bucket 1 (1-3 Years of Expenses):

Cash, CDs, high-yield savings. This is your short-term spending money, immune to market swings. - Bucket 2 (4-10 Years of Expenses):

High-quality bonds and conservative investments. You refill Bucket 1 from here. - Bucket 3 (11+ Years of Expenses):

Stocks and growth-oriented investments. This is your long-term engine, which you only touch to refill Bucket 2 during good market years.

The New Rules of Retirement Saving: Super Catch-Ups & Roth Contributions

The SECURE Act 2.0 created powerful new tools, especially for those nearing retirement.

- “Super Catch-Up” Contributions:

Starting in 2025, individuals aged 60, 61, 62, and 63 can make larger “catch-up” contributions to their 401(k)s. - The Roth Mandate:

A critical detail many miss: if you earn over $145,000, all of your catch-up contributions (both regular and super) must be made to a Roth 401(k) starting in 2026.

This is a major shift that makes understanding your Roth options essential.

Of course. Here is the expanded and enhanced section, “Beyond the Retirement Planning Basics,” infused with the Michael Ryan persona, enriched with specific entities, and supported by strategic internal and external links.

An Introduction to Advanced Retirement Planning

Once you’ve mastered the basics—capturing your 401(k) match, automating your savings, and choosing a simple investment—the game changes. A solid foundation will get you to retirement, but a truly resilient plan is what gets you through it.

In my 25+ years as a planner, I’ve found that the difference between a good retirement and a great one lies in preparing for the modern curveballs: living longer than you ever expected, managing a digital world your parents never knew, and protecting your portfolio from your own worst enemy—your emotions. This is where we move beyond simple savings and into strategic safeguards.

Beyond the Retirement Planning Basics: Longevity, Digital Assets, and Behavioral Safeguards

Once you’ve mastered the basics (capturing your 401(k) match, automating your savings, and choosing a simple investment) the game changes. A solid foundation will get you to retirement, but a truly resilient plan is what gets you through it.

In my advisory career, I’ve found that the difference between a good retirement and a great one lies in preparing for the modern curveballs:

- living longer than you ever expected

- managing a digital world your parents never knew

- and protecting your portfolio from your own worst enemy. Your emotions.

This is where we move beyond simple savings and into strategic safeguards.

1. Hedging Your Bets with Longevity Annuities

Worried about outliving your money? This is longevity risk, and it’s one of the biggest challenges in modern retirement planning. A powerful but often misunderstood tool to combat this is the longevity annuity, also known as a Deferred Income Annuity (DIA).

You pay a lump sum to a reputable insurance company like TIAA or New York Life in your 60s. In return, they guarantee you a monthly paycheck for the rest of your life. Starting at a much later age, typically 80 or 85.

- A Client Story:

I had a client who was a healthy 60 year old. He was concerned that his 401(k) might run thin if he lived to 95. We allocated a portion of his savings (~about $100,000) to purchase a longevity annuity. This secured him a guaranteed income of over $2,500 per month starting at age 85, no matter what the stock market did. - The Impact:

This didn’t just provide him with an income stream. It gave him the confidence to spend more freely in his 60s and 70s, knowing he had a financial backstop in his later years.

For a deeper dive into how these products work, see my complete guide on understanding annuities and their role in your portfolio.

💡 Planner’s Tip: I always told my clients to think of a longevity annuity not as an investment, but as “longevity insurance.” You are paying a premium to insure against the financial risk of a long and healthy life.

It’s a strategic tool for peace of mind. Whatever they may or may not be worth to you

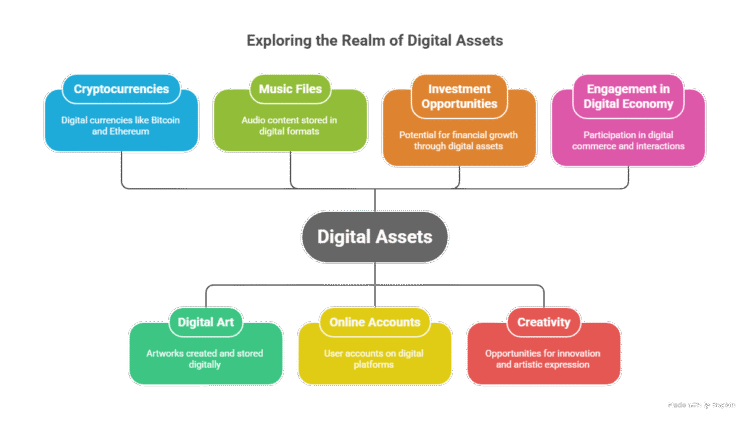

2. Planning for Your Digital Assets

Your estate plan is dangerously incomplete if it only covers your house and your bank account. In today’s world, your digital assets can be incredibly valuable, and without a plan, they can be lost forever.

A 2024 Chainalysis report estimated that billions of dollars in cryptocurrency are inaccessible simply because the owners passed away without leaving instructions for their digital wallets.

What are Digital Assets?

- Cryptocurrencies and non-fungible tokens (NFTs)

- Social media accounts and blogs with potential revenue

- Domain names

- Cloud storage accounts with family photos and important documents

- Any online account with a stored financial value or balance

What to Do Today:

- Create a secure inventory of your digital assets and passwords using a trusted password manager.

- Name a Digital Executor in your will. This is the person you authorize to manage your digital life.

Provide clear instructions for your Digital Executor on how to access and distribute or close down your accounts. This is governed by the Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA), which provides a legal framework for this process.

3. Building Your Behavioral Safeguards

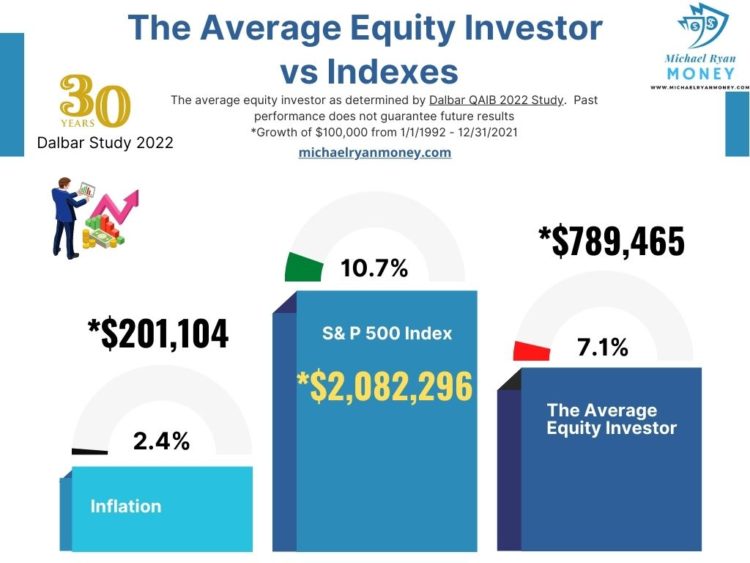

The biggest threat to most retirement plans isn’t a market crash; it’s the investor’s reaction to it. When faced with a downturn, fear can lead to hasty decisions that jeopardize long-term financial security. Therefore, understanding the retirement crisis is crucial for developing a resilient plan that withstands market fluctuations.

Behavioral finance has proven that we are all susceptible to emotional decision-making, like panic selling during a downturn. The annual DALBAR QAIB study consistently shows that the average investor dramatically underperforms the market precisely because they let fear and greed drive their choices.

Your best defense is to build systems that protect you from yourself.

Use “Envelope” Sub-Accounts for Your Budget:

Just as you might have used envelope budgeting to get out of debt, you can use it in retirement. Create separate savings accounts, buckets or “envelopes” for different spending categories (e.g., Travel, Hobbies, Grandkids) and fund them from your automated monthly withdrawal.

When the travel envelope is empty, you stop spending on travel for the month. It’s a simple but incredibly effective way to stick to your retirement budget.

💡 See Where You Stand

Feeling unsure about your progress? A great way to get a data-driven picture of your future is to use a detailed retirement calculator. This tool can help you model different scenarios and see if you’re on track.

Compare a constant-return savings projection with the portfolio estimated to support your retirement spending gap through a selected planning age.

This calculator provides a deterministic educational illustration. It does not predict investment returns, lifespan, inflation, Social Security, pension benefits, taxes, medical costs, long-term-care expenses, or retirement success.

The model assumes the reliable income entered begins at retirement and maintains its purchasing power. Actual Social Security and pension start dates, cost-of-living adjustments, taxes, survivor provisions, and payment rules may differ.

The required-portfolio estimate uses a constant real return and level inflation-adjusted spending through the selected planning age. Actual markets do not produce constant returns, and poor returns early in retirement can materially change sustainability.

Use consistent tax treatment when entering spending and income. Do not compare after-tax spending with gross Social Security, pension, or account-withdrawal amounts without accounting for taxes.

This tool provides general financial education, not individualized financial, investment, tax, legal, Social Security, pension, or retirement-planning advice.

Retirement Funding Gap Projector

Modeled Retirement Funding Comparison

Portfolio Projection in Today’s Dollars

How to interpret this scenario

Important cautions

Assumptions used

The Dangers You Don’t See: Advisor Mistakes & Finfluencer Myths

⚠️ Myth Busted: “You need $5 million to retire.”

This is hyperbole often peddled by finfluencers. The amount you need is deeply personal and based on your expenses. A paid-off house and a frugal lifestyle require far less than a high-cost urban life with a mortgage.

⚠️ Myth Busted: “Dave Ramsey’s 8% withdrawal rule works.”

This is one of the most dangerous pieces of advice. A 2023 Morningstar analysis confirms that assuming you can safely withdraw 8% of your portfolio each year fails in the majority of historical scenarios, dramatically increasing your risk of running out of money.

Continue Learning: Build Your Financial Fortress

Conclusion: Building a Resilient Retirement

The journey to a million-dollar retirement starts with a single step. For you, that step is capturing your full 401(k) match. Do that one thing this week, and you will have already won the most important battle. By blending a prioritized action plan, modern withdrawal strategies, and a healthy skepticism of oversimplified advice, you can build a retirement plan that not only endures uncertainty but empowers you to live your post-career years with confidence and peace of mind. You’ve got this.

Now, try searching for: Roth IRA, 401k match, spousal IRA.

About the Author Michael Ryan is a former financial planner and the creator of MichaelRyanMoney.com. For over 25 years, he has specialized in helping families navigate complex financial challenges to build lasting wealth

Additional resources:

- AARP

- American Savings Education Council

- Certified Financial Planner Board of Standards

- Consumer Federation of America

- The Actuarial Foundation

- U.S. Department of the Treasury

- U.S. Securities and Exchange Commission

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.