You already know a Roth IRA is a powerhouse for tax free growth. But knowing and doing are different. The real challenge isn’t just opening the Roth IRA account. It’s strategically funding it to the legal max, year after year.

Forgetting to max out your Roth IRA is like leaving a winning lottery ticket on the table; a mistake that can cost you hundreds of thousands in tax-free compounded growth by retirement.

In my near 30 years as a financial planner, I’ve seen 2 types of people:

- Those who treat their Roth IRA contribution limit as a hopeful suggestion

- And those who treat their annual IRA savings as a non-negotiable mission.

The difference in their financial outcomes is staggering.

This is your mission playbook. Forget the generic advice. We’ll break down the official 2026 rules, give you the exact financial maneuvers to “find the cash,” and walk you through the advanced Backdoor Roth strategy for high-earners. Including how to sidestep the costly traps I’ve seen derail even savvy investors.

Key Takeaways Ahead

First, The Rules: 2026 Roth IRA Limits

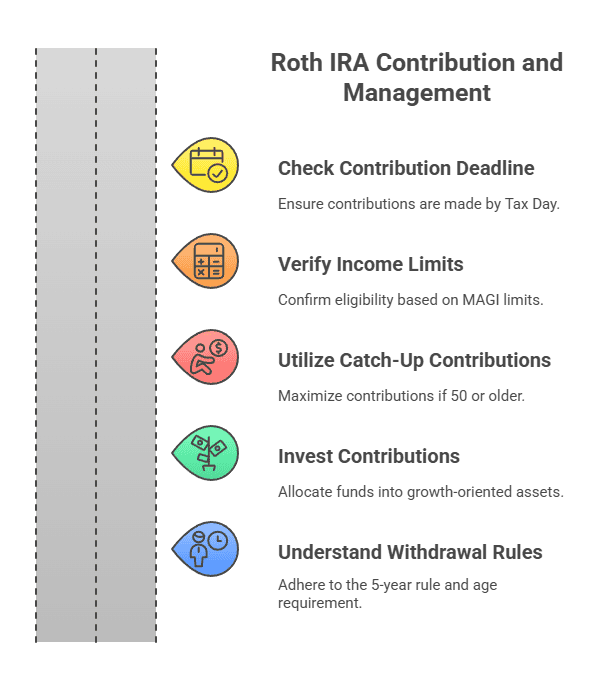

To max out your Roth IRA, you need to know the exact limits. These numbers, set by the IRS, are adjusted periodically for inflation thanks to legislation like the SECURE 2.0 Act.

Here are the official 2026 Roth IRA contribution and income limits you can actually use right now, based on the IRS cost‑of‑living adjustments.

2026 Roth IRA Income Limits

Use your 2026 Roth IRA modified adjusted gross income and tax-filing status to determine whether you may make the full direct contribution, a reduced contribution, or no direct contribution.

| Tax-filing status | Full contribution | Reduced contribution | No direct contribution |

|---|---|---|---|

| Single or head of household | Less than $153,000 | $153,000 to less than $168,000 | $168,000 or more |

| Married filing jointly or qualifying surviving spouse | Less than $242,000 | $242,000 to less than $252,000 | $252,000 or more |

| Married filing separately You did not live with your spouse at any time during 2026. | Less than $153,000 | $153,000 to less than $168,000 | $168,000 or more |

| Married filing separately You lived with your spouse at any time during 2026. | $0 | More than $0 to less than $10,000 | $10,000 or more |

The contribution limit is shared

The $7,500 or $8,600 limit generally applies to your combined traditional IRA and Roth IRA contributions for 2026. It is not a separate limit for each account.

Taxable compensation can lower it

Your maximum IRA contribution is generally limited to the smaller of the annual IRA limit or your taxable compensation for the year, subject to the spousal IRA rules.

MAGI is not simply salary

Roth IRA MAGI starts with adjusted gross income and applies IRA-specific modifications. It may differ from gross income, taxable income, or the amount shown on a pay stub.

The phase-out requires a calculation

Income inside the reduced-contribution range does not automatically permit one fixed amount. Use the applicable IRS worksheet to calculate the reduced limit.

This table addresses regular direct Roth IRA contributions for the 2026 tax year. It does not determine your exact MAGI, taxable compensation, reduced contribution, eligibility for a spousal IRA, or the tax result of a Roth conversion.

Roth IRA contributions are not deductible. Eligibility to deduct a traditional IRA contribution uses different income ranges and workplace-plan rules.

This information provides general financial education, not individualized tax, legal, accounting, investment, or retirement-planning advice. Verify your calculation using current IRS instructions or a qualified tax professional.

2026 Limits (Now Official): The Roth IRA contribution limit is $7,500 if you are under 50 and $8,600 if you are 50 or older (including a $1,100 catch‑up), with income phase‑outs rising to $153,000–$168,000 for single filers and $242,000–$252,000 for joint filers.

The Ground Rules for Contributing to a Roth IRA

There are two non-negotiable rules:

- You (or your spouse, via a Spousal IRA) must have taxable compensation (earned income) at least equal to your contribution amount.

- Your total contribution to all your IRAs (Roth and Traditional) cannot exceed the annual maximum.

The ‘Max Out’ Blueprint: 3 Practical Strategies to Find the Cash

Knowing the limit is easy. Coming up with $7,500 a year in 2026 is the hard part.

Here are three proven financial maneuvers I use with my clients to make it happen automatically.

1. The Automated Monthly Transfer

This is the gold standard for a reason: it works. You turn a big, intimidating goal into a small, invisible habit.

- The Math for 2026:

$7,500 ÷ 12 ≈ $625 per month if you’re under 50.

For the 50+ catch‑up, $8,600 ÷ 12 ≈ $717 per month. Roughly the cost of a nice dinner out each week redirected toward your future self. - The Action:

Set up an automatic, recurring transfer from your checking account to your Roth IRA at a brokerage like Vanguard or Fidelity for the 1st or 15th of every month.

Treat it like your rent or mortgage payment. It’s non-negotiable.

2. The “Bonus & Tax Refund” Lump Sum

If your monthly cash flow is tight, this is your best move. Earmark any financial windfalls (like your annual bonus or tax refund) specifically for your Roth IRA contributions.

Make the full contribution in one lump sum at the beginning of the year to give your money more time to compound tax-free.

3. The “Side-Hustle Siphon”

For those with variable income from consulting or a side gig, this creates order from chaos. Open a separate, free savings account and label it “Roth Funding.”

Set up a rule to automatically transfer 20-30% of every payment you receive from that side-hustle into this account.

When you hit the max contribution limit, transfer the money to your Roth IRA.

The Gateway for High Earners: The Backdoor Roth IRA Playbook

If your income is above the Roth IRA MAGI limits in the table above, the front door to a Roth IRA is closed. It’s time to use the back door.

This is a legal, IRS-sanctioned strategy used by millions of high-earners.

Step 1: Make a Non-Deductible Contribution to a Traditional IRA

First, you contribute to a Traditional IRA. Since your income is high, you likely won’t be able to deduct this contribution from your taxes, which is exactly what we want.

In 2026 you can contribute up to the maximum IRA limit ($7,500 or $8,600 if you’re 50+) using after‑tax money to set up the backdoor Roth.

Step 2: Convert the Traditional IRA to a Roth IRA

Wait for the funds to settle in the Traditional IRA (usually 1-2 business days). Then, contact your brokerage and instruct them to “convert” the entire balance to your Roth IRA.

Since you already paid taxes on the contribution, this conversion is typically a non-taxable event, provided you follow the next step carefully.

Step 3: Report Both Steps on IRS Form 8606

This is the critical compliance step.

When you file your taxes, you must use IRS Form 8606, Nondeductible IRAs. This form documents your non-deductible contribution and the subsequent conversion, proving to the IRS that the converted amount should not be taxed again.

Advanced Play: The Mega Backdoor Roth IRA

For those looking to save even more, the Mega Backdoor Roth is the ultimate strategy. If your 401(k) plan allows for both after-tax contributions and in-service withdrawals, you can contribute up to an additional $72,000 in 2026 (or about that amount depending on your plan’s overall 401(k) limit and employer contributions) into your 401(k). And then convert that after‑tax money to a Roth IRA or Roth 401(k), dramatically increasing your tax‑free retirement funds.

Frequently Asked Questions About Maxing Out Your Roth IRA

What happens if I contribute more than the limit to my Roth IRA?

If you contribute more than your legal limit, it’s called an “excess contribution.” This amount is subject to a 6% penalty tax from the IRS for each year it remains in the account. To avoid the penalty, you must withdraw the excess contribution and any earnings before your tax filing deadline.

What is the absolute latest I can contribute for the 2026 tax year?

The deadline for making your 2026 Roth IRA contribution is the tax filing deadline in 2027, typically April 15th, and you don’t need to file an extension just to use that window.

When making the contribution, your brokerage firm will ask you to specify which tax year it is for.

Can I contribute to a Roth IRA and a 401(k) at the same time?

Yes, absolutely. The contribution limits for IRAs and 401(k)s are separate. You can max out both accounts simultaneously if your cash flow allows, which is a powerful strategy for accelerating your retirement savings.Is there a tax credit for contributing to a Roth IRA?

Your Mission: Make Maxing Out Your Roth IRA Non-Negotiable

Ultimately, the mission to max out your Roth IRA for 2026 is less about financial wizardry and more about disciplined execution. Whether you’re setting up automated monthly contributions to hit the $7,000 contribution limit or executing a strategic Backdoor Roth IRA to navigate the IRS income phase-outs, the objective remains clear: consistently funding this powerful vehicle for tax-free growth.

By understanding the rules, especially the critical pro-rata rule, and integrating this process with your broader 401(k) strategy, you transform a good idea into an unbreakable financial habit.

Your financial future won’t be defined by a single market swing, but by the disciplined systems you build today.

Take the first step this week: choose your funding strategy, automate it, and make hitting your 2026 contribution limit a non‑negotiable part of your financial planning—before lifestyle creep quietly absorbs that $625–$717 a month.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.