Ever wondered how fast you could get your hands on cash if life hit the fan today? If that question makes your stomach drop, you’re not alone.

After decades in the financial trenches, I’ve watched “liquid asset” confusion and poor monetary accessibility ruin more plans than any bear market ever could.

BLS, 2026

gig economy

But this isn’t a lecture. Think of it as your practical, punchy roadmap to cash confidence and understanding your short-term liquidity ratio.

I’ll show you what counts as liquid, what pretends to, and how to use this power so you sleep easy and leap on big opportunities. You can’t pay the plumber with your Picasso, after all.

Take Michael Ryan’s 60-Second Liquidity Check-Up:

Wondering where you stand? Enter your numbers below for a quick snapshot and some straight talk.

Emergency Liquidity & Reserve Check-Up

See how long your readily available reserves could cover essential spending, then build a planning range around your household’s income and risk factors.

Emergency Liquidity Results

Reserve gap or surplus

Funding timeline

Why the planning range moved

Suggested next actions

Questions to resolve

So, What Exactly Is a Liquid Asset? Here’s the Straight Answer

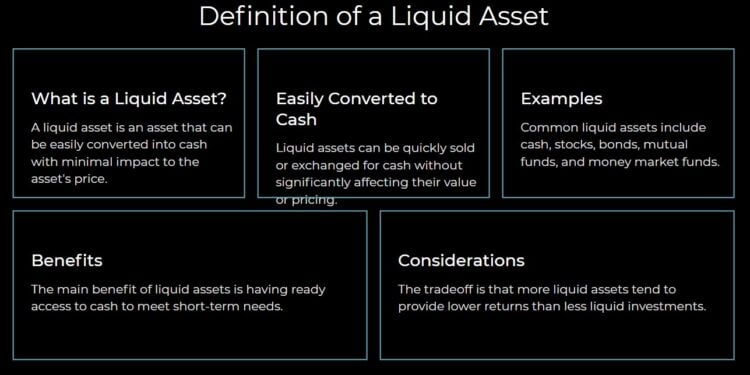

Let me cut the financial fog: A true liquid asset is your emergency escape hatch. Something you can flip into ready cash almost instantly, with no haircut on its value.

Picture the $10K a client of mine, Joanne, pulled from her HYSA in under 30 minutes when her roof caved in during that Florida storm of January 2024. I

f you can’t tap it for full value, fast, it’s not liquid—period. Would you trust a lifejacket with a slow leak?

“Liquidity” is more than speed. It’s about certainty. The “speed” is useless if your asset’s value evaporates in a pinch. This is a key aspect of liquidity risk. The danger that an asset cannot be sold quickly without a substantial price concession.

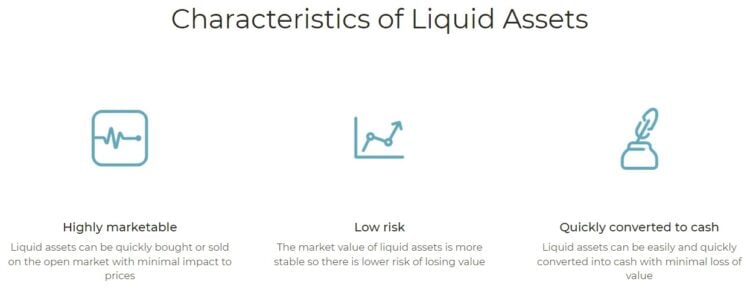

The Golden Trio: Key Characteristics of Truly Liquid Assets

What really makes an asset ready for action?

- Speed of Conversion: Almost immediate or within a few days.

- Minimal Value Loss (Price Stability): You get what it’s worth, no fire sales.

- Established Market & Ease of Access: Simple, straightforward process.

Show Me the Money! Common Examples of Liquid Assets (and Some Surprises)

Don’t sleepwalk through your list: not all “liquid” is equal.

Most Common Liquid Assets (The Real Deal):

- Cash (of course): In hand or in your checking/savings accounts. The ultimate for monetary accessibility.

- Digital checking & savings accounts you can drain on your phone

- And even U.S. Treasury Bills, which

- May 2026

- Money Market Accounts (MMAs) or Money Market Funds (MMFs): Generally reliable, but watch out for those rare institutional freezes during panics.

Did you know they froze redemptions for a handful of institutional clients in 2008 and during the Silicon Valley Bank panic of 2023 - U.S. Treasury Bills (T-Bills) and some other short-term government debt: Very safe and easily sold. One of my business clients used to meet payroll during a regional bank scare.

- Highly Traded Stocks/ETFs (Exchange Traded Funds): These come with a big asterisk. Technically, you can sell Apple shares in seconds, but will you like the price on a market crash day?

Liquid Net Worth & Emergency Reserve Calculator

Compare your readily accessible assets with short-term liabilities, then measure how many months of essential expenses are covered by cash reserves.

Your Liquidity Snapshot

Emergency-reserve comparison

How to read the result

Questions to consider next

This calculator uses the values you enter and does not verify account availability, market value, taxes, settlement time, withdrawal restrictions, insurance coverage, interest rates, or debt terms.

The emergency-reserve calculation includes checking, savings, and the cash-equivalent amount entered. Taxable brokerage investments are included in liquid net worth but excluded from emergency-reserve coverage.

There is no universally correct emergency-fund target. Income stability, dependents, insurance deductibles, health needs, home and vehicle risks, access to credit, and other available resources may justify a different amount.

This tool provides general financial education, not individualized financial, investment, tax, legal, credit, or debt-management advice.

April 2026

Fast isn’t always smart. Liquid isn’t always wise.

Tom learned that the hard way during the COVID market drop in 2020 too; he panic-sold then, missed the rebound, and doubled down on stress.

Hold Your Horses: What’s Not Considered a Liquid Asset?

I once had a client with a Picasso print and a classic Corvette, convinced he was “flush.” He found out the hard way… After three months and four auction attempts, that cool assets are rarely cool cash.

The brutal truth? Most real estate, luxury goods, or collectibles require time, paperwork, and usually a painful discount to move. If your asset can’t bail you out of a Friday afternoon crisis, it’s more trophy than safety net.

Would you accept a Rembrandt as rent?

Classic Illiquids (The “Not-So-Fast” Cash Crew):

- Real estate (your home, rental properties)

- Vehicles (cars, boats)

- Collectibles/fine art (that Picasso, those Beanie Babies)

- Private business shares

- Most retirement accounts like 401(k)s or traditional IRAs (before age 59½, due to penalties and taxes)

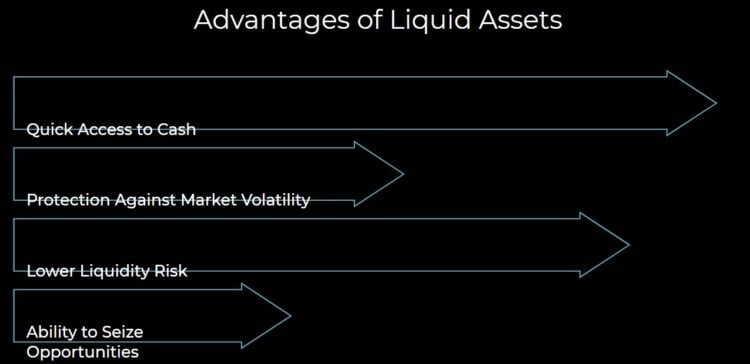

Why Should You Even Care? The Crucial Role of Liquid Assets in Your Financial Life (and Business!)

Back in October 2023, two small business owners I worked with faced the same cash crunch: a freak supply chain shutdown. One survived, the other shuttered. The difference?

A pile of T-bills and cash equivalents on deck for one, while the other tried (and failed) to sell equipment on short notice.

Liquidity is your lifeline. Without it, even profitable businesses can go belly-up. Are you cash-rich, or asset-poor when it counts?

Profit doesn’t equal survival if you can’t manage your liquidity risk.

Your Financial Fire Extinguisher: The Emergency Fund

This isn’t just theory. I’ve seen families glide through layoffs with a 6-month HYSA cushion. While their neighbors scrambled to hock valuables.

This is your cash flow cushion for life’s unexpected moments. Don’t let your life’s work hinge on how quickly you can pawn a painting.

Cash for today. Cash for tomorrow. Cash when the sky falls.

For Your Business: The Lifeblood of Operations

Ask any business owner who’s missed payroll. Liquid assets are oxygen.

SBA data (2024) shows a 33% higher survival rate for companies with 3+ months of cash reserves.

Try making rent with an IOU from your inventory supplier. Effective management of your short-term liquidity ratio is paramount.

Beyond Emergencies: Liquidity for Opportunity and Peace of Mind

The “three to six months” rule is a tired old chestnut.

In 2026, with gig economy volatility and freelance work rising 17% year-over-year (BLS, 2026), I coach clients to calculate liquidity based on actual cash flow gaps. Not some ancient rule.

For some, that’s a year’s expenses; for others, a few weeks with a robust credit line is enough. Cookie-cutter rules are for cookies, not your life.

The Million-Dollar Question (Almost!): How Much Liquidity is “Enough”?

Can you turn your wealth into groceries by Friday?

If not, you’re liquid net worth isn’t enough for your situation.

- Income Stability: Rock-solid or a rollercoaster? (Gig workers need more of a cash flow cushion).

- Dependents: More mouths to feed = bigger safety net.

- Essential Monthly Expenses: What must get paid, no matter what?

- Job Security: One pink slip away from zero, or backed by a strong safety net?

- Business Owners: Analyze cash flow cycles, upcoming capital needs, and payment terms.

I build “Liquidity Ratio Check-Ups” for clients. A living snapshot, updated every 6–12 months. Reflecting the real risks and opportunities in their lives.

Navigating the Waters: Smart Ways to Manage & Optimize Your Liquid Assets

In 2022, I met a couple still hoarding tens of thousands in their checking account “for safety.” Missing out on $2,400 in lost interest just that year because they weren’t taking advantage of HYSA yields.

Sure, inflation’s a quiet thief (especially that 3%+ we saw, per Federal Reserve CPI data), but cash laziness is a mugging in broad daylight.

Use the “Lazy Cash Index” (my term for annual interest lost to inertia) to put a hard number on the cost of complacency.

Want to see your money shrink? Leave it all in checking. Over-saving in cash is just as dangerous as being illiquid.

Michaelryanmoney.com Quick Wins for Optimizing Monetary Accessibility:

- Keep 1–3 months’ “grab-and-go” cash in HYSAs (FDIC/NCUA insured).

- Layer in T-Bills or money market funds for any overflow beyond that immediate cash flow cushion.

- Automate transfers to your savings. Review every life change or at least annually.

- Calculate your “Lazy Cash Index” yearly. (I’m working on a downloadable tool for this – stay tuned!)

Common Myths & Mistakes About Liquid Assets (Michael Ryan Busts Them!)

Let’s clear the air on some dangerous misconceptions.

Myth #1: “My house is a liquid asset because I can get a Home Equity Line of Credit (HELOC).”

Reality Check: A HELOC is debt, not an asset you can readily convert. It’s a loan.

Banks can freeze or reduce HELOCs, especially during economic downturns (we saw this in 2008-2009 and again for several of my clients in 2023 when the economy hiccupped).

A credit line is a promise, not cash in hand. Don’t bank your emergency fund on it.

Myth #2: “All stocks are highly liquid, so they’re great for my emergency fund.”

Reality Check: As Tom’s story illustrated earlier, while stocks are technically liquid, their value isn’t stable.

Selling in a panic during a market crash means locking in losses. Fast isn’t always smart. Liquid isn’t always wise. Don’t let your emergency fund become a hostage of market panic.

Myth #3: “It’s best to keep ALL my savings completely liquid, just in case.”

Reality Check: This is the “cash under the mattress” mentality. While safety is paramount for your emergency fund and short-term cash flow cushion, keeping too much cash beyond your calculated needs means you’re losing to inflation and missing out on long-term growth.

Find your minimum for true monetary accessibility – deploy the rest. Not art. Not cars. Not your cousin’s business. Only cash and its kin count for that immediate safety net.

Calculate your Liquid Net Worth

FAQs: Liquid Asset Real Talk

Is gold a liquid asset?

It’s more “slushy” than liquid. You’ll likely lose some value to dealers and it takes time to find a buyer. Not your first call for an immediate crisis.

Are bonds generally liquid assets?

Short-term Treasuries (T-bills) are very liquid. Some other bonds, like certain corporate or municipal bonds, can be harder to sell quickly without a price hit. It really depends on the specific bond.

How fast is “liquid” in practical terms?

Cash in your checking/savings/HYSA should be accessible the same day. Most major funds or stocks, once sold, take 1-2 business days for the trade to settle and cash to be available.

The Bottom Line: Making Liquid Assets Your Ally, Not Your Afterthought (Michael’s Take)

Liquid assets aren’t an afterthought. They’re your crisis parachute, your chance-taker, your stress antidote.

Liquidity isn’t just about cash. It’s about control. Don’t let lazy rules or wishful thinking leave you exposed. Know your number, use the tools, and let your liquidity work for you—not against you.

What’s your “Lazy Cash Index” this year? How are you managing your liquidity risk? Drop a comment below, I’m always interested in hearing real-world experiences.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.