Ever feel like your credit card rewards are just buying you a cup of coffee when they should be funding a flight? You’re not alone. The simple secret to choosing the best rewards credit card is to match it to your real-life spending, not just the shiniest sign-up bonus.

After 3 decades as a financial planner, I saw countless clients leave thousands of dollars on the table by picking the wrong card for the right reasons. Forget the jargon and analysis paralysis.

We’ll show you how to analyze your spending, calculate a card’s true net value, and sidestep the common traps that drain your points.

This isn’t another generic list of cards. This is the playbook to turn your everyday spending into significant, tangible value.

Key Takeaways of Choosing The Best Rewards Credit Cards For You

- Start with your Spending DNA, not the sign-up bonus — Identify where you spend most today and match it to cards that supercharge those categories. // MUVERA FDE unit

- Run the Annual Fee Litmus Test — Compare total value of rewards and perks against the fee so you know if it’s an investment or a drain.

- Hunt for hidden perks that beat points — Transfer partners, trip protections, and extended warranties can be worth more than flashy earn rates.

- Adapt to 2026’s seismic shifts — FICO® 10T, BNPL reporting, and rewards devaluations demand a smarter, long-term strategy.

Your Guide to Choosing a Rewards Credit Card

The industry is in the midst of a seismic shift. As industry expert So Yeon Chun from INSEAD explains, issuers are preserving the “appearance of program stability while quietly reducing average value.” They are banking on your confusion to maintain their profit margins.

But what if you had a simple, powerful system to cut through the noise? A method that not only finds the right card for your real life but also arms you against the game-changing shifts happening right now in 2026?

Let’s find the card that pays you for a change.

⚠️ A Crucial Money Warning From Michael Ryan Money:

Before we continue, one rule is non-negotiable. If you currently carry a credit card balance, a rewards card is NOT for you. The interest you pay, often 20% or more, will always cost more than any rewards you earn. Your absolute first priority should be a low-interest or 0% intro APR card to aggressively pay down that debt. This guide is for users who commit to paying their balance in full every single month.

What Are Rewards Cards and How Do They Really Work?

At its core, a rewards credit card gives you a small rebate on your spending, funded by the “interchange fees” banks charge merchants for every transaction. These rebates come in three main flavors:If this is all new to you, I wrote a beginners guide to Cash Back Credit Card Rewards programs that may be a great start for your journey.

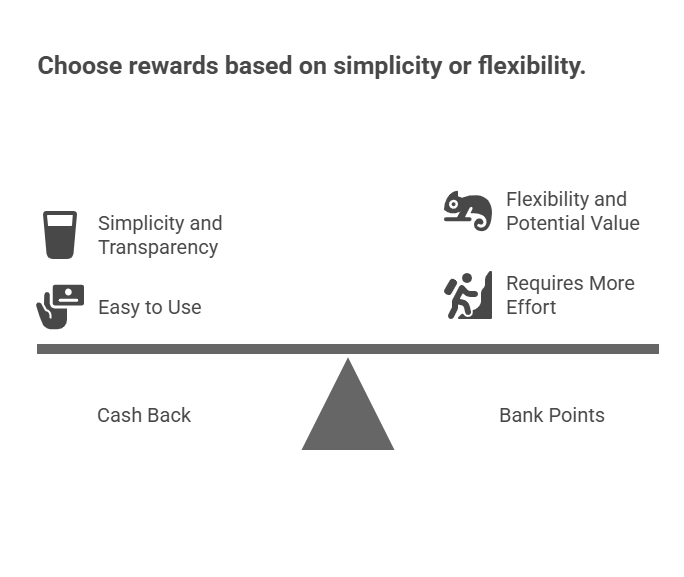

Cash Back: The Simplest Return

You spend money and get a direct percentage back, usually as a statement credit. It’s simple, transparent, and easy to use.

Bank Points: The Flexible Currency

Think of these as a proprietary currency from a bank (e.g., Chase Ultimate Rewards®, Amex Membership Rewards®). Their value can be amplified significantly when transferred to airline and hotel partners. This offers the highest potential value but requires more effort.

Co-branded Miles: The Loyalist’s Choice

These are points tied directly to a specific airline or hotel brand (e.g., Hilton Honors, Marriott Bonvoy). Best for those who are loyal to one company for their travel needs.

- Consistent cash-back rewards can be a powerful, passive way to build up your savings or add to your liquid assets without changing your spending.

The Spending DNA Match System™: Your 3-Question Framework

To avoid the common traps, you must start with strategy, not with a card.

1: What is my primary spending DNA? (The Habit Match)

Look at your last three months of bank and credit card statements. Be honest about where your money actually goes. Your goal is to find a card that gives you supercharged rewards on what you’re already doing, not what you aspire to do.

📘 Client Story: The “Aspirational Spending” Trap

I once worked with ‘David,’ a young engineer with the AmEx Platinum. He dreamed of global travel, but his family’s budget was dominated by groceries, gas, and takeout. He was earning just 1 point per dollar on 80% of his spending. We switched him to the AmEx Blue Cash Preferred®, and he immediately started earning 6% on groceries and 3% on gas. He gave up the “status” but gained over $800 in real cash at year’s end.

- For the Frequent Traveler:

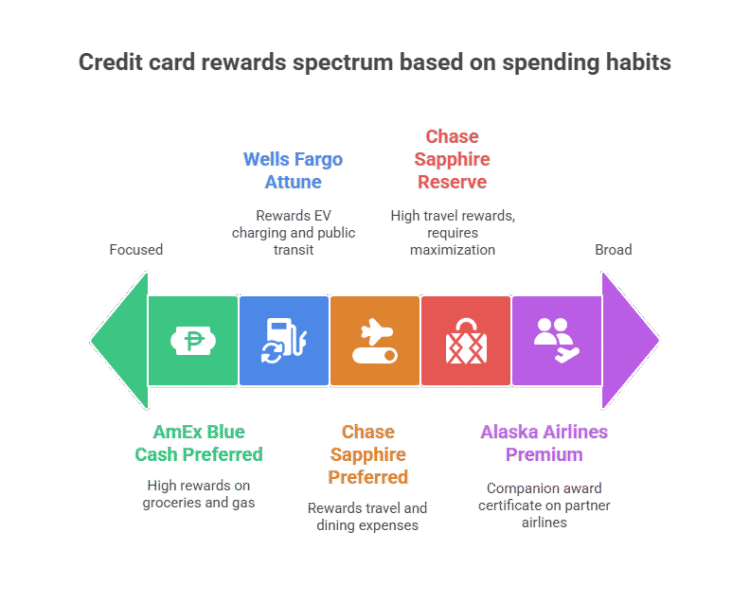

Your DNA is flights and hotels. A premium travel card like the Chase Sapphire Preferred® Card is a natural fit. - For the Homebody & Family:

Your DNA is groceries, gas, and streaming. A cashback card like the Blue Cash Preferred® Card from American Express is a powerhouse. - For the Modern Commuter & Conscious Spender:

New-in-2026 cards like the Wells Fargo Attune℠ Card target modern DNA, offering 4% cash back on EV charging, public transit, and even thrift stores, with no annual fee.

2: Is this annual fee an investment or a tax? (The Litmus Test)

An annual fee is only a bad deal if you don’t get more value in return. Calculate the card’s Net Annual Value.

Formula:

(Total Value of Rewards Earned + Value of Perks Used) - Annual Fee = Net Annual Value

Let’s test this on a high-stakes example: The Chase Sapphire Reserve®, which increased its fee to a staggering $795 in June 2025.

📘 Client Story: Making a $795 Fee a Bargain

My client ‘Maria,’ a consultant who travels twice a month, was shocked by the new fee. We did the math. Her ~$15k in annual travel/dining earns 3x points. With Chase’s new 2 cents/point “Points Boost” on select bookings, that’s $1,800 in travel value. Add the easy-to-use $300 annual travel credit, and she gets $2,100 in value. For her, the $795 fee is a fantastic investment. But as NerdWallet’s Funto Omojola wisely notes, you must “put in a lot of work” to maximize it. For a non-traveler, this fee is a disaster.

3: Where is the hidden value? (The Perk Hunt)

Often, the best benefits aren’t the points.

Transfer Partners: The Value Multiplier

This is the most important “hidden” perk. Transferring points from Chase, Amex, or Capital One to an airline partner (like Hyatt or Air Canada) can turn a $500 value into a $2,000 business class seat. This is the secret to outsized value.

Game-Changing Perks

As of August 2025, the new Alaska Airlines Premium Card exemplifies this. It’s launching with a Global Companion Award Certificate valid on partner airlines—a unique feature that could save a traveling couple thousands, making its $395 fee a potential bargain.

Critical Insurance Protections

Look for trip cancellation insurance, primary rental car insurance (so you can decline the expensive coverage at the counter), and extended warranty protection. These are practical benefits that save you real money.

Michael Ryan Moneys Best Credit Card Rewards Programs in 2026

Ready to Put the Framework into Action? Top Reards Cards for Different Spending DNAs

You now have the exact strategic questions I used with my clients for over 25 years. To make it even easier, I’ve built this simple tool that uses the same logic to give you a personalized starting point in under 30 seconds.

Your Personal Credit Card Finder

Stop the analysis paralysis. Answer two questions from my 25 years of experience to find the card that fits your real life.

Did you get your result?

Your recommendation is a fantastic starting point, grounded in the timeless principles of matching a card to your real life. But the credit card game is changing fast. Before you apply, it's critical to understand the major shifts happening in 2026 that could affect your strategy...

Best Rewards Cards by Category (Real User Data, 2026)

🏆 Overall Best Rewards Card — Chase Sapphire Preferred® Card

- Why it stands out:

75,000-point welcome bonus after meeting minimum spend; Chase Ultimate Rewards® points transfer 1:1 to premium travel partners like Hyatt, Air Canada Aeroplan, United MileagePlus®, and Singapore KrisFlyer. - User win stories:

The Points Guy editor redeemed 100,000 transferred points for a Lufthansa first-class ticket valued at over $8,000. - Key benefits:

- $95 annual fee with premium perks.

- Broad travel protections, primary rental car insurance, and trip cancellation coverage.

- Consistently rated #1 best travel credit card by multiple review sites and forums.

- Apply now: Get the Chase Sapphire Preferred® Card

💰 Best Cash Back Card — Blue Cash Preferred® Card from American Express

- Why it shines for families:

6% cash back at U.S. supermarkets (up to $6,000/year), 6% on U.S. streaming services, 3% at U.S. gas stations and transit. - Real-world match:

Perfect for households that prioritize groceries, utilities, and family streaming over travel redemptions. - Extra perks:

Amex Offers (my personal favrite program!!!), purchase protection, and return protection for everyday purchases. - Apply now: Get the Blue Cash Preferred® Card

🆓 Best No Annual Fee Rewards Card — Chase Freedom Unlimited®

- Why it’s flexible:

Earn 1.5% cash back on all purchases, plus 5% in rotating quarterly bonus categories (up to $1,500 per quarter). - Hidden power:

Points can be combined with Sapphire Preferred® or Sapphire Reserve® for transfer to airline and hotel partners. - Perfect fit:

Those wanting everyday simplicity without a fee but with upgrade potential. - Apply now: Get the Chase Freedom Unlimited®

⛽ Best Gas Rewards Card — Citi Strata Premier® Card

- Why it’s underrated:

Earns strong rewards in gas station purchases, plus bonus categories for travel, dining, and supermarkets. - Ideal for:

Drivers and commuters who want higher gas rewards than most general travel cards offer. - Apply now: Get the Citi Strata Premier® Card

🚫 Most Overhyped Card — Chase Sapphire Reserve®

- Why it misses the mark for most:

$795 annual fee (as of 2025) with value requiring heavy travel spending and multiple credits to justify. - Real-world feedback:

You must “put in a lot of work” to maximize benefits. Most users find the Sapphire Preferred® delivers 80% of the value for a fraction of the cost. - Better alternative: Chase Sapphire Preferred® Card

Master Your Finances, One Skill at a Time

Now that you know how to analyze your spending, get more actionable money moves like this delivered straight to your inbox.

💡 2026 Reality Check:

- Sign-up bonuses are shrinking and redemption rules tightening.

- Banks are reducing benefits while maintaining the appearance of stability.

- Your strategy: Choose cards that match your actual spending patterns — not aspirational ones — to maximize real-world value.

The Hidden Seismic Shifts of 2026 You Cannot Ignore

Advice from last year for credit card rewards programs is already dangerously outdated. I mean, I'm sure you noticed, right? Every other website you visited - they all pitched you the same old, outdated advice. And the same cards over and over again - based on who pays them the highest affiliate commissions.

1. The FICO® Score Revolution: "Buy Now, Pay Later" Now Counts

Starting in Fall 2025, the new FICO® 10T score will incorporate your Buy Now, Pay Later (BNPL) payment history for the first time. This affects over 90 million Americans who have used services like Afterpay or Klarna.

⚠️ Expert Warning: A Looming Credit 'Catastrophe'

Credit expert Micah Smith warns this could cause a "dramatic decrease in credit scores." With 43% of BNPL users admitting to late payments, millions who saw these as consequence-free loans could see their credit damaged. Every BNPL decision is now a credit decision.

2. The Great Rewards Devaluation: Getting Less for More

Issuers are tightening the screws. Why? Pressure on interchange fees and a saturated market mean they are focusing on profitability.

- American Express Gold Card:

The 4x points on restaurant spending is now capped at $50,000 annually. - Chase Sapphire Preferred®:

The long-standing 1.25 cents per point redemption value in the travel portal has been replaced with a 1 cent base value, supplemented by a new 'Points Boost' feature for select bookings. This fundamentally changes its value calculation for non-strategic users. - Industry-Wide Trend:

Banks are making it harder to earn and redeem, quietly reducing the value for all but the most strategic users.

3. The End of Easy "Churning"

"Churning", rapidly opening cards for bonuses, is getting much harder.

- Chase's "5/24 Rule":

You will likely be denied most Chase cards if you've opened 5 or more personal credit cards (from any bank) in the last 24 months. - Amex's "Once Per Lifetime" Rule:

You can typically only earn a welcome bonus on a specific Amex card once. - Stricter Timelines:

24-48 month exclusion periods for new bonuses on the same card are now the industry norm.

Which Rewards Credit Card is Right For You? Frequently Asked Questions (FAQ)

Do rewards credit cards hurt your credit score?

Opening any new credit card can cause a small, temporary dip in your credit score due to the "hard inquiry." However, over the long term, a new card can actually help your score by increasing your total available credit and lowering your overall credit utilization ratio, provided you use it responsibly and pay your bills on time.

Is it better to get cash back or travel points?

This depends entirely on your lifestyle. Cash back is simple, flexible, and never expires. Travel points can offer a higher value per dollar spent if you are a frequent traveler who can strategically redeem them for flights or hotels. For most people, a straightforward cash-back card is the more practical and consistently valuable choice.

How many rewards credit cards should I have?

There is no magic number. For most people, having two to three cards is a manageable strategy. This allows you to have a primary card for most purchases and one or two others to maximize rewards in specific categories where you spend a lot, like groceries, gas, or dining. The key is to only have as many as you can manage

Master Your Finances, One Skill at a Time

Now that you know how to analyze your spending, get more actionable money moves like this delivered straight to your inbox.

Michael Ryan Money Credit Card Rewards Checklist & Next Steps

Final Checklist Before You Choose

- [ ] I analyzed my last 3 months of spending using the Spending DNA Match System™.

- [ ] I ran the Net Annual Value calculation for any card with an annual fee.

- [ ] I checked the card’s transfer partners and insurance perks to confirm they fit my life.

- [ ] I commit to the golden rule: paying the balance in full every single month.

- [ ] I have a plan to meet the sign-up bonus with my normal, budgeted spending.

Ready to Take Control? Download Your Worksheet

Feeling empowered? To make this even easier, download our free [Rewards Strategy Worksheet] to walk through these steps and find your perfect card today. (This would be a link to a PDF).

What to Read Next

Next Steps for Choosing Your Best Rewards Credit Card

Choosing the right rewards card isn't about finding a magic bullet; it's about holding up a mirror to your own spending habits. You now have the framework to move beyond flashy sign-up bonuses and calculate the true net value of any card in your wallet.

After years of advising people, I can tell you the greatest feeling isn't just getting a "free" flight—it's the quiet confidence of knowing your financial tools are actively working for you month after month.

Don't let the analysis stop here. Continue scrolling to explore our related guides on mastering your credit and building wealth. For more practical, experience-backed insights delivered straight to your inbox, sign up for our newsletter and never miss a beat.

Explore next steps like: 'using transfer partners', 'business card strategies', or 'paying down debt'.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.