So, the Venmo app is dangling its credit card in front of you, and you’re tempted. But before you agree to that “hard pull” on your credit report, you have one crucial question that will determine if it’s even worth it:

Am I going to get a useful credit limit, or just a token $500 that won’t even cover a grocery run?

Let’s cut through the usual “it depends” nonsense. You need real numbers to manage your expectations.

While the issuer, Synchrony Bank, has the final say, here’s the evidence-based answer: The Venmo Credit Card comes with a guaranteed minimum starting limit of $250 for anyone approved.

Planning a big purchase on your new Venmo card but worried you might hit a surprisingly low limit? You’re not alone.

However, real-world data from Credit Karma shows the average limit is a much healthier $4,159, with approvals reported as high as $30,000 for top-tier applicants.

Where you’ll land in that wide range is what we need to figure out. Let’s break down the data so you can apply with confidence.

TL;DR: Key Takeaways

- The Average Limit is Higher Than You Think: While the guaranteed minimum is just $250, with some approvals reaching as high as $30,000.

- Your FICO Score is the Key: Your approval odds and limit size are strongly tied to your credit score. The article below breaks down the specific score ranges that typically get a $2.5k, $7.5k, or $15k+ starting limit.

- You Can “Test Drive” Your Approval: The application starts with a “soft pull” that won’t hurt your credit score. This allows you to see your potential approval and limit before you commit to the hard inquiry that impacts your credit.

- It’s a Real Bank Making the Decision: The card is issued by Synchrony Bank. They care more about your credit history and income than how often you use Venmo.

Key Takeaways Ahead

What Starting Limits Are Venmo Users Actually Getting?

Forget marketing fluff. The best way to gauge your chances is to look at what real people are getting. After analyzing dozens of self-reported data points from myFICO forums and Reddit, a clear pattern emerges for the Venmo Credit Card.

| Applicant’s FICO Score | Typical Reported Starting Limit |

|---|---|

| 670 – 699 (“Fair”) | $500 – $2,500 |

| 700 – 749 (“Good”) | $2,500 – $8,500 |

| 750+ (“Excellent”) | $9,000 – $25,000+ |

Some users report truly surprising results. One applicant received a $25,000 limit, calling it their highest starting limit ever. Another, just six months after a bankruptcy discharge, was approved for $17,000, which shows Synchrony Bank heavily values income and recent credit behavior.

Read my full Venmo Credit Card Review here

The Key Factors That Synchrony Bank Cares About

As a financial planner, I can tell you that banks don’t just pull a number out of a hat. Synchrony is looking at a few key metrics to decide how much credit to extend to you.

- Your Credit Score:

This is the gatekeeper. While some users report approvals in the 640-670 range, your odds increase dramatically with a score above 670. Aiming for 700+ puts you in a much stronger position. - Your Reported Income:

This is straightforward. Higher income demonstrates a greater ability to handle payments, leading to higher limits. The average income for approved users is just over $96,000. - Your Credit Utilization:

This is the silent killer of high credit limits. It’s the percentage of your existing credit you’re currently using. If your other credit cards are maxed out, you look like a risk, and your starting limit will be lower. To improve your odds, learn how to hide your credit utilization by paying down balances before your statement closing dates.

Credit Utilization Calculator & Worksheet

Enter your credit card balances and limits to see your utilization ratios.

See an issue or have a suggestion? We'd love to hear from you!

💡 Advisor Tip:

Your credit utilization makes up 30% of your FICO score. Before you apply for the Venmo card, pay down the balances on your other credit cards to get them below 30% utilization. This is the single fastest way to look better to the underwriting algorithm.

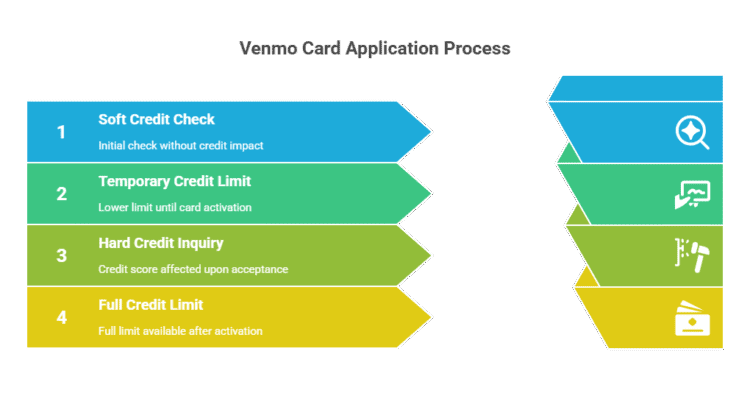

Important Venmo Application Details You Need to Know

The Venmo card application process has a few quirks you should be aware of.

The “Soft Pull” Pre-Approval

The initial application is a soft credit check—in other words, it does NOT affect your credit score. You can see if you’re likely to be approved without any risk. Only if you accept the offer will Synchrony Bank perform a hard inquiry, which is the part that dings your score by a few points temporarily. This is a fantastic, pro-consumer feature.

The Temporary Limit Upon Approval

This is a big one that confuses people. Upon approval, you may be given a temporary, lower credit limit for immediate use within the Venmo app. One user reported getting an $8,500 approval, which showed as a $2,000 temporary limit until he received and activated the physical card a few days later. Don’t panic if this happens; your full limit will be available once the physical card is active.

Venmo Account Requirement

To apply, you must have a Venmo account that has been open and in good standing for at least 30 days. You can’t just sign up for Venmo and immediately apply for the credit card.

Got a Low Veno Limit? Here’s How to Increase It.

Look, getting a low starting limit isn’t a life sentence. It’s a starting point. I had a client, “Mark,” a 24-year-old graphic designer who was frustrated when he got approved for a Venmo card with only a $1,500 limit. We put a simple 6-month plan in place.

- He used the card for one recurring bill (his Netflix subscription) and nothing else.

- He set up autopay to pay the statement balance in full every single month.

- After six months of perfect payment history, he used the “Request Credit Limit Increase” button in the app.

The result? They bumped his limit from $1,500 to $4,000. It’s not magic; it’s just demonstrating responsible behavior over time.

Your Next Steps

Getting approved for a new card is a financial milestone. Your starting limit doesn’t define your creditworthiness—it’s just your starting line. Use the card responsibly, pay it off every month, and it will grow with you.

Want to see how your current credit habits stack up? Use our free Credit Utilization Calculator to see your ratio in seconds and find out if it’s helping or hurting your score.

Venmo Payment Not Showing Up In Bank Account

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.

an attractive option for those who want to pay with the convenience and security of their credit card. Here are just some of the advantages: