College costs have absolutely exploded in recent years. I’m talking about a 25%-30% increase in just ten years. Insane, right? Look, I know that sounds scary, but I’ve got some real strategies to help you navigate choosing the right college savings accounts for your kids.

Imagine this: Your kid gets accepted to their dream school. Instead of panicking about the cost, you can actually tell them, “We’ve got this covered.” That’s an incredible feeling.

Now, I’m not just talking out of my hat here. I’ve been in your shoes – twice! As a dad with two kids in college and a retired financial planner, I’ve learned a thing or two about saving for college.

There are several different ways to save for college, and honestly, it’s like picking the right tool for the job. You’ve got 529 Plans, Coverdell ESAs, Custodial Accounts, even Roth IRAs. Don’t worry if that sounds confusing. I’m going to break it all down for you.

I’m going to walk you through each option. I’ll show you how to maximize your savings and cut your tax bill. Plus, how all this affects financial aid (which is critical).

College Savings Quiz

College Savings Quiz

Q1: What is the current average annual cost of college tuition, room, and board in the U.S.?

Q2: At what age should saving for college ideally start?

Ready to stop stressing about those tuition bills? Let’s get started.

Key Article Takeaways: Choosing A Savings Account For Your Kids College

- What should I consider when choosing a college savings account? When selecting the right account, consider your overall financial goals, the need for liquidity, and the potential tax benefits that apply in your state.

- What are the main types of college savings accounts?

College savings accounts include 529 Plans, Coverdell ESAs, and Custodial Accounts, each designed to meet different educational savings needs. - How do 529 Plans benefit families? 529 Plans provide tax-free growth and withdrawals for qualified education expenses, making them a favored option for many families.

- What are the limitations of Coverdell ESAs? Coverdell ESAs permit contributions of up to $2,000 per year, but they have income limits and must be utilized before the beneficiary turns 30.

- How do Custodial Accounts affect financial aid? Custodial Accounts (UGMA/UTMA) are classified as the student’s assets, which can greatly influence their eligibility for financial aid.

College Savings Calculator

College Savings Calculator

- Rising College Costs: A report indicates that the average cost of college tuition has been increasing steadily, outpacing inflation and family income growth. This trend underscores the importance of early and strategic saving.

- How expensive is college? According to the College Board, the average cost of tuition and fees for the 2025-2026 academic year ranges from $11,950 for in-state public schools to $45,000 for private schools.

- Student Debt Impact: Research, like this comprehensive study, reveals the significant impact of student debt on graduating young adults, affecting their financial independence and life choices. This underscores the need for effective college savings strategies to minimize debt.

Quick Links: Types of College Savings Accounts

Understanding Types of College Savings Accounts And Plans

Planning for your kid’s education can be overwhelming. Trust me, I get it. But understanding your savings options makes this whole thing a lot simpler. You’ve basically got three main choices: 529 Plans, Coverdell ESAs, and Custodial Accounts. Each one has its own pros and cons.

Each option has different benefits, from tax-free growth to how flexibly you can use the money. I’ll get into the details in a minute, but first, here’s a quick comparison:

College Savings Accounts

Compare College Savings Accounts

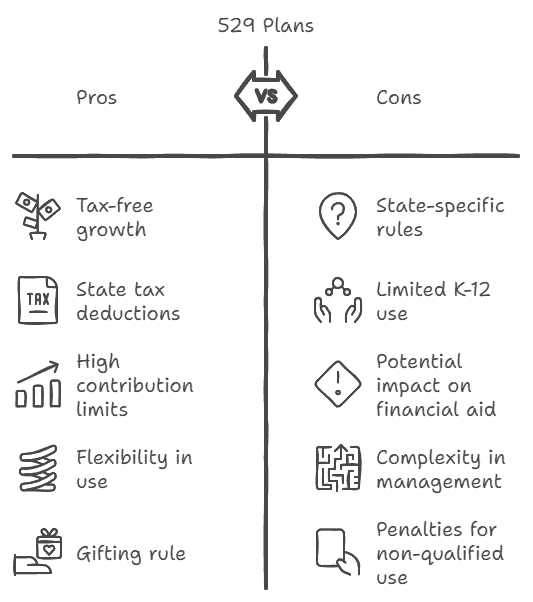

529 Plan

Contribution Limit: Varies by state (up to $450,000+)

Tax Benefits: Tax-free growth, state tax deductions

Primary Use: College, K-12 (some states)

Flexibility: Can change beneficiary; broad education uses

Coverdell ESA

Contribution Limit: $2,000

Tax Benefits: Tax-free withdrawals

Primary Use: K-12 and college expenses

Flexibility: Must use by age 30; income limits apply

Custodial Account

Contribution Limit: No limits

Tax Benefits: Gains taxed at child’s rate

Primary Use: Any purpose after age 18

Flexibility: Flexibility beyond education; may impact financial aid

I’ll walk you through each of these accounts and how they affect financial aid eligibility, but this table gives you a quick snapshot of the differences.

529 College Savings Plans: Flexibility and Tax-Free Growth

When it comes to saving for college, 529 Plans are a popular choice for families due to their tax advantages and flexibility. Let me tell you why I often recommend this option first.

Contributions grow tax-deferred, meaning you won’t pay taxes on any investment growth as long as the funds are used for qualified education expenses. Withdrawals are also tax-free when used for things like tuition, books, and even certain K-12 expenses (depending on your state). Plus, many states offer tax deductions or credits for contributions to their 529 plans—so you’re not only saving for college but also lowering your state tax bill.

- If you want to know more about 529 Plans, feel free to read my guide on Everything You Need To Know About 529 Plans here.

- Answers to Your Most Important 529 Plan College Savings Plan Questions

I’ve seen this work well for families, especially when they take advantage of the high contribution limits—some states allow lifetime contributions up to $500,000. Grandparents can even contribute using a special gifting rule that lets them donate up to $95,000 per individual ($190,000 for married couples) in one year without triggering gift taxes.

Later, I’ll explain how these plans affect financial aid eligibility, but for now, just know that funds in a 529 Plan are considered parental assets, which generally have a smaller impact on financial aid compared to other accounts.

| 529 Plan Features | Details |

|---|---|

| Tax Benefits | Tax-free growth, state tax deductions |

| Contribution Limits | Varies by state, up to $450,000+ |

| Flexibility | Can be used for college, K-12 (limited), or vocational programs |

| Gifting Rule | Up to $95,000 per individual ($190,000 married couples) without gift tax under 5-year rule |

- Read more here about the Florida 529 Plans, perhaps the most popular plan in the country.

- Or this article about 19 Ways to Pay For College and Higher Education

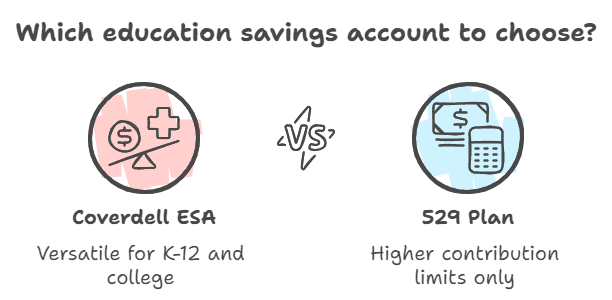

Coverdell Education Savings Account (ESA) Versatility for Education Expenses

If you’re seeking flexibility beyond just college, the Coverdell Education Savings Account (ESA) might be an excellent optionparticularly for covering K-12 expenses. With a Coverdell ESA, you can withdraw funds tax-free for both K-12 and higher education expenses. Offering you more versatility than a 529 Plan.

However, there are some limitations to keep in mind. Contributions are limited to $2,000 per year. And there are income restrictions to consider. Also, the funds must be used before the beneficiary turns 30, or they could face penalties.

| Coverdell ESA Features | Details |

|---|---|

| Contribution Limit | $2,000 per year |

| Income Restrictions | Single filers: $110,000; Married: $220,000 |

| Qualified Expenses | K-12 and college expenses |

| Use of Funds | Must use by age 30 |

We’ll discuss more about income limits and penalties in a later section. But for now, the key takeaway is that Coverdell ESAs are perfect if you want to save for more than just college. However the lower contribution limit can be a disadvantage for some families.

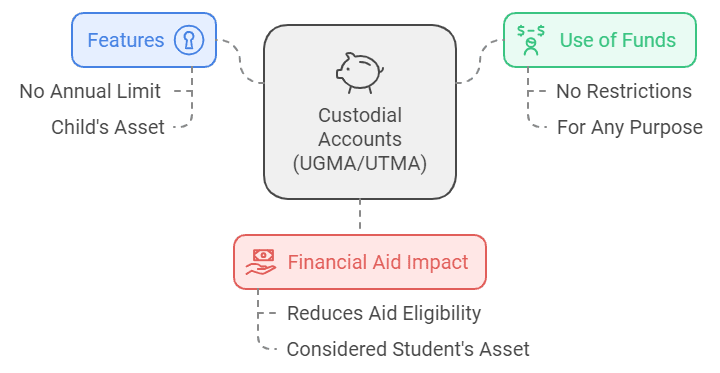

Custodial Accounts (UGMA/UTMA): Beyond Education Saving Funds

Custodial Accounts (UGMA/UTMA) differ from 529 Plans or Coverdell ESAs in that they allow savings for purposes beyond just education. These accounts let you save on behalf of your child, and once they reach adulthood (typically age 18 or 21, depending on the state), they take full control of the funds.

While this flexibility can be appealing, it’s important to note that custodial accounts are considered the child’s asset, which can significantly reduce their eligibility for need-based financial aid. I’ve seen families get caught off guard by this, so it’s an important factor to keep in mind.

| Custodial Account Features | Details |

|---|---|

| Contribution Limit | No annual limit |

| Use of Funds | No restrictions—funds can be used for anything |

| Financial Aid Impact | Considered the student’s asset, affects aid eligibility |

Choosing the right education savings vehicle requires balancing flexibility with financial aid considerations. Understanding how different account types impact your FAFSA eligibility and Expected Family Contribution (EFC)—from 529 Plans and Coverdell ESAs to custodial accounts and traditional savings—helps you maximize both education funding and potential financial aid opportunities for your family.

| Type of Account | FAFSA Impact |

|---|---|

| 529 Plans | Considered a parental asset if the parent is the account owner. This means it has a lower impact on financial aid eligibility (up to 5.64% of the asset’s value is considered in the EFC – Expected Family Contribution). |

| Coverdell Education Savings Accounts (ESAs) | Similar to 529 Plans, if the parent is the account owner, it’s treated as a parental asset. Thus, it has a relatively lower impact on financial aid eligibility. |

| Custodial Accounts (UGMA/UTMA) | Considered a student asset. This has a higher impact on financial aid eligibility (20% of the asset’s value is considered in the EFC). |

| Savings Bonds (if in the student’s name) | Treated as a student asset, thus having a higher impact on financial aid eligibility. |

| Traditional Savings Accounts | If in the parent’s name, it’s treated as a parental asset. If in the student’s name, it’s considered a student asset and has a higher impact on financial aid. |

Structure your education savings strategically by using parent-owned 529 Plans or Coverdell ESAs to minimize FAFSA impact while building funds for your student’s future education.

Financial Aid Impact and Tax Considerations

One of the key factors to think about when selecting a savings account is its potential impact on your child’s future financial aid. As I mentioned before, funds in 529 Plans are classified as parental assets, which typically have a lesser effect on financial aid compared to custodial accounts.

But that’s not all—there are also tax advantages to consider, which can play a huge role in maximizing your savings.

Selecting the optimal education savings strategy requires comparing how different account types affect financial aid eligibility and tax efficiency. Understanding the distinctions between 529 Plans, Coverdell ESAs, and custodial accounts—in terms of FAFSA impact and tax treatment—enables you to build the most advantageous savings plan for your family’s education funding goals.

| Account Type | Impact on Financial Aid | Tax Treatment |

|---|---|---|

| 529 Plan | Minimal impact as a parental asset | Tax-free growth; state tax deductions available |

| Coverdell ESA | Considered a student’s asset, high impact | Tax-free withdrawals for qualified education expenses |

| Custodial Account (UGMA/UTMA) | High impact as a student asset | Gains taxed at child’s rate; no restrictions on use |

Prioritize parent-owned 529 Plans to balance tax advantages with minimal financial aid reduction, ensuring maximum flexibility and savings efficiency for education expenses.

In the following section, I’ll walk you through a detailed process for opening these accounts. I will include tips on how to maximize your contributions and reduce your tax liabilities

- Learn more in this article about different types of student loans

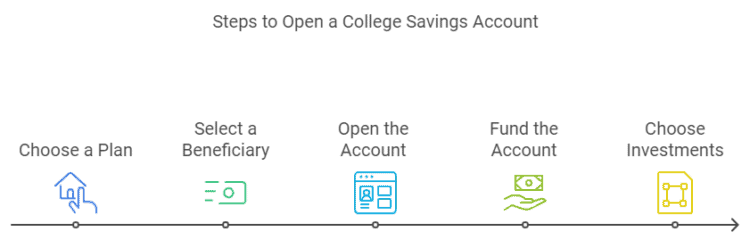

Steps to Open a College Savings Account

Opening a college savings account is simpler than you might expect. Here’s a guide to help you set up a 529 Plan or Coverdell ESA:

Step-by-Step: Opening a 529 Plan

Most plans provide a variety of options, including mutual funds and age-based portfolios.

- Choose a Plan: Research direct-sold and advisor-sold plans. Pay attention to state tax benefits, fees, and available investment options.

- Select a Beneficiary: Usually, this will be your child, but you could change the beneficiary later if necessary.

- Open the Account: Most accounts can be opened online with some basic personal details.

- Fund the Account: start with an initial deposit and consider setting up automatic contributions to simplify your saving process.

- Choose Investments: Most plans provide a variety of options, including mutual funds and age-based portfolios.

Step-by-Step: Opening a Coverdell ESA

- Select a Financial Institution: Find one that has low investment expenses and a wide range of investment options.

- Gather Information: You’ll need the beneficiary’s Social Security number and date of birth.

- Open the Account: This can typically be done online or in person at a bank or brokerage firm.

- Fund the Account: Keep in mind the $2,000 annual contribution limit—other family members can also contribute.

- Understand Withdrawal Rules: Funds must be used for qualified expenses, and all funds should be utilized by the time the beneficiary turns 30.

By following these steps, you’ll be on your way to creating an education fund that meets your family’s needs. Later, I’ll offer expert tips on which account might be the best fit for your unique situation.

Choosing the Right College Savings Plan for Your Needs

Selecting the ideal college savings plan is crucial and requires careful assessment of your financial situation, long-term goals, and the urgency of accessing funds. With rising education costs, understanding the available financial tools empowers you to make informed decisions. Here are some prominent options to consider:

- 529 Qualified Tuition Programs: These state-sponsored investment plans allow for high contribution limits and offer significant tax benefits on growth, making them ideal for families planning for college expenses.

- Coverdell Education Savings Accounts (ESAs): Versatile accounts that can cover educational expenses from kindergarten through college, providing tax-free withdrawals for qualified costs.

- Uniform Transfers to Minors Act (UTMA) / Uniform Gifts to Minors Act (UGMA) Accounts: Custodial accounts that allow adults to save for minors, offering flexibility in fund usage once the child reaches adulthood, though they may impact financial aid eligibility.

- Roth Individual Retirement Accounts (IRAs): Primarily for retirement, these accounts can also be used for educational expenses, but doing so may affect your long-term retirement strategy.

Expert Financial Tips

- Maximize Benefits: 529 Plans are often recommended for their favorable tax treatment and high contribution limits.

- Utilize Coverdell ESAs: These accounts are particularly useful for covering educational costs before college due to their flexibility.

- Consider UTMA/UGMA Accounts: While they broaden investment options, be mindful of their potential impact on financial aid eligibility.

- Exercise Caution with Roth IRAs: Use them for education judiciously, as it may influence your retirement planning. Learn more in this article to find out if you should use a Roth IRA to fund your college savings

Key Evaluation Factors

When choosing a college savings plan, consider:

- Financial Goals: Assess how your savings strategy aligns with broader objectives, balancing education and retirement.

- Liquidity and Flexibility: Determine how quickly you may need access to funds and the desired flexibility in their use.

- Financial Aid Impact: Understand how different accounts affect your child’s eligibility for need-based aid.

- State-Specific Tax Benefits: Investigate potential tax advantages for contributions to 529 Plans in your state.

Strategic Implementation Tips

- Combine Options: A strategy that merges 529 Plans and Coverdell ESAs can optimize tax benefits and cover a broader range of expenses.

- Enhance Flexibility: Incorporating UTMA/UGMA accounts or Roth IRAs into your savings plan can provide greater financial adaptability.

- Seek Professional Guidance: Consult a certified financial planner for personalized advice tailored to your specific situation.

Unlock Your Child’s Future: Mastering College Savings Plans for Lifelong Success!

In conclusion, understanding the various college savings options available is essential for planning your child’s educational future. From 529 Plans that offer tax-free growth to Coverdell ESAs that provide flexibility for K-12 expenses, each option has unique advantages and considerations. Remember, the funds in these accounts can significantly influence your child’s financial aid eligibility, so choose wisely.

“An investment in knowledge pays the best interest.”

– Benjamin Franklin

Now that you are equipped with knowledge about college savings accounts, take actionable steps to secure your family’s financial future:

- Research and select the right college savings account for your needs.

- Consult a financial advisor to tailor your strategy.

- Start saving early to maximize the benefits of compounding interest.

Ready to take control of your child’s educational journey? Explore our comprehensive guide on 529 Plans to maximize your savings potential today! Investing in your child’s education is not just a financial decision; it’s a commitment to their dreams and future success.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.