Are you feeling overwhelmed by the rising costs of college education? Worried about how to pay for tuition and expenses when you go to college? Don’t worry, you’re not alone! Many students and parents face the challenge of financing higher education.

But fear not! In this article, we’ll explore different ways of paying for college and provide valuable tips on managing college expenses. So, if you’re looking for a financial plan that works and want to know about 6 ways to pay for college, keep reading!

So, how are you going to pay for college? Are you considering paying out of pocket, using financial aid, or exploring other ways to pay for school?

Learning how to pay for college can feel like navigating a maze, with countless options and decisions to make. But fear not! Think of us as your trusted guide, here to help you understand the pros and cons of different ways to pay for college.

Paying for college requires careful consideration and planning. Scholarships, grants, work-study programs, student loans, and other cost-saving measures all have their pros and cons, and it’s essential to weigh them based on individual needs and circumstances.

Imagine a recent graduate, Jordan, who was excited to start her college journey but was unsure of how to pay for it. She decided to seek professional advice and worked with a financial advisor to explore her options.

Together, they compared the pros and cons of different ways to pay for college based on key factors such as eligibility requirements, application processes, repayment options, interest rates, and potential impact on future finances.

Let’s explore scholarships, grants, work-study programs, student loans, and other cost-saving measures, so you can make an informed decision that fits your financial needs and goals.

But wait, there’s more! We’ll also share tips on earning college credit, attending college classes, and utilizing the College Level Examination Program (CLEP) to save on tuition costs.

We know that figuring out how to pay for college can be overwhelming, but don’t worry, we’ve got practical advice to help you navigate this process.

Are you ready to take control of your college expenses? Let’s dive in and explore how you can create a financial plan that works, earn money to help pay for college, and make your dream of obtaining a college degree a reality.

As the famous quote goes:

THE FUTURE BELONGS TO THOSE WHO BELIEVE IN THE BEAUTY OF THEIR DREAMS.

by Eleanor Roosevelt

By understanding the options and making wise financial choices, students can make their dream of obtaining a college degree a reality.

Importance of Higher Education and Best Ways To Pay For College

Key Takeaways Ahead

Higher education plays a crucial role in an individual’s personal and professional development. It opens doors to better job prospects, higher salaries, and improved quality of life.

College education provides opportunities to learn and grow in a structured environment, interact with diverse peers, and gain valuable life skills such as critical thinking, problem-solving, and communication.

Obtaining a degree can also increase an individual’s confidence and self-esteem, leading to a sense of accomplishment and pride.

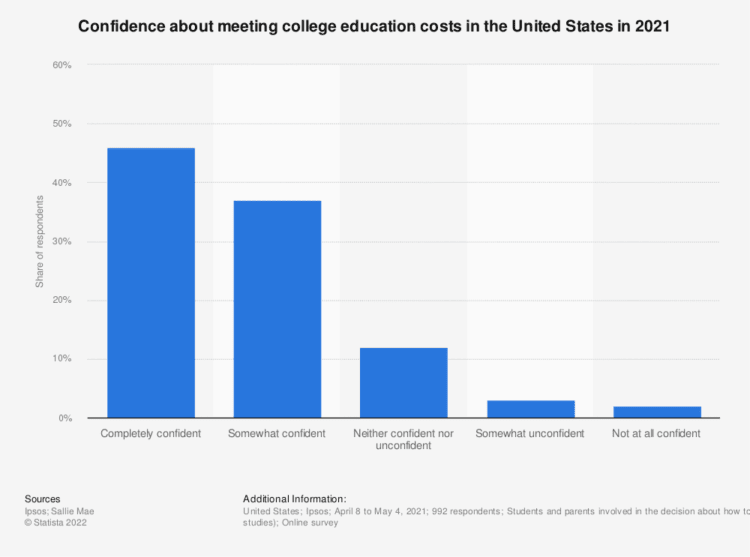

Rising Costs of College Education & Tuition

Over the years, the cost of college education has been on the rise, becoming a significant financial burden for many families.

According to the College Board, the average cost of tuition and fees for a public college, or four-year in-state college was $11,950 in the 2025-26 academic year, and for a private college was $59,750.

These costs do not include additional expenses such as textbooks, room and board, transportation, and other miscellaneous fees, which can significantly add to the overall cost of college education.

Challenges in Paying for College Expenses

Paying for college can be like climbing a mountain with ever-increasing heights. As you ascend, you face challenges like rising tuition and fees, student loan debt, limited scholarships and grants, and limited job opportunities.

Navigating these obstacles can be daunting, but with careful planning and informed decision-making, you can reach the summit of a college education.

The future belongs to those who prepare for it today.

– Malcolm X

While traditional methods of paying for college can be helpful, they may not always be sufficient to cover the rising costs of college education. Many students and families face challenges in financing higher education, including:

1. Rising Tuition and Fees

As mentioned earlier, the cost of college education has been steadily increasing, outpacing inflation and wage growth. Rising tuition and fees can pose a significant financial burden for families, making it challenging to afford college education without incurring debt or compromising on other essential expenses.

2. Student Loan Debt

Student loans are a common method of financing college education, but they can also lead to significant debt burdens for students and their families. Many students graduate with substantial student loan debt, which can take years or even decades to pay off, impacting their financial well-being and future financial decisions.

3. Limited Scholarships and Grants

While scholarships and grants can provide valuable financial assistance, they may not always be readily available or cover the full cost of college education. Scholarships and grants are often competitive, and not all students may qualify for them, leaving them with limited options for funding their education.

4. Limited Job Opportunities

Part-time jobs and work-study programs can be a good source of income for college students, but job opportunities may be limited or competitive, depending on the location and availability of jobs. Students may struggle to find suitable employment or may need to balance work with their academic and personal commitments.

I recently assisted Christine, a high school senior with college plans. Despite her dream of studying engineering, Christine was worried about rising tuition costs and potential student loan debt.

We discussed pros and cons of loans, explored scholarships and grants, and considered part-time work on campus. Christine was determined to minimize debt and diligently searched for more scholarships, secured a part-time job, and successfully graduated with minimal student loan debt and a strong financial foundation for her future.

- As per a report by the Institute for College Access and Success, the average student loan debt for the class of 2020 was $30,030, and about 62% of college seniors who graduated from public and private nonprofit colleges had student loan debt.

The best way to pay for college is to not go into debt in the first place. Plan ahead, save early, apply for scholarships and grants, and explore all financial aid award options.

Navigating the Costs & Expenses of College Education

Planning for college expenses is like embarking on a journey with a map in hand. Just as you need a well-defined path to reach your destination, understanding the expenses of college education and having a comprehensive plan in place is crucial for a successful journey to obtaining a degree.

Tuition costs and how they vary by institution

When planning for higher education, it’s crucial to comprehend the various costs associated with attending college. Tuition costs can vary significantly depending on the institution, with some colleges and universities charging higher tuition and fees compared to others. Room and board expenses, which include housing and dining costs, also play a significant role in the overall expenses of college.

Room and board expenses and their impact on overall costs

In addition to tuition and room and board, there are other expenses to consider. Textbooks, supplies, and transportation are additional costs that can add up quickly. College textbooks, in particular, can be quite expensive, and transportation costs, whether for commuting to campus or traveling home during breaks, can also impact the overall cost of college.

Additional costs such as textbooks, supplies, and transportation

| Expense Category | Estimated Cost | Significance |

|---|---|---|

| Tuition | $10,000 – $40,000 per year | Largest expense, varies by college and program |

| Room and Board | $8,000 – $15,000 per year | Covers housing and meal plans |

| Textbooks and Supplies | $1,000 – $2,000 per year | Necessary for coursework |

| Transportation | $500 – $2,000 per year | Varies based on location and commuting needs |

| Miscellaneous Expenses | $1,000 – $3,000 per year | Includes personal and other miscellaneous expenses |

Importance of budgeting for college expenses

Budgeting money for college expenses is vital to ensure that you can cover all the costs associated with your education. It’s important to plan ahead and create a budget that includes tuition, room and board, textbooks, supplies, transportation, and other miscellaneous expenses. Understanding the full scope of college expenses and planning accordingly can help you avoid financial difficulties during your college years.

Figuring out how to pay for college can be a challenge for many students and their families. Some options include scholarships, grants, and loans. Scholarships and grants are typically awarded based on academic or athletic achievements, while loans may need to be repaid with interest after graduation. Many students also work part-time jobs or find other ways to earn money to help pay for their college education.

| Type of College | Tuition | Room and Board | Other Expenses |

|---|---|---|---|

| Public | Lower cost compared to private | Lower cost compared to private | Varies based on location and program |

| Private | Higher cost compared to public | Higher cost compared to public | Varies based on location and program |

| In-state | Lower cost for residents | Lower cost for residents | Varies based on location and program |

| Out-of-state | Higher cost for non-residents | Higher cost for non-residents | Varies based on location and program |

| Traditional | On-campus housing options | Meal plans available | Campus-related expenses |

| Online | Lower tuition, no room and board | No room and board | Technology and internet-related expenses |

It’s also essential to consider the long-term financial benefits of obtaining a college degree. Although college costs can be significant, obtaining a college degree can increase your earning potential over your lifetime, making it a worthwhile investment in your future.

There are various ways to plan for paying for college. It’s crucial to research and explore all available options, such as college grants or other forms of financial aid that can help cover college expenses. Many colleges and universities also offer payment plans or installment options to make paying for college more manageable.

When it comes to college expenses, it’s essential to have a comprehensive plan in place to cover all costs associated with attending college. Understanding the different expenses, budgeting effectively, and exploring all available options for financial aid can help you successfully navigate the costs of obtaining a college education.

- According to the National Center for Education Statistics, the average undergraduate student spends around $1,226 on textbooks and supplies each year.

- The Federal Reserve reported that outstanding student loan debt in the U.S. reached $1.635 trillion in 2022.

Investing in education pays the best interest.

– Benjamin Franklin

Navigating Federal Student Aid: FAFSA, Financial Aid, Federal Loans, Private Loans

As a financial expert and a father of a college student myself, I know firsthand the challenges of navigating the complex world of higher education expenses. However, there is hope in the form of federal student aid programs that can make pursuing a college degree more accessible.

Overview of Federal Student Aid programs

Federal Student Aid offers various programs to help students cover college expenses, including grants, scholarships, and loans.

Having a solid financial plan that works for your family’s situation is crucial when it comes to accessing federal student aid. Utilizing the resources available at the financial aid office and understanding the types of aid, repayment options, and eligibility criteria can help you find the best financial plan for your college expenses.

It’s also important to save for college through college savings plans or accounts to cover qualified higher education expenses.

| Type of Aid | Description | Pros | Cons |

|---|---|---|---|

| Grants | Pell Grants and other federal grants awarded based on financial need | Free money that does not need to be repaid | Limited funding, eligibility based on students with financial need |

| Scholarships | Awards based on merit, talent, or other criteria | Free money that does not need to be repaid | Limited availability, competitive |

| Loans | Borrowed money that must be repaid with interest | Flexible repayment options, lower interest rates compared to private loans | Repayment required, may accrue interest |

Filling out the Free Application for Federal Student Aid (FAFSA)

The Free Application for Federal Student Aid (FAFSA) is the first crucial step in accessing federal student aid. This form collects information about your financial situation, including your income, assets, and family size, to determine your eligibility for federal aid. It’s important to fill out the FAFSA accurately and on time to increase your chances of receiving financial aid.

Types of federal student loans and their features

Federal student loans are one type of aid available through the Department of Education. There are different types of federal student loans, each with its own features and benefits. Repayment options for federal student loans are flexible, and interest rates are typically lower compared to private loans. Qualifying for federal student loans is based on financial need, and they do not require a credit check or co-signer.

| Type of Loan | Description | Interest Rates | Repayment Options |

|---|---|---|---|

| Direct Subsidized Loans | Based on financial need, interest paid by the government while in school | Fixed, currently 6.39% for undergraduates | Standard, Graduated, Extended, Income-Driven Repayment (IDR) |

| Direct Unsubsidized Loans | Not based on financial need, interest accrues while in school | Fixed, currently 7.94% for undergraduates | Standard, Graduated, Extended, IDR |

| Direct PLUS Loans | For graduate students or parents of dependent undergraduate students, credit check required | Fixed, currently 8.94% | Standard, Graduated, Extended, IDR |

| Direct Consolidation Loans | Allows consolidation of multiple federal loans into one loan | Fixed, based on weighted average of current loans | Standard, Graduated, Extended, IDR |

For accurate and up to date student loan interest rates visit StudentAid.Gov

Federal Grants & Scholarships

Federal grants and scholarships are another form of aid that can help students pay for college. Pell Grants and other federal grants are awarded based on financial need and do not need to be paid back. It’s important to apply for federal grants and scholarships as they provide free money that can significantly reduce the overall cost of college.

(Source: U.S. Department of Education)

Comparing Federal and Private Student Loans

When it comes to financing your education, federal student loans generally offer more favorable terms compared to private loans. Federal loans typically have lower interest rates, flexible repayment options, and do not require a credit check or co-signer.

In contrast, private loans often have higher interest rates, may require a credit check, and may require a co-signer. It’s important to carefully consider your options and borrow responsibly to avoid overwhelming student debt in the future.

- I suggest you read my recent article for a more in depth view about navigating federal and private students loans.

Federal student aid is like a compass that can guide you on your educational journey. Just as a compass helps you find your way in the wilderness, federal student aid can help you navigate the sometimes daunting terrain of college expenses, pointing you in the direction of financial assistance and making higher education more accessible.

Unlocking the Treasure Chest: How Scholarships and Grants Can Reduce College Costs

- Types of scholarships and grants available for college students

- How to search for scholarships and grants

- Tips for successful scholarship applications

- Understanding merit-based and need-based scholarships

The importance of scholarships, grants, and financial aid in funding higher education is undeniable.

Scholarships and grants are like a treasure chest hidden in plain sight, waiting to be discovered by diligent college-bound students. Just like a skilled treasure hunter, you can unlock the riches of scholarships and grants to reduce your college costs and make your higher education dreams come true.

Scholarships are awarded based on merit, such as academic achievements, leadership skills, or community involvement, and do not require repayment. Many organizations, including schools, non-profits, and private foundations, offer scholarships to eligible students.

Grants, on the other hand, are typically need-based and can be awarded based on financial need or specific criteria, such as major or field of study.

Scholarships and grants are an essential part of the college funding equation, helping students bridge the gap between their aspirations and financial limitations.

When it comes to scholarships and grants, there are various types available for college students, including merit-based scholarships, need-based scholarships, institutional scholarships, private scholarships, and grants from organizations and foundations.

Types of Scholarships and Grants That Are Available to You

Students can search for scholarships and grants using scholarship search engines, local scholarships, high school and community resources, and other avenues.

| Type of Scholarship/Grant | Description | Pros | |

|---|---|---|---|

| Merit-based Scholarships | Awarded based on academic achievements, leadership skills, or community involvement. | Do not require repayment. Recognize and reward students’ achievements. Can be highly competitive. May have specific eligibility criteria. | |

| Need-based Scholarships | Awarded based on financial need. | Do not require repayment. Provide assistance to students with financial limitations. May require submitting financial information. Availability may be limited. | |

| Institutional Scholarships | Offered by colleges and universities. | May be based on merit or need. Can be tailored to specific majors or fields of study. May require maintaining certain GPA or enrollment requirements. | |

| Private Scholarships | Offered by non-profits, private foundations, and organizations. | Wide range of eligibility criteria. Can be based on specific demographics, interests, or career goals. May require additional application materials. May have limited availability. | |

| Grants from Organizations and Foundations | Offered by non-profits, foundations, and organizations. | May be need-based or based on specific criteria. Can provide financial assistance for tuition, fees, and other expenses. May require additional documentation. Availability may vary. |

Tips for successful scholarship applications can also help students increase their chances of securing these forms of financial aid.

Scholarships and grants play a crucial role in reducing the overall costs of college education. They can provide cost-saving benefits and help students cover tuition, fees, books, and other expenses associated with college.

Maximizing scholarship and grant opportunities can be a part of an effective financial plan that works to make college education more affordable and accessible.

In addition to scholarships and grants, financial aid, including federal and state aid, is another important source of funding for college education. Students can complete the Free Application for Federal Student Aid (FAFSA) to determine their eligibility for federal and state aid programs, such as Pell Grants, Federal Work-Study, and student loans. Financial aid can provide significant support in covering the costs of college education, and utilizing it wisely can help students minimize the need to rely on loans that need to be paid back.

Understanding the different types of scholarships, grants, and financial aid options available, as well as the application process, can be key in securing funds for college.

According to the National Association of Student Financial Aid Administrators, private scholarships account for about 3% of total student aid awarded annually.

It’s important for students and families to explore all available opportunities and create a financial plan that works for their individual needs and circumstances.

Scholarships, grants, and financial aid can be valuable resources that help students achieve their higher education goals without facing excessive financial burdens.

- The College Board reports that the average annual tuition and fees for private four-year institutions were $36,880 in the 2020-2021 academic year. See Trends in College Pricing

How to Search for Scholarships and Grants: Practical tips for students on how to search for scholarships and grants, including:

- Utilize scholarship search engines: Websites such as Fastweb, Scholarships.com, and Cappex allow students to search for scholarships that match their interests, skills, and background.

- Check local scholarships: Many local organizations, such as community foundations, businesses, and civic groups, offer scholarships to students from their area. Check with

Private Student Loans: Navigating Your Options

While scholarships, grants, and financial aid are crucial sources of funding, they may not always cover all the expenses. That’s where private student loans can come into play.

In this section, I’ll share some insights on understanding private student loans and how they differ from federal student loans, as well as the pros and cons of taking out private student loans.

Think of private student loans as a double-edged sword – they can be a powerful tool to unlock the doors of higher education, but they come with their own set of risks and challenges. Just like a sword, private loans should be wielded with caution, and it’s essential to have a firm grip on your financial situation to avoid getting cut by unexpected costs or predatory lending practices.

Understanding private student loans and their differences from federal student loans

First, it’s important to understand the differences between federal and private student loans. Federal student loans are offered by the Department of Education and are based on financial need, while private student loans are typically offered by private lenders and may require a credit check or a cosigner.

Unlike federal loans, private loans are not backed by the government, which means they may have different terms, interest rates, and repayment options.

Pros and cons of private student loans

One of the benefits of private student loans is that they can help bridge the gap between the cost of attendance and other forms of financial aid. Private loans can be used for tuition, fees, books, and other college-related expenses.

However, it’s important to carefully consider the pros and cons before deciding to take out a private student loan.

| Aspect | Federal Student Loans | Private Student Loans |

|---|---|---|

| Offered By | Department of Education | Private lenders |

| Based on | Financial need | Creditworthiness, may require cosigner |

| Backed By | Government | Not backed by government |

| Interest Rates | Fixed rates set by Congress | Variable rates based on creditworthiness |

| Repayment Options | Flexible options, including income-driven plans | Varies by lender, may not be as flexible |

| Borrower Protections | Borrower-friendly options, such as loan forgiveness, deferment, and forbearance | Limited borrower protections, may not offer forgiveness or other options |

Pros of private student loans include flexibility in loan amount and repayment options, potentially lower interest rates for borrowers with good credit, and the ability to use the funds for various education-related expenses.

Private loans can be a viable option for students who don’t qualify for federal loans or need additional funds beyond what federal loans provide.

On the other hand, there are also cons to private student loans. Private loans may have higher interest rates compared to federal loans, and the interest may start accruing while the student is still in school.

Private loans also typically require a credit check, and borrowers with limited credit history or poor credit may need a cosigner, which can impact their credit score and financial responsibility.

| Pros | Cons |

|---|---|

| Flexibility in loan amount and repayment options | Higher interest rates compared to federal loans |

| Potentially lower interest rates for borrowers with good credit | Interest may start accruing while in school |

| Ability to use funds for various education-related expenses | Credit check and cosigner may be required for some borrowers |

| Can bridge the gap between cost of attendance and other forms of financial aid | Limited borrower protections compared to federal loans |

How to apply for private student loans

Applying for private student loans involves several steps.

- First, borrowers need to meet the eligibility requirements of the private lender, which may include credit score, income, and other criteria. It’s important to research and compare different lenders to find the best fit for your needs.

- Once a lender is chosen, the borrower will need to submit an application, including personal information, financial details, and the desired loan amount.

- After approval, the borrower will receive loan terms and disclosures that outline the interest rate, repayment options, and other important details.

Managing private student loan debt requires responsible borrowing and financial planning. It’s important to borrow only what is necessary and to keep track of the total loan amount, interest rates, and repayment terms.

Repayment options and strategies for private student loans

Creating a budget and setting aside funds for loan payments can help borrowers stay on top of their obligations. Exploring repayment options, such as making interest payments while in school or opting for a longer repayment term, can also make monthly payments more manageable.

Private student loans can provide much-needed financial assistance for college, but it’s important for borrowers to carefully consider the terms and weigh the risks against the benefits. It’s crucial to understand the differences between federal and private loans, and make informed decisions to avoid potential financial pitfalls.

Factors to consider when choosing private student loans

Private student loans can be a valuable tool for financing college education, but they should be approached with caution. Understanding the differences between federal and private loans, considering the pros and cons, and carefully managing the borrowing and repayment process are crucial steps in utilizing private student loans effectively.

As a financial expert and a father of a college student myself, I encourage you to thoroughly research and evaluate all your options to make informed decisions about paying for college. Remember, responsible borrowing and financial planning are key to minimizing student loan debt and achieving long-term financial success.

- The Consumer Financial Protection Bureau (CFPB) reports that over 90% of private student loans are cosigned, and having a cosigner can impact the borrower’s credit score and financial responsibility.

- According to a report by The Institute for College Access & Success (TICAS), private student loans often have higher interest rates than federal loans, with rates that can reach double digits, and the interest may start accruing while the student is still in school.

Building a Bright Future: Unlocking the Power of 529 College Savings Plans

As a father of a college student myself, I understand the financial challenges that come with paying for higher education. One option that has been immensely helpful for my family is a 529 college savings account. Let me share with you some insights on how you can use college savings plans to effectively save for your child’s education, and can help you pay for school.

As parents, we want the best for our children, including a bright and promising future. However, the rising cost of higher education can be a daunting challenge. Fortunately, there are powerful tools available to help families save for college, and one such tool is a 529 college savings plan.

529 College Savings Plans

Think of a college savings plan like a powerful toolbox that equips you with the right tools to build a bright future for your child. Just like a hammer, screwdriver, and wrench serve different purposes in construction, different college savings options have their unique features and benefits. But when it comes to saving for higher education, a 529 plan is like a Swiss Army knife – versatile, efficient, and designed to meet all your needs.

To read more about everything you want to know about 529 plans, I suggest you read my recent article:

How Much Should A Teenager Save Now?

Overview of 529 college savings plans

A 529 plan is a specialized savings plan designed to help families save for college expenses. There are two types of 529 plans: prepaid tuition plans and education savings plans. Prepaid tuition plans allow you to prepay a portion of your child’s tuition at today’s prices, while education savings plans allow you to invest in a variety of investment options to grow your savings over time.

FL 529 vs. Prepaid Tuition Plan – Which is Better?

Tax benefits and investment options of 529 plans

The biggest advantage of a 529 plan is the tax benefits it offers. Contributions to a 529 plan are typically tax-deductible at the state level, and the earnings grow tax-free. When it’s time to use the funds for qualified education expenses, such as tuition, books, and room and board, the withdrawals are also tax-free at the federal level. This makes a 529 plan a powerful tool for saving for college.

How to set up and contribute to a 529 plan

Setting up a 529 plan is relatively easy. You can open an account with a plan directly or through a financial advisor. Once the account is set up, you can make regular contributions to the plan, which can be as low as $25 per month. It’s important to choose an investment option that aligns with your risk tolerance and time horizon, as the performance of the investments will impact the growth of your savings.

One major update in 2023 is the SECURE 2.0 Act. Beginning in 2024 you can rollover money that is unused 529 Roth IRA (up to $35,000)

Understanding other college savings options

In addition to 529 plans, there are other college savings options to consider. Coverdell Education Savings Accounts (ESAs) and custodial accounts (UTMA/UGMA) are other tax-advantaged options that can be used to save for education expenses. Roth IRA, which is typically used for retirement savings, can also be used to save for college if needed.

| Option | Tax Benefits | Contribution Limits | Investment Options | Withdrawal Flexibility | Pros | Cons |

|---|---|---|---|---|---|---|

| 529 Plan | Tax-deductible contributions at state level; Tax-free growth and withdrawals for qualified education expenses | $17,000 per year Varies by plan; generally higher limits compared to other options | Wide range of investment options; flexibility to change investments | Can be used at any eligible educational institution; can also be transferred to another family member | Provides significant tax benefits; flexibility in investment options; can be used for tuition, books, room and board | Limited to education expenses only; penalties for non-qualified withdrawals |

| Coverdell ESA | Tax-free growth and withdrawals for qualified education expenses | $2,000 per year per beneficiary | Limited investment options; contributions must stop when beneficiary turns 18 | Can be used for elementary, secondary, and higher education expenses | Can be used for K-12 education expenses; flexibility to change investments | Contributions limited to $2,000 per year; must stop at age 18 |

| Custodial Account (UTMA/UGMA) | Taxable investment earnings at child’s tax rate; flexible use of funds | No contribution limits | Limited investment options; assets belong to the child | Child gains control of the account at age of majority (18 or 21, depending on the state) | No contribution limits; flexibility in use of funds | Assets belong to the child; child gains control at age of majority |

| Roth IRA | Tax-free growth and withdrawals for qualified education expenses; can also be used for retirement | Contribution limits based on income and age | Wide range of investment options | Can be used for retirement and education expenses; flexibility in investment options | Can be used for retirement and education expenses; tax-free growth and withdrawals for qualified education expenses | Contributions limited by income and age; penalties for non-qualified withdrawals |

Using 529 plans to save for college expenses

College savings plans play a crucial role in reducing the reliance on student loans, which can result in significant debt burden for students after graduation. By starting early and consistently contributing to a college savings plan, you can provide your child with a solid financial foundation for their higher education journey.

It’s important to develop a strategy that aligns with your family’s financial goals and seek advice from a qualified financial professional if needed.

Remember, planning and saving for college is a long-term process, and every dollar you save today can make a meaningful difference in your child’s future. Don’t wait until the last minute to figure out how you’re going to pay for college. Start exploring your college savings options now and take control of your financial future.

Work-Study Programs and Part-Time Jobs

Imagine navigating a maze where every turn presents a new challenge, and the stakes are high. That’s what paying for college can feel like for many students and their families. As a college consultant, I’ve seen firsthand the financial struggles that can accompany pursuing higher education. However, with careful planning and creative solutions, it’s possible to unlock a path to financial success.

In this section, I’ll share insights on work-study programs, part-time jobs, and other creative ways to pay for college, including tables to provide a clear comparison of these options.

Let me share with you some insights on how you can pay for college through work-study programs, part-time jobs, and other creative ways.

Overview of work-study programs offered by colleges and universities

Work-study programs offered by colleges and universities can be a great option for students to earn money while gaining valuable work experience. These programs typically provide on-campus jobs that are tailored to the student’s academic schedule, allowing them to balance work and academics effectively.

Many work-study programs also offer competitive wages and flexible hours, making them an attractive option for students looking to earn money you need to pay for college expenses.

Finding part-time jobs on and off-campus

Finding part-time jobs on and off-campus can also be a viable option for students. Many colleges and universities have job boards or career services offices that can help students find part-time employment opportunities. Off-campus jobs, such as internships or jobs in the local community, can also provide valuable experience and income.

| Concept | Pros | Cons |

|---|---|---|

| Work-Study Programs | – Earn money while gaining work experience – On-campus jobs tailored to academic schedule – Competitive wages and flexible hours | – Limited availability – May require applying and competing for positions – May not cover all expenses |

Balancing work and academics during college

It’s important to balance work and academics during college to ensure academic success. Managing time effectively and prioritizing academic responsibilities while working can be challenging, but with proper planning and organization, it’s possible to strike a healthy balance between work and school commitments.

Utilizing work-study and part-time jobs to pay for college

In addition to work-study programs and part-time jobs, there are other creative ways to pay for college. Some employers offer tuition assistance or reimbursement programs as part of their employee benefits package. These programs can provide financial support for employees pursuing higher education and may have specific eligibility requirements.

How Teens Can Earn Money

Community college and transfer programs can also be a cost-effective way to start your college journey. Community colleges often offer lower tuition rates compared to four-year colleges and universities, and students can save money by completing general education requirements at a community college before transferring to a four-year institution. Transfer programs can also provide a seamless pathway to continue education at a four-year college or university.

How Much Should A Teenager Save Now?

Other ways to pay for college may include earning college credit for life experiences, leveraging military benefits for higher education if applicable, or exploring crowdfunding options to gather support from the community.

Benefits and limitations of work-study programs

Remember, paying for college requires careful planning and consideration of all available options. Work-study programs, part-time jobs, employer tuition assistance, community college and transfer programs, and other creative solutions can help you fund your education and achieve your academic goals.

Don’t be afraid to explore different avenues and seek guidance from college resources or financial advisors to make informed decisions about how to best pay for college. Your hard work and determination can pave the way for a successful college experience without incurring excessive debt.

- According to the Federal Student Aid website, in the 2019-2020 academic year, approximately 640,000 undergraduate students participated in the Federal Work-Study program, earning an average of $1,770 each.

- A study by the National Association of Student Financial Aid Administrators found that students who participated in work-study programs were more likely to graduate compared to those who did not participate.

Client Story:

However, Lauren initially struggled with time management and found herself overwhelmed with balancing her job, academics, and other commitments.

As her consultant, I helped her develop a schedule and prioritize her responsibilities, ensuring that she could excel in her studies while still earning money through the work-study program. Lauren learned from her mistakes and eventually found a healthy balance between work and academics, leading to academic success and financial stability.

| Concept | Pros | Cons |

|---|---|---|

| Part-Time Jobs | – Opportunities on and off-campus – Can provide valuable work experience – Additional income source | – May require additional time commitment – May not align with academic schedule – May not cover all expenses |

- According to a report by Georgetown University’s Center on Education and the Workforce, 70% of college students work while enrolled in school.

- A study by the National Association of Colleges and Employers found that students who work part-time during college are more likely to develop skills such as time management, organization, and problem-solving.

Other Ways to Pay for College + Room and Board

It’s important to note that these creative ways to pay for college may not be suitable or available for everyone, and it’s essential to carefully consider the pros and cons before pursuing them. It’s also recommended to consult with college resources, financial advisors, or other trusted sources to ensure informed decision-making.

Exploring alternative options for paying for college

It can be overwhelming to figure out the best ways to cover the costs, but don’t worry, there are alternative options to explore! Let me share some creative methods that can help you find financial solutions for college education.

| Creative Way to Pay for College | Concept | Pros | Cons |

|---|---|---|---|

| Earning College Credit for Life Experiences | Some colleges and universities offer programs that allow students to earn college credit for life experiences, such as work or volunteer activities, military service, or other relevant experiences. | – Can save time and money by earning college credit without taking traditional courses. | – Availability and applicability of credit may vary by institution. – May require extensive documentation and evaluation of experiences. – Credit earned may not always transfer to other institutions. |

| Leveraging Military Benefits for Higher Education | Members of the military, veterans, and their dependents may be eligible for various education benefits, such as the GI Bill, tuition assistance programs, or scholarships specifically for military personnel. | – Can provide financial support for education without incurring debt. – May offer additional benefits, such as housing allowances, health insurance, or career opportunities. | – Eligibility and benefits may vary depending on military branch, service duration, and other factors. – May require meeting specific service requirements or maintaining certain academic standards. – Benefits may have limitations or expiration dates. |

| Crowdfunding for College Expenses | Crowdfunding platforms, such as GoFundMe or Kickstarter, can be used to gather support from friends, family, and the community to fund college expenses. | – Can provide additional financial support beyond traditional sources. – Can raise awareness and engagement from a wider audience. – Can foster a sense of community and support. | – Success may depend on personal network and marketing efforts. – May require ongoing promotion and outreach. – Contributions may be subject to fees or taxes. |

Crowdfunding, grants from community organizations, and other creative methods

One of the best ways to explore alternative methods of paying for college is through crowdfunding and fundraising. Students can create crowdfunding campaigns or seek donations from family, friends, and the community to help cover their educational expenses.

Social media platforms and online fundraising websites have made it easier for students to connect with potential donors and raise funds for their education. It’s a creative way to leverage the power of community support!

Another option to consider is employer tuition assistance programs. Many employers offer tuition assistance programs as part of their employee benefits package.

These programs provide financial assistance to employees who want to pursue higher education, and the employer may cover part or all of the tuition costs. It’s worth checking if your employer offers such programs and take advantage of this benefit to help you pay for college.

Considering part-time or online education to reduce costs

Alternative education programs, such as vocational or trade schools, community colleges, or online programs, can also be more affordable compared to traditional four-year colleges and universities.

These programs may provide specialized training and education that can lead to rewarding career opportunities without incurring substantial student loan debt. It’s worth exploring these options and considering if they align with your career goals and financial plan.

Additionally, serving in the military or joining programs like Americorps can provide education benefits in exchange for service.

The military and Americorps offer various education assistance programs, such as the GI Bill, tuition reimbursement, or education grants, which can help fund college education. It’s a unique way to serve your country and earn college credit at the same time.

Combining multiple methods to pay for college

Remember, combining multiple methods you’ll have to pay for college can also be a strategic approach. You can explore a mix of crowdfunding, employer tuition assistance, alternative education programs, and military service to create a financial plan that works for you.

It may require careful planning and consideration, but with creativity and determination, you can find alternative ways to help cover college expenses and achieve your educational goals.

Understanding the risks and benefits of alternative ways to pay for college

So, don’t be discouraged if you’re unsure about how to pay for college. There are alternative options out there! By considering crowdfunding, employer tuition assistance, alternative education programs, and military service, you can explore creative and effective ways to make your college dreams a reality.

Remember to do your research, weigh the risks and benefits, and create a financial plan that aligns with your unique situation. You’ve got this!

Can a 529 Plan Be Used to Pay for College and Higher Education Expenses?

529 plan questions answered: Yes, a 529 plan can be used to pay for college and higher education expenses. These plans are tax-advantaged savings accounts specifically designed for educational expenses. They cover various costs like tuition, books, room and board, and even certain technology expenses. It’s a great way to save and invest for future education while enjoying potential tax benefits.

The College Financial Maze: Practical Tips for Planning and Budgeting for Higher Education Expenses

As a parent, I know firsthand the challenges of planning and budgeting for college expenses. It’s not just about the tuition fees, but also the cost of textbooks, housing, meals, and other education expenses that can add up quickly. That’s why it’s crucial to have a financial plan in place that works for you and your family.

Creating a budget for college expenses

Creating a budget for college expenses is an essential step in managing costs effectively. Start by listing out all the potential expenses, from tuition fees to textbooks to living expenses. Then, prioritize and allocate your available funds accordingly. It’s important to be realistic about what you can afford and avoid taking on unnecessary debt.

Understanding the long-term financial impact of paying for college

Understanding the long-term financial impact of paying for college is crucial. Loans may seem like a quick solution, but they come with interest rates and repayment options that need to be considered carefully. Look into all available options, such as scholarships, grants, and work-study programs, before resorting to loans. Keep in mind that loans need to be repaid, and it’s important to have a plan in place for repayment.

Importance of financial planning for college

Planning and budgeting for college expenses is like embarking on a complex maze with multiple paths and dead-ends. Without a well-thought-out strategy and careful navigation, families can easily get lost in the maze of tuition fees, textbooks, housing costs, and other education expenses, leading to financial stress and unnecessary debt.

Seeking professional advice for financial planning for college

Don’t be afraid to seek professional advice for financial planning for college. Financial advisors, counselors, and other experts can provide valuable insights and help you figure out how to pay for college without sacrificing your long-term financial goals. They can help you understand the repayment options, interest rates, and other details related to financing your education.

Tips for managing college costs effectively

In addition to financial aid funds, there are other ways to offset college expenses. Consider earning college credit while still in high school through programs such as the College Level Examination Program (CLEP) or taking college classes at a local community college and then transferring the credits to a four-year institution. These options can help you save on tuition costs and graduate earlier, reducing the overall expenses.

Planning and budgeting for college expenses require careful consideration and realistic expectations. By creating a detailed budget, prioritizing expenses, exploring alternative methods of paying for college, and seeking professional advice, families can effectively manage the financial aspects of sending their children to college without sacrificing their long-term financial goals. A

As the saying goes, “Failing to plan is planning to fail.” By taking proactive steps to navigate the college financial maze, families can set themselves up for success and ensure a brighter future for their children.

The best investment you can make is in yourself.

Warren Buffett

Frequently Asked Questions (FAQs)

What are some common ways to pay for college?

Common ways to pay for college include financial aid, scholarships, grants, savings, part-time jobs, and student loans.

How do I create a budget for college expenses?

Creating a budget for college expenses involves estimating tuition, housing, textbooks, and other costs, and setting spending limits accordingly.

What are some repayment options for student loans?

Repayment options for student loans include standard repayment, income-driven repayment, deferment, and forbearance.

What are the interest rates on student loans?

Interest rates on student loans vary depending on the type of loan and market conditions, and can be fixed or variable.

How can I earn college credit while in high school or community college?

Earning college credit in high school or community college can be done through dual enrollment programs, Advanced Placement (AP) courses, or College Level Examination Program (CLEP) exams.

Where can I find additional information and assistance?

Additional information and assistance can be found on college websites, financial aid websites, or by contacting college financial aid offices or student loan servicers.

Are there additional resources for financial aid and scholarships?

Yes, there are many additional resources available, such as the Free Application for Federal Student Aid (FAFSA), scholarship search engines, and college financial aid offices.

How can I make informed decisions about paying for college?

To make informed decisions about paying for college, research different options, compare costs, and seek advice from financial aid counselors or other professionals.

Any quick tips for managing college costs effectively?

Some quick tips for managing college costs effectively include creating a budget, applying for financial aid early, exploring scholarship opportunities, and minimizing unnecessary expenses.

Recap of Various Ways of Paying For College

Let’s summarize the different methods available to cover the cost of a college education. It’s essential to carefully plan how to pay for college by conducting thorough research and making informed decisions. This may involve creating a budget, understanding loan options and interest rates, exploring scholarships and grants, and even earning college credit in high school or community college.

Given that college is expensive, it’s crucial to have a plan in place to cover the costs associated with higher education.

By planning how to pay for college, you can navigate the various avenues available to finance your education and make the most informed choices.

Importance of researching and planning for college expenses

In summary, having a financial plan in place and managing college expenses wisely can help you avoid unnecessary debt and set yourself up for long-term success. The key points to remember are to be realistic about your financial situation, seek professional advice if needed, and explore different options to make the most of your education.

To make sure you have the money to pay for college, it’s important you have a plan to pay the cost of college. This includes exploring options like scholarships or even paying for college courses at community college campuses.

Encouragement to explore different options and make informed decisions

In conclusion, paying for college may seem daunting, but with careful planning, budgeting, and exploring various resources, you can create a financial plan that works for you and your family. Remember, it’s never too early to start researching and preparing for college expenses, and making informed decisions can help you navigate the financial aspects of higher education with confidence. Best of luck in your college journey!