You’re sipping your morning coffee when it hits you. Recent changes to retirement laws could dramatically shape how you manage your finances.

SECURE Act 2.0 introduced a series of retirement rule changes that took effect in different years, with several important contribution-related updates applying in 2026.

Here’s what matters most about these key provisions and how you can use them to build a more secure retirement.

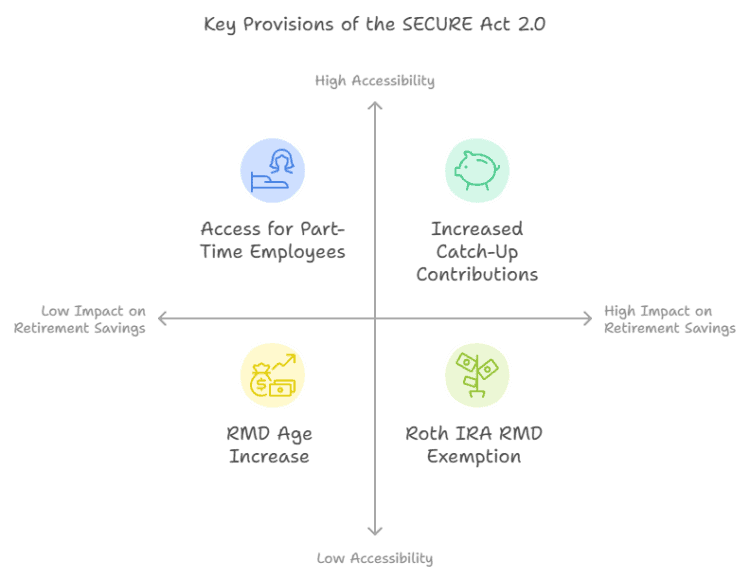

Key Provisions of the SECURE Act 2.0

The SECURE Act 2.0 brings changes that give you more control over your retirement funds, allowing for greater flexibility in growing your savings and managing your tax obligations.

- Catch-Up Contributions: In 2026, workers ages 60 through 63 in most 401(k), 403(b), governmental 457, and Thrift Savings Plan accounts can make up to $11,250 in catch-up contributions.

- RMD Age Increase: The RMD age is 73 for many current retirees, and it rises to 75 for individuals born in 1960 or later.

- Part-Time Employees: Starting in 2025 for plan years, long-term part-time employees generally need only two consecutive years with at least 500 hours of service to become eligible to make elective deferrals in covered 401(k) plans.

SECURE 2.0 did not create one single 2026 retirement rule change; instead, it rolled out a series of changes over several years.

Including higher catch-up contribution limits for certain workers in 2026, earlier access for long-term part-time employees, and prior changes to RMD and Roth employer-plan rules.

Why the SECURE Act Is Changing Your Retirement: What You Need to Know in 2026

In 2026, the SECURE Act will allow older workers (60-63) to supercharge their savings with a $11,250 catch-up contribution ($7,000 if under 50), while part-time employees gain access to retirement plans after two years of qualifying work.

Original owners of Roth IRAs already had no lifetime RMDs under prior law; SECURE 2.0 newly eliminated pre-death RMDs for designated Roth accounts in employer plans such as Roth 401(k)s and Roth 403(b)s beginning in 2024.

What Exactly Is the SECURE Act and How Does It Affect Your Retirement?

SECURE Act 2.0 includes several important retirement planning changes, with some already in effect and others continuing to matter in 2026. You’ll have more opportunities to boost your retirement savings through increased catch-up contributions.

Many newly established 401(k) and 403(b) plans must include automatic enrollment, generally with default deferral rates between 3-10% enrollment, unless an exception applies.

Plus, these plan amendments help if you’re working part-time, you’ll finally have access to the retirement benefits you deserve.

Increased Catch-Up Contributions: A Game-Changer for Older Workers

In 2026, workers ages 60 through 63 in most employer plans covered by the enhanced catch-up rule can contribute up to $11,250 in catch-up contributions.

For workers age 50 and older in most of those same plans, the regular catch-up limit is $8,000 in 2026.

That makes the years just before retirement especially valuable for boosting workplace retirement savings.

Retirement Savings Calculator

Calculate the monthly savings required to meet your 2026 retirement goals.

Key Changes Breakdown

| Change type | Old rule | New rule (SECURE 2.0) |

|---|---|---|

| RMD penalties on missed withdrawals | IRS excise tax was 50% of the missed required minimum distribution. | Excise tax reduced to 25%, and 10% if corrected in the IRS-approved window. |

| Roth 401(k) and Roth 403(b) RMDs | Employer-plan Roth accounts were subject to required minimum distributions. | No RMDs from Roth employer plans starting in 2024, aligning with Roth IRAs. |

| 529 plan rollovers to Roth IRA | 529 college savings funds generally could not be rolled into a Roth IRA. | Certain long-held 529 plans can roll up to $35,000 lifetime into a Roth IRA, subject to limits. |

| Employer match tax treatment | Matching contributions had to go into pre-tax accounts only. | Employees can elect to receive employer matches as Roth contributions where plans allow. |

RMD Flexibility: More Time for Growth

Under SECURE 2.0, the RMD starting age is now 73 for many retirees, and it increases to 75 for people born in 1960 or later.

For seniors, the extension of the RMD age means you’ll have more time for your investments to grow tax-deferred. RMDs, which are the minimum amounts you must withdraw from tax-deferred retirement accounts like 401(k)s and IRAs.

For seniors worried about the impact of taxes, the reduction in penalties for missed RMDs—from 50% to 25%. With the possibility of reducing it further to 10% if the mistake is corrected promptly. This reduction offers peace of mind, allowing retirees to fix mistakes without facing huge penalties.

These changes address core seniors’ concerns about preserving wealth and managing taxes effectively. Good-faith interpretations will be accepted while the IRS finalizes these regulations.

Inherited IRA rules and certain RMD questions remain complex, so it is wise to verify current IRS guidance before making distribution decisions.

Here’s what you need to know: Understanding the RMD aggregation rules, taking advantage of Qualified Charitable Distributions, and selecting the correct RMD Tables is crucial for accurate calculations.

Roth IRA Benefits: Tax-Free Growth with No RMDs

One longstanding benefit of Roth IRAs is that original owners do not have to take lifetime RMDs. SECURE 2.0 extended similar treatment to Roth employer-plan accounts beginning in 2024.

This means more flexibility for tax-free growth in your retirement savings, giving you greater control over your income strategy.

Retirement Readiness Quiz

Analyze your preparedness in 60 seconds. Our algorithm checks your strategy against current 2026 inflation and savings benchmarks.

Part-Time Workers Gain Access to Retirement Plans

Part-time employees will have access to retirement plans after two years of working at least 500 hours annually. This change opens up retirement options for millions of part-time workers who may have missed out on retirement benefits in the past.

| Benefit | What you get | How it helps |

|---|---|---|

| Catch-up boost (ages 60–63) | Up to about $11,250 extra catch-up room starting in 2025. | Lets late‑career workers accelerate 401(k)/403(b) savings in the final years before retirement. |

| Automatic enrollment in new plans | Default deferral between 3% and 10% of pay in many new 401(k)/403(b) plans. | Starts your retirement contributions automatically so you build savings without having to opt in. |

| Part‑time worker access | Long‑term part‑time employees become eligible to defer after as little as 500 hours in two years. | Extends retirement plan access to more part‑time workers who previously could not participate. |

| Lost plan search tool | New DOL Retirement Savings Lost & Found online database for old plans. | Helps you track down forgotten 401(k) or pension benefits after job changes or mergers. |

These changes aren’t just updates – they’re your pathway to a more secure retirement future.

What the SECURE Act Changes Mean for Retirement Accounts & RMDs

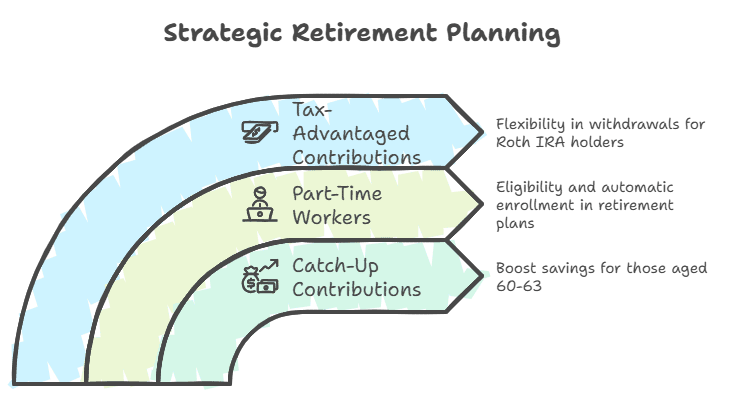

To make the most of these changes, consider adjusting your strategy. Here’s how:

- Maximize Catch-Up Contributions: If you’re aged 60-63, now’s the time to increase contributions to your 401(k) or IRA. This is your opportunity to boost savings in the final years before retirement.

- Part-Time Workers: Check if you’re eligible to participate in retirement plans and take advantage of the automatic enrollment features that ensure you’re saving for the future.

- Tax-Advantaged Contributions: Roth IRA holders will benefit from the elimination of RMDs, providing flexibility in your retirement withdrawals.

Real-Life Examples: How These Changes Help

Late-Career Worker: Sarah’s Strategy

Sarah, a 62-year-old marketing manager, worries about having enough for retirement. By taking advantage of the $11,250 catch-up contribution, she increases her 401(k) contributions and significantly boosts her savings. As a result, Sarah feels more confident and financially prepared for retirement.

Part-Time Worker: John Gets Access to Retirement

John, a part-time teacher and online business owner, has never had access to retirement plans. Thanks to the SECURE Act, he now qualifies for his employer’s retirement plan after two years of working 500+ hours annually. This new opportunity allows him to start saving for retirement without extra effort.

Strategic Withdrawal Considerations

- Balance traditional and Roth contributions

- Manage inherited IRA distributions within 10-year window

- Avoid higher tax bracket triggers

- Consider Roth catch-up contributions for high earners

Tax Optimization Strategies

| Approach | Benefit |

|---|---|

| Spread distributions | Stay in lower tax brackets |

| Time withdrawals | Minimize tax impact |

| Early withdrawal planning | Manage future income expectations |

The SECURE Act provides flexible tools to maximize retirement savings while minimizing tax liabilities, empower

1. Maximizing Contributions

- Step-by-Step Guide: Set up automatic transfers from your checking account to your retirement account to ensure you consistently contribute. Start small and gradually increase your contributions as your financial situation improves.

- Example: Consider setting a reminder every month to review your budget and increase your contributions by a small percentage.

2. Navigating RMDs

- Planning for RMDs: Strategically plan your RMDs by timing withdrawals to minimize tax impact. For instance, if you expect a lower income in a particular year, that might be the best time to take larger distributions.

3. Using Financial Tools

- Retirement Calculators: Use online retirement calculators to visualize how much you need to save each month to reach your retirement goals. Tools like our retirement calculator can provide personalized estimates based on your current savings and desired retirement age.

- Budgeting Apps: Consider using budgeting apps like Mint or YNAB (You Need A Budget) to track your spending and identify areas where you can increase your retirement contributions.

Key RMD Dates to Remember

| Action Item | Deadline Reminders |

|---|---|

| First RMD | April 1 following year you turn 73 |

| Annual RMDs | December 31 each year |

| Account Review | Quarterly check-ups recommended |

| Tax Planning | Year-round monitoring needed |

Penalty Reduction Strategy

- Correct missed RMD promptly

- Respond within the IRS correction window

- Take missed distribution immediately

- Document reasonable cause for potential waiver

Strategic Implications & Recommended Actions

- Consult with financial advisor

- Review RMD deadlines

- Strategize withdrawal timing

- Maximize tax-deferral benefits

Conclusion: Take Control of Your Retirement: SECURE Act Strategies

Strategic Action Plan: Contribution Optimization

- Maximize catch-up contributions

- Review employer plan details

- Balance traditional and Roth contributions

- Consider Roth conversions before RMDs

Tax Management

- Strategically time withdrawals

- Avoid higher tax bracket triggers

- Explore Qualified Charitable Distributions

- Monitor inherited IRA 10-year distribution rules

Practical Considerations

| Focus Area | Key Strategy |

|---|---|

| Budget | Increase retirement contributions |

| Tax Planning | Minimize tax liability |

| Withdrawal Timing | Optimize RMD strategies |

| Account Management | Consolidate and review regularly |

Critical Deadlines

- First RMD: April 1 following age 73

- Annual RMDs: December 31

- Catch-up contribution review: Annually

- Employer plan assessment: Before year-end

Recommended Next Steps

- Consult financial advisor

- Review retirement account strategy

- Assess catch-up contribution potential

- Update tax planning approach

Transform retirement planning by proactively leveraging the SECURE Act’s new opportunities.