After 25 years as a financial planner, I can tell you that the most financially fragile people I’ve met weren’t the ones with the lowest incomes. They were the ones with the best excuses. Those who never learned how to stop spending money

I’m talking about Pat and John from South Florida. From the outside, they were the picture of success: beautiful home in an affluent neighborhood, new cars, vacations that looked amazing on social media. But when I put their finances under the microscope, I saw a different story.

They were drowning in six figures of debt with almost nothing saved. They looked rich, but they were broke.

And they’re not alone. A stunning report from Clever Real Estate found that 74% of Americans admit they have an overspending problem. This isn’t a math problem. It’s a mindset problem.

Forget the generic tips you’ve heard a hundred times. We’re going to diagnose the real reason you can’t control your spending and give you the system that actually fixes it.

Key Takeaways Ahead

The Great Financial Illusion: Why Rich-Looking People Are Often Broke

The biggest predictor of overspending has nothing to do with your income and everything to do with the story you tell yourself and the world.

A big paycheck won’t save you from debt. After reviewing thousands of bank statements, I’ve seen six-figure earners crushed by lifestyle inflation. True wealth is measured by what you keep, not just what you earn.

I had other clients, Juan and Laura, who lived in the same neighborhood as baseball legend Cal Ripken. They had the address, but they lacked his famous discipline.

Even celebrities aren’t immune. Nicolas Cage earned $40 million in one year but ended up facing foreclosure after buying 15 homes. Income doesn’t inoculate you from a broken financial mindset.

The Overspender’s Playbook: 3 Common Excuses That Keep You Trapped

Overspenders are masters of self-deception, typically relying on three core excuses I’ve heard thousands of times.

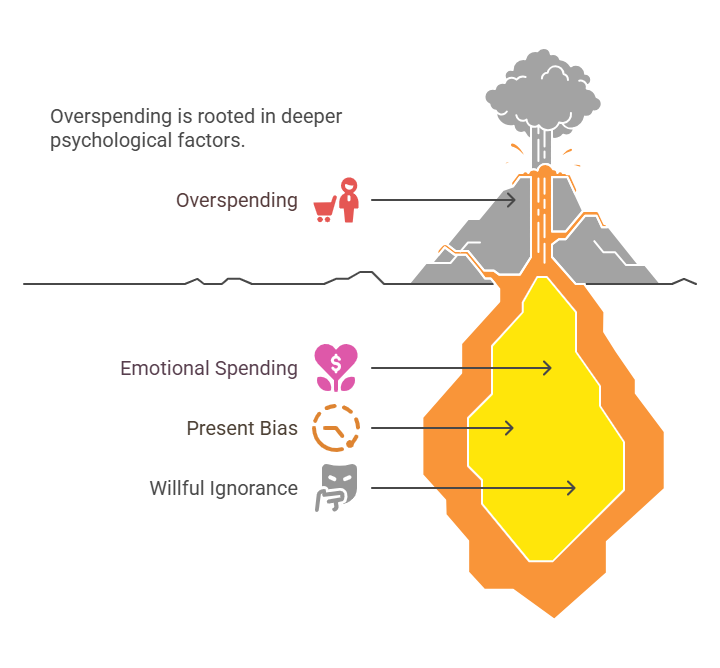

Excuse #1: “I Deserve It” – The Emotional Spending Trigger

This is never about the item; it’s about the feeling. Shopping triggers a release of dopamine in your brain, a neurochemical reward that makes you feel good in the moment. It’s why “retail therapy” is a real phenomenon.

Research from the American Psychological Association highlights how these behaviors provide temporary relief from stress or sadness.

Excuse #2: “I’ll Deal With It Later” – The High Cost of Present Bias

This is the most destructive excuse. It’s prioritizing the instant gratification of today over the well-being of your future self.

It guarantees a future of constant worry.

Excuse #3: “I Don’t Know Where It Goes” – The Willful Ignorance Trap

This isn’t a lack of information; it’s a fear of the truth. People avoid looking at their bank statements for the same reason they avoid stepping on a scale. They’re afraid of what they’ll see.

🧠 Michael’s Take: The Stories We Tell Ourselves

After 25 years, I realized my job wasn’t just managing money; it was decoding stories. The phrase “I deserve it” is rarely about the thing being bought. It’s usually code for “I’m stressed,” “I’m sad,” or “I feel inadequate.” Until you address the underlying emotion, you’ll never solve the spending problem. The purchase is just a symptom of a deeper narrative.

The ‘Frank’ Method: How the Truly Wealthy Really Think About Spending

The secret to controlling your spending is to stop budgeting and start curating, a mindset where every dollar is a tool used to build a life aligned with your deepest values.

The wealthiest client I ever had was a man named Frank. He was as down-to-earth as they come, and he will never have to worry about money. Why? Because Frank wasn’t a “spender” or a “saver”. He was a strategic allocator.

Break free from “one-size-fits-all” budgets. With value-based spending, you decide exactly where every dollar goes. Splurge without guilt on the 2–3 passions that light you up, and cut out every expense that doesn’t fuel your purpose.

Frank would spend lavishly on his family and hobbies and ruthlessly cut costs on everything else. He wasn’t afraid to look at his finances because his spending reflected his values. As Warren Buffett said:

“Do not save what is left after spending.

but spend what is left after saving.”

Your 3-Step Action Plan to Finally Control Your Spending

To stop overspending, you need to implement a system that makes intentionality the default. For a structured approach, consider a tool like the 50/30/20 rule calculator below to see where your money should be going.

Interactive 50/30/20 Budget Rule Calculator

The 50/30/20 rule is a guideline. Your ideal budget may vary based on income, location, goals, and debt levels. Focus on progress, not perfection!

See an issue or have a suggestion? We'd love to hear from you!

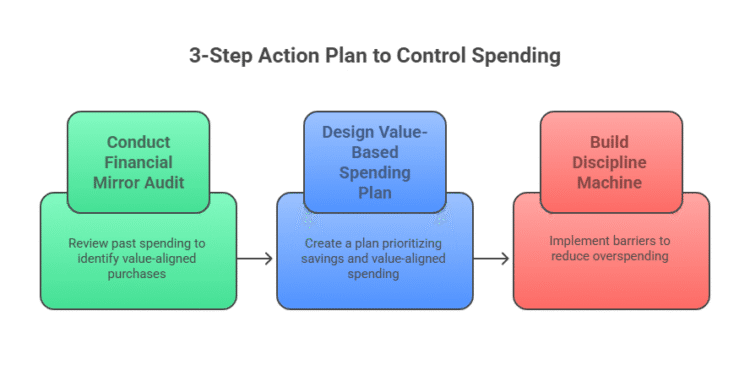

- Step 1: Conduct the “Financial Mirror” Audit

Print your last two credit card statements. With a green highlighter, mark every purchase that brought you genuine, lasting value. With a red highlighter, mark everything else. This “mirror” will show you the gap between your values and your habits. - Step 2: Design Your Value-Based Spending Plan

Based on your audit, create a simple spending plan. Use three categories:- Future You: Automate savings and investments first.

- Value Spending: The green-highlighted items. Spend guilt-free here.

- Everything Else: The red-highlighted items. Shrink this category with precision.

- Step 3: Build Your “Discipline Machine”

Create barriers to make overspending harder.- Automate Your Financial Future: Set up automatic transfers to savings. This is one of the core benefits of budgeting and planning.

- Implement a Waiting Period: Enforce a 24-48 hour waiting period for non-essential purchases.

- Use the Right Tool: Use cash or a separate debit card for your “Everything Else” category to create spending friction.

Beyond Excuses: The Real Payoff of Financial Discipline

The choice is yours: Will you continue making excuses, or will you develop the financial discipline that creates true freedom? Frank didn’t out-earn his peers; he just out-behaved them. He understood that controlling your spending isn’t about deprivation. It’s about designing a life where your money is a loyal employee working tirelessly for the things you care about most.

That is the foundation for lasting peace of mind.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.