Did you know that inheriting property could potentially cost you thousands in taxes? While receiving valuable assets is exciting, the looming specter of capital gains tax can turn your windfall into a financial headache.

But fear not – with the right strategies, you too can learn how to avoid paying capital gains tax on an inherited property.

As a financial planner for over two decades – I helped many clients significantly reduce or even eliminate this tax burden.

| Emotional Consideration | Description |

|---|---|

| Sentimental Value | Heirs must carefully evaluate their emotional attachment to financial needs and objectives |

| Complex Decision-Making | Heirs must carefully evaluate their emotional attachment against financial needs and objectives |

| Open Communication | Effective communication among family members can help in making informed decisions |

Why Should You Care About Capital Gains Tax on Inherited Property?

Imagine opening a letter from the Internal Revenue Service (IRS) demanding a hefty sum after selling your inherited home. Sounds stressful, right? This scenario is all too common, but it doesn’t have to be your reality.

🚨 CRITICAL 2026 UPDATE: The estate tax exemption is NO LONGER sunsetting! Under the One Big Beautiful Bill Act passed in 2025, the estate and gift tax exemption INCREASES to $15 million per person ($30 million for couples) starting January 1, 2026 – with NO sunset provision. This is a PERMANENT change, indexed for inflation going forward. Many financial advisors and websites still have outdated information about the supposed “sunset” to $7 million. That’s no longer happening. This means you have MORE time for strategic planning, not less.

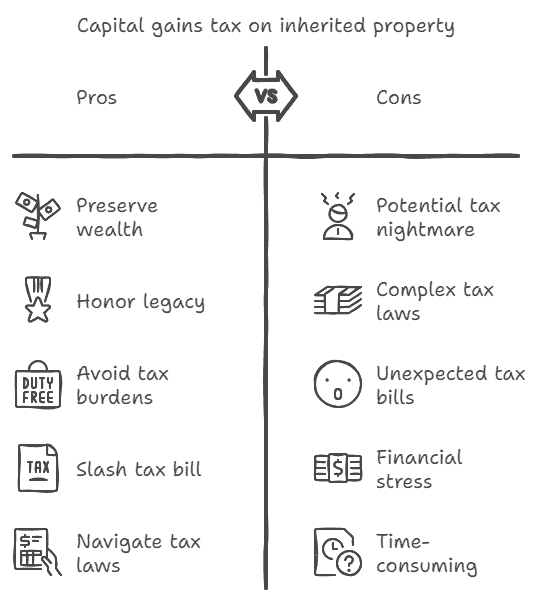

Whether you’re dealing with a family home, rental property, or vacation getaway, mastering the intricacies of capital gains tax on inherited property is crucial for:

- Preserving your wealth

- Honoring your loved one’s legacy

- Avoiding unexpected tax burdens

In this comprehensive guide, we’ll look at:

- The power of the “step-up in basis” rule and how it can slash your tax bill

- Actionable strategies to minimize or avoid capital gains tax altogether

- Expert insights on navigating complex tax laws with confidence

Ready to transform your inheritance from a potential tax nightmare into a true financial blessing? Let’s dive in and unlock the secrets to keeping more of your inherited wealth where it belongs – in your pocket.

Interactive Inherited Property Tax Estimating Calculator

Capital Gains Tax Calculator – Inherited Property

Capital Gains Tax Calculator – Inherited Property

How to Use:

- Enter the original purchase price, the stepped-up basis, and the sale price of the inherited property.

- Select the appropriate filing status.

- Click the “Calculate Capital Gains Tax” button to see the tax owed.

This tool simplifies understanding capital gains tax obligations when selling inherited property, particularly with the benefit of the stepped-up basis. Keep in mind, it is meant to be used as just an estimate and to speak with a tax professional.

Related reading: Find out if your Inheritance is Taxable?

Key Takeaways on Avoiding or Reducing Capital Gains Tax On Inherited Property

- Do I always have to pay capital gains tax on inherited property?

No – strategically using the step-up in basis rule can significantly reduce or eliminate your tax liability. - How does the step-up in basis work for inherited property?

The property’s tax basis is adjusted to its fair market value at the time of the original owner’s death, potentially minimizing taxable gains. - What’s the fastest way to avoid capital gains tax on inherited property?

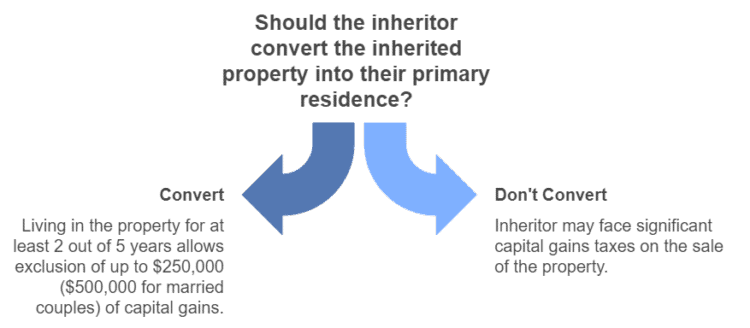

Selling the property soon after inheriting can minimize gains, potentially resulting in little to no tax owed. - Can I use the inherited property as my primary residence to save on taxes? Yes – living in the property for at least 2 out of 5 years before selling allows you to exclude up to $250,000 ($500,000 for married couples) of capital gains.

- Are there ways to defer capital gains tax on inherited investment property?

Consider a 1031 exchange to reinvest proceeds into another investment property, deferring capital gains tax.

- Learn more about What You Need To Know About Taxes on an Inheritance

Quick Links: I Inherited a Property. How Can I Avoid Capital Gains Tax?

Strategies to Minimize or Avoid Capital Gains Tax

Now that you understand the basics of capital gains tax and the step-up in basis, let’s explore 7 strategies to help you minimize or avoid paying capital gains tax on inherited property:

| Financial Benefits of Selling | Description |

|---|---|

| Liquidity | Selling inherited property provides liquid cash for various purposes (e.g., investing, paying debts) |

| Avoidance of Ongoing Costs | Selling inherited property eliminates ongoing ownership responsibilities (e.g., property taxes, insurance) |

1. Leverage the “Step-Up in Basis” Rule

The step-up in basis rule is your most powerful ally in reducing tax liability. Here’s how stepped-up basis works:

- The property’s tax basis is adjusted to its fair market value at the time of the original owner’s death.

- You’re only taxed on appreciation that occurs after you inherit the property.

Example: If a property was purchased for $200,000 and valued at $500,000 at the time of death, your new tax basis is $500,000. Selling it for $510,000 means you’re only taxed on the $10,000 gain, not $310,000.

2. Sell the Property Immediately

Why wait? Selling soon after inheriting can minimize your tax burden:

- The value of the property may not have increased much since the inheritance. Meaning your tax liability could be very low or even nonexistent.

- Potential for little to no taxable gain.

Pro Tip:

Consider market conditions and your financial needs before making a quick sale.

Example:

You inherit a property valued at $300,000. If you sell it within a few months for $305,000, you would only owe tax on the $5,000 gain.

3. Convert the Property to Your Primary Residence

Question: Could living in your inherited property for a few years save you hundreds of thousands in taxes? Yes, living in the property to unlock significant tax benefits:

By living in the inherited property as your primary residence for at least two out of the five years before selling, you can exclude up to $250,000 of capital gains ($500,000 for married couples filing jointly).

Key Points:

- Occupy the home for at least 2 out of 5 years before selling.

- Exclude up to $250,000 of capital gains ($500,000 for married couples).

- This strategy is ideal if you need a new home and wish to avoid significant capital gains taxes.

Example:

After living in the inherited property for two years, you sell it for $400,000 more than its stepped-up basis. As a single filer, you can exclude $250,000 of that gain, paying tax on only $150,000.

Learn more about how to avoid paying capital gains tax on inherited property here.

4. Rent the Property

Renting out the inherited property can defer your tax liability while generating rental income. This strategy allows you to wait for more favorable market conditions and potentially take advantage of tax deductions related to rental expenses.

Renting out the inherited property offers multiple advantages:

- Defer tax liability

- Generate rental income

- Benefit from depreciation deductions

Tip: Consult a tax professional to maximize rental property deductions.

Example:

You inherit a vacation home, decide to rent it out, and generate income for five years. Over time, you benefit from depreciation deductions, and the property’s value increases before you decide to sell.

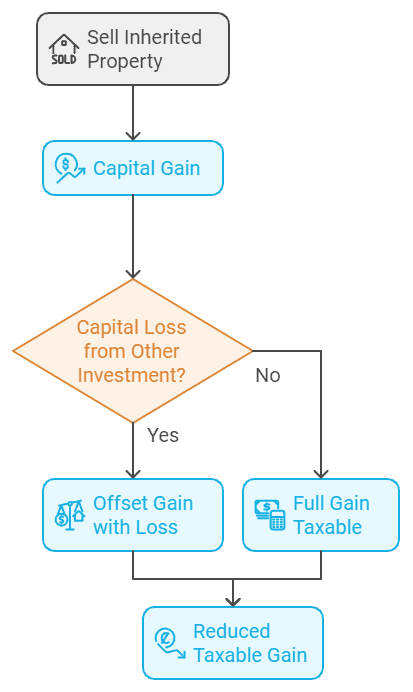

5. Offset Gains with Losses

Use tax-loss harvesting to your advantage:

- Offset gains from the inherited property with losses from other investments.

- Reduce or eliminate your capital gains tax burden.

Example:

You sell stocks at a $30,000 loss, which can offset part of the $50,000 gain from selling your inherited property, reducing your taxable gain to just $20,000.

6. Consider a 1031 Exchange (For Investment Properties)

If the inherited property was used for investment purposes, you might consider a 1031 exchange. This allows you to defer capital gains tax by reinvesting the proceeds into another investment property.

Key Requirements:

- Both properties must be used for investment or business purposes.

- The new property must be identified within 45 days and acquired within 180 days of selling the old one.

Example:

You inherit a rental property worth $500,000 and use a 1031 exchange to acquire a small apartment building. This defers your tax liability and increases your rental income.

Warning: 1031 exchanges have strict rules. Always consult with a qualified intermediary. I suggest you read my full in-depth article that discusses a 1031 exchange here.

7. Donate the Property to Charity: A Win-Win Solution

Not reliant on the sale proceeds? Consider donating:

- Avoid capital gains tax completely.

- Potentially qualify for a charitable deduction.

- Support a cause you care about.

- Ensure donations go to qualified 501(c)(3) charities.

Example:

You donate the inherited property to a charitable organization and potentially receive a deduction based on the property’s fair market value.

Another related option would be to disclaim the inheritance. As an heir, you can renounce or waive your rights to the inheritance.

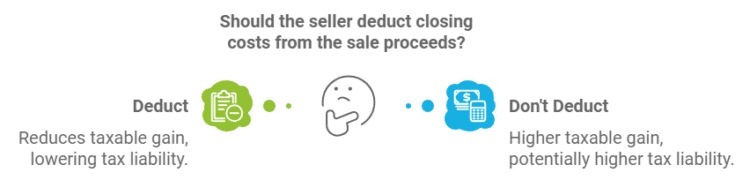

8. Deduct Closing Costs When Selling

Certain closing costs incurred during the sale, such as real estate agent fees and legal fees, can be deducted from the sale proceeds, reducing your taxable gain.

Example:

You sell an inherited property for $400,000 but incur $20,000 in closing costs. This reduces your taxable gain to $380,000.

Gift Property Before Death

If you’re planning ahead, gifting property before death can remove it from your taxable estate entirely. Under 2026 IRS rules, you can gift up to $18,000 per recipient per year without triggering gift tax reporting requirements (annual exclusion). Larger gifts reduce your lifetime gift tax exemption ($13.99 million in 2025, indexed for inflation).

When you gift property during your lifetime, the recipient receives your cost basis (carryover basis), not a stepped-up basis. This means they’ll owe capital gains tax on the appreciation when they sell.

Benefits:

Removes property from your taxable estate

Reduces estate tax exposure for high-net-worth individuals

Allows you to see your heirs benefit during your lifetime

Drawbacks:

Recipient loses stepped-up basis benefit

May trigger gift tax filing requirements

Irrevocable once completed

Example:

You gift a rental property worth $300,000 (your basis: $150,000) to your daughter. She receives your $150,000 basis. If she sells for $300,000, she owes capital gains tax on $150,000 of gain. If she had inherited it after your death, her basis would step up to $300,000 (fair market value at death), eliminating the capital gains tax entirely.Gift Property Before

Use an Irrevocable Trust for Estate Planning

Understanding Capital Gains Tax Rates

Knowing your tax bracket is crucial. Here are the capital gains tax rates for 2026 (IRS Revenue Procedure 2025-44, November 2025):

| Filing Status | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Single | Up to $49,450 | $49,451 – $545,500 | Over $545,500 |

| Married Filing Jointly | Up to $98,900 | $98,901 – $613,700 | Over $613,700 |

| Head of Household | Up to $66,200 | $66,201 – $579,600 | Over $579,600 |

Note: These rates are for long-term capital gains and are adjusted annually. Always verify current rates with a tax professional.

Key Considerations When Selling Inherited Property

- Accurate Property Valuation: Hire a professional appraiser to determine the fair market value at the time of inheritance.

- State-Specific Laws: Research your state’s inheritance and capital gains tax laws, as they can vary significantly.

- Professional Advice: Consult with a tax professional or estate planning attorney to navigate complex regulations and maximize tax-saving strategies.

Thoroughly understand your responsibility around tax forms like:

- Schedule D for capital gains and losses

- Form 8960 for the Net Investment Income Tax

- Form 8949 for sales details

Professional Insights: Expert Tips for Inheriting Property from Tax Attorneys, Accountants, and Wealth Managers

With intricate tax codes spanning hundreds of pages, trying to uncover all available deductions by yourself can be an exercise in futility. Enlisting qualified finance professionals pays dividends through tailored tax planning.

We asked specialty tax attorneys, CPAs, and financial advisors for their best tips for inheriting property while minimizing tax liabilities.

Tax Attorney Tips

“Inheriting property offers wonderful financial potential, but also opens the door to capital gains taxes that can take huge bites out of your profits if you aren’t smart about sales,” says Martha Hanson, legacy and estate planning tax attorney.

Estate Tax Attorney Martha Hanson’s Top Tips For Heirs:

- “First and foremost, consult a tax pro to understand capital gains cost basis – that is key! Then explore whether strategies like a 1031 exchange or primary residence conversion make sense for your financial life stage.”

- “For retirement-focused heirs, gifting highly appreciated assets to kids in lower tax brackets and leaving less tax-burdened assets in IRAs or 401ks can really optimize inheritances.”

Certified Public Accountant Strategies

“Understanding date of death valuations is critical for utilizing that stepped-up cost basis to minimize inherited capital gains taxes,” advises Bradley Wu, CPA.

- “Documentation is also key as heirs must prove basis amounts should their tax return face scrutiny. An independent appraisal from an IRS-approved professional valuer goes a long way to validating basis value claims.”

Other CPA tips include:

- Explore a Qualified Personal Residence Trust to transfer residences to beneficiaries while retaining living rights

- Donate appreciated property to philanthropic taxpayers like Donor Advised Funds and avoid capital gains tax completely while benefitting charity

Wealth Manager Guidance

- “One often overlooked strategy is gifting highly appreciated assets to family members in lower income tax brackets – children or elderly parents, for instance,” counsels Clara Kent, Certified Financial Planner.

- “By gifting assets set to trigger high capital gains tax, you spread that tax liability across gift recipients who likely fall into much lower tax brackets.”

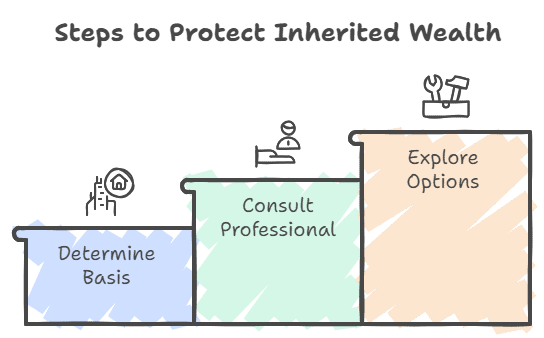

Wrapping Up: Take Action to Protect Your Inherited Wealth

Ready to unlock the full potential of your inheritance? Follow these steps:

- Determine the stepped-up basis of your property through professional appraisal.

- Consult a tax professional to develop a personalized tax-minimization strategy.

- Explore options like renting, charity donations, or offsetting gains with losses.

By leveraging these strategies and understanding the nuances of capital gains tax on inherited property, you can significantly reduce your tax burden and preserve your family’s legacy.

| Consideration | Potential Impact | Risk of Overlooking |

|---|---|---|

| Stepped-Up Basis | High | Very High |

| Professional Advice | Medium to High | Medium |

| Accurate Valuation | High | High |

| State-Specific Laws | Medium to High | Medium |

Have questions about your specific inherited property situation? Use our interactive Capital Gains Tax Calculator to estimate your potential savings and take the first step toward financial clarity.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.

Frequently Asked Questions

Do I Have To Pay Capital Gains Tax On Inherited Property?

You typically don’t pay capital gains tax on the inheritance itself, but you will owe tax when you sell the property. Thanks to the stepped-up basis rule (IRC Section 1014), your cost basis resets to the property’s fair market value on the date of the decedent’s death. You only pay capital gains tax on appreciation that occurs after you inherit it, not on the original owner’s gains.

What Is The Stepped-Up Basis And How Does It Work?

The stepped-up basis adjusts your property’s cost basis to its fair market value on the date of the decedent’s death (or alternate valuation date, 6 months later). For example, if the original owner bought property for $100,000 and it’s worth $400,000 at death, your basis steps up to $400,000. This eliminates $300,000 of potential capital gains. You only pay tax on appreciation above $400,000 when you sell.

Can I Avoid Capital Gains Tax By Living In The Inherited Property?

Yes. If you convert the inherited property into your primary residence and live in it for at least 2 out of 5 years before selling (IRC Section 121), you can exclude up to $250,000 ($500,000 for married couples filing jointly) of capital gains from taxation. This primary residence exclusion stacks on top of the stepped-up basis benefit, potentially eliminating all capital gains tax.

What Is A 1031 Exchange And Can It Help Me Avoid Capital Gains Tax?

A 1031 exchange (IRC Section 1031) allows you to defer capital gains tax by reinvesting sale proceeds into a like-kind investment property. Both properties must be held for investment or business use. You must identify replacement property within 45 days and close within 180 days. This defers, not eliminates, capital gains tax until you sell the replacement property without exchanging it.

Do Multiple Heirs Split Capital Gains Tax On Inherited Property?

Yes. Each heir receives a proportional stepped-up basis based on their ownership percentage. When the property sells, each heir reports capital gains on their individual tax return based on their share of proceeds minus their stepped-up basis. For example, if three siblings inherit equally, each reports one-third of the total capital gain on their personal Form 1040, Schedule D.