You did it. You won the game. By saving aggressively & living intentionally, you’ve achieved the dream of early retirement. But as you stare at that massive 401(k) or IRA balance, you’re realizing the game isn’t over.

You’ve just reached the final boss: a multi-million-dollar tax time bomb.

As a financial planner for 3 decades, I’ve seen the FIRE community master the art of accumulation. But the art of de-accumulation is a completely different, and FAR more complex challenge. The conventional wisdom to “just convert in your low-income years” is dangerously simplistic for an early retiree.

Your entire retirement before age 73 is a “low-income” period.(The RMD age is 73 for those born between 1951 and 1959, per the SECURE 2.0 Act.)

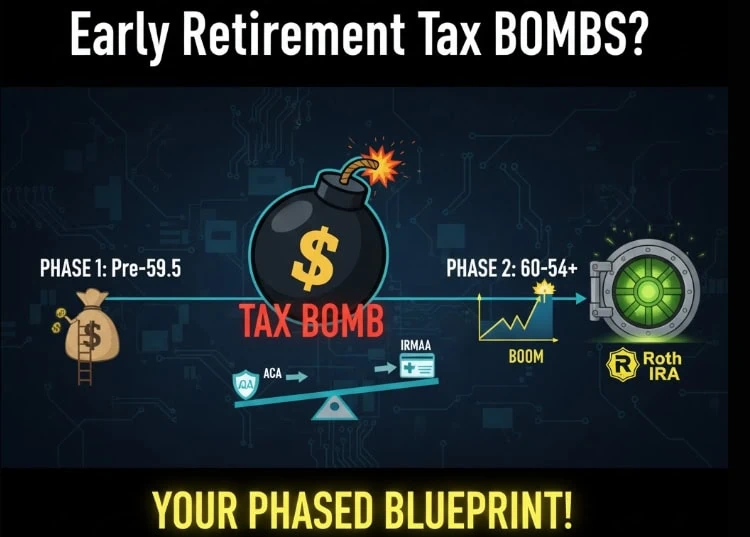

The real challenge is navigating three conflicting financial minefields at once:

- The pre-59.5 withdrawal penalties

- The treacherous ACA subsidy cliff

- The looming threat of Medicare IRMAA surcharges.For 2026, IRMAA applies to beneficiaries with Modified Adjusted Gross Income (MAGI) exceeding $109,000 (single filers) or $218,000 (married filing jointly) based on their 2024 tax returns.

This is your year-by-year blueprint for turning that tax bomb into a controlled, strategic burn.

⚡ Key Takeaways

- Early Retirement Isn’t One Phase, It’s Three: Your strategy must be broken down by age: Phase 1 (Ages 55-59.5) focuses on penalty-free access, Phase 2 (Ages 60-64) is a delicate balance of ACA subsidies vs. IRMAA prevention, and Phase 3 (Age 65+) is about managing income under Medicare rules.

- Don’t Be Penny-Wise and Pound-Foolish with ACA Subsidies: Maximizing your health insurance subsidy every year can feel smart, but it often means under-converting your IRA. It’s sometimes better to pay a little more for healthcare now to save a fortune on RMD and IRMAA taxes later.

- The “Golden Window” is Still Golden: The years between age 60 and 63 are your last, best chance to make large Roth conversions that will be invisible to Medicare’s 2-year IRMAA lookback. This is a one-time opportunity you can’t afford to miss.The 2-year lookback means your 2026 Medicare premiums are determined by your 2024 income, creating a strategic window before age 65.

- A Roth Conversion Ladder is Your First Move: If you retire before 59.5, your first priority is establishing a 5-year Roth conversion ladder to create a pipeline of penalty-free cash to live on.

The Core Problem: Trading a Subsidy Today for a Tax Bomb Tomorrow

The single biggest mistake I see early retirees make is optimizing for the wrong thing.

They become experts at keeping their Modified Adjusted Gross Income (MAGI)(your adjusted gross income plus tax-exempt interest) just below the “ACA subsidy cliff” to get the maximum discount on their health insurance premiums. While this saves money in the short term, it means they are barely touching their huge pre-tax retirement accounts.

The result?

That $2 million 401(k) continues to grow, untouched and untaxed. By the time Required Minimum Distributions (RMDs) begin at age 73, the balance could be $3 or $4 million.

The forced annual withdrawals will be massive, catapulting them into the highest tax brackets and triggering the top-tier IRMAA surcharges for the rest of their lives.

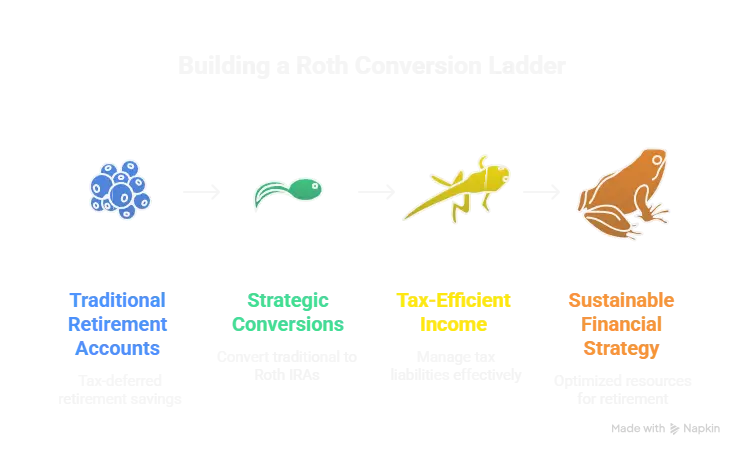

Phase 1 (Ages 55-59½): Building Your Pipeline with a Roth Conversion Ladder

If you retire before age 59.5, your first problem is simple. How to get money out of your retirement accounts without paying a 10% early withdrawal penalty.

The solution is a Roth conversion ladder.

Here’s how it works:

- Each year, you convert a portion of your Traditional IRA to a Roth IRA.

- You pay ordinary income tax on the converted amount that year.

- After a 5-year waiting period for each conversion, you can withdraw that specific converted amount (the “principal”) tax-free and penalty-free. For a deep dive into the mechanics, see our comprehensive guide on the Roth IRA 5-year rule.

🚀 Your First 5 Years of Retirement (Example)

- Year 1 (Age 55): Convert $60,000. Pay tax on it.

- Year 2 (Age 56): Convert $60,000. Pay tax.

- …and so on for 5 years.

- Year 6 (Age 60): You can now withdraw the $60,000 from Year 1, completely tax- and penalty-free, to live on. You also make a new $60,000 conversion to keep the ladder going.

Phase 2 (Ages 60-64): The ACA Subsidy vs. IRMAA Prevention Tightrope

This is the most complex phase of your early retirement. You are now over 59.5, so the 10% penalty is gone. Your two competing goals are:

- Keep your MAGI low enough to get an affordable health insurance plan on the ACA Marketplace.

- Convert enough from your traditional IRA to a Roth IRA to reduce your future RMDs and avoid the IRMAA bombs.

These two goals are in direct conflict. Why? Because Roth conversions increase your MAGI.

This is where the “subsidy cliff” comes in. For example, earning just one dollar over 400% of the Federal Poverty Level can cause your health insurance premium subsidies to disappear, potentially costing you over $10,000 a year.Note: The 400% FPL subsidy cliff returned in 2026, reinstating the hard cutoff that was temporarily eliminated during 2021-2025.

💡 Defuse Your Tax Bomb & Win Retirement

One clear financial move each week, straight from 28 years of seeing what goes wrong.

- → Master Roth conversion timing.

- → Learn to navigate ACA & IRMAA rules.

- → Get proven RMD-avoidance strategies.

💡 AVOID IRMAA TRAPS & MAXIMIZE ROTH WINS

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Discover your “Golden Window” for conversions

- → Prevent costly Medicare IRMAA surcharges

- → Get proven tax-saving retirement strategies

Get money moves like this delivered every week — before the costly mistakes happen.

📬 No spam. Unsubscribe.

The IRMAA “Golden Window” (Ages 60-63)

While managing ACA subsidies is important, you cannot forget about Medicare. Because of the 2-year lookback, your income at age 63 determines your Medicare premiums at age 65. This means the years before age 63 are a “golden window” to perform larger Roth conversions that will be invisible to your initial IRMAA calculation.

Failing to use this window is one of the biggest IRMAA mistakes even tax professionals can make.

The Strategy:

In these years, it may be worth “breaching” the 400% FPL, paying more for health insurance for a year or two, in order to execute a much larger, IRMAA-free Roth conversion that will save you far more in the long run.

Phase 3 (Age 65+): The Game Changes Again

Once you enroll in Medicare, the ACA subsidy concern is gone. Your new focus is keeping your MAGI below the annual IRMAA thresholds. At this point, your ability to do large Roth conversions is limited.For 2026, the standard Medicare Part B premium is $202.90 per month. IRMAA surcharges begin when MAGI exceeds $109,000 (single) or $218,000 (married filing jointly), with total premiums ranging from $284.10 to $689.90 depending on income level.

The goal now is to perform smaller, “bracket-filling” conversions each year, moving just enough to fill up the 22% and 24% tax brackets without triggering the next IRMAA surcharge cliff.

Read Deeper on This Strategy

- Master the Roth Conversion Rules – Our definitive guide to the mechanics, tax implications, and common pitfalls of all Roth conversions.

- Learn 5 Core Strategies to Avoid IRMAA – Go beyond timing and learn about the other tools you can use to keep your MAGI under control.

- Review the IRS Rules on RMDs – Understand the official regulations for when you must start taking distributions from your pre-tax accounts.

Frequent Reader Questions

How much should I convert each year before age 65?

It’s a balance. You need to convert enough to create your living expense “ladder” for ages 55-59.5. After that, you should model the trade-off: is the long-term tax saving from a larger conversion greater than the short-term loss of an ACA subsidy? Often, paying an extra $5,000 in premiums for one year to convert an extra $100,000 is a fantastic deal.

What if I have a pension or other income?

Any other taxable income (pensions, rental income, etc.) reduces the amount of “space” you have in a given tax bracket for conversions. You must factor in all sources of income when calculating your MAGI for both ACA and IRMAA purposes.

Is it ever a good idea to just avoid conversions and live off my taxable brokerage account?

Living off a taxable account is a key strategy for the early years. However, this only delays the RMD problem. Your tax-deferred accounts continue to grow, making the eventual RMDs even larger. A balanced approach involves using both taxable funds and strategic, small conversions to defuse the tax bomb over time.

Your Next Steps

You’ve mastered the accumulation phase of retirement, but the real challenge (and opportunity) lies in skillfully de-accumulating your tax-deferred wealth. As shown, navigating early retirement isn’t just about preserving capital; it’s about executing a precise, multi-phase tax strategy to disarm your multi-million-dollar tax bomb.

The journey through pre-59.5 penalties, ACA subsidy cliffs, and looming IRMAA surcharges requires a blueprint, not simplistic advice.

Don’t let your hard-earned savings become a future tax burden. Take control by: understanding your “Golden Window” for conversions, balancing ACA subsidies against long-term tax savings, and establishing a Roth conversion ladder if you’re an early retiree.

Here’s how to act this week: Begin modeling your phased approach to Roth conversions and ensure you’re turning potential tax traps into strategic wins.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.