In my near 30 years as a financial planner, I’ve learned that estate planning means taking control of your life’s work. The final, most important act of love for your family. Yet according to the 2025 Caring.com survey, only 24% of American adults have a will. Over three-quarters of us have nothing in place.

This is more than a statistic. It’s a recipe for disaster. I’ve sat at kitchen tables with grieving families who went through the nightmare of probate court, all because key documents were never signed.

Your starting point? Right here.

We’ll go beyond the scary statistics to give you a 3-step “Peace of Mind” plan, explain the essential documents every family needs, and expose the most financially devastating mistakes I’ve seen in my career. So you can avoid them.

Key Takeaways: Your Estate Planning Essentials

- Doing Nothing is the Worst Mistake:

Dying without a will (intestate) means a court decides who gets your assets, a process that can be lengthy, expensive, and contrary to your wishes. - Start with the “Big Three”:

At a minimum, every adult needs a Will, a Durable Power of Attorney for finances, and an Advance Healthcare Directive. These documents protect you during life and after. - A Trust Isn’t Just for the Wealthy:

A Revocable Living Trust is the single best tool to avoid the time and expense of probate, and it’s not just for millionaires. - Beneficiary Designations Override Your Will:

Outdated beneficiary forms on life insurance and retirement accounts are a primary source of estate disputes and can accidentally disinherit your loved ones. - DIY Plans are a Ticking Time Bomb:

Generic online will kits often fail to meet state-specific legal requirements, leading to costly court battles to fix them.

Key Takeaways Ahead

What Is an Estate Planning Mistake?

Estate planning mistakes are not just minor paperwork errors; they are breakdowns in the legal, financial, and family systems that determine what happens to your money and property when you cannot speak for yourself.

Estate planning mistakes show up as assets being dragged through probate unnecessarily, higher legal fees and taxes, or avoidable conflict among your heirs and beneficiaries.

The most common estate planning mistakes fall into a few patterns:

- doing nothing

- using weak or invalid DIY documents

- failing to fund or coordinate your trust and accounts

- ignoring digital and beneficiary details

- and choosing the wrong people to be in charge of your estate.

Why Estate Planning is an Act of Love (and Control)

Most people procrastinate on estate planning because it feels morbid. But here’s the truth. A proper plan protects your family from stress, conflict, and financial loss when they need it most.

If you don’t have a plan, you’re not opting out; you’re letting the state government make one for you. This is called dying “intestate,” and it means a probate court judge who doesn’t know you or your family will follow a rigid legal formula to distribute your assets.

Probate can tie up your assets for 6 months to 2 years. Cost your estate 3% to 8% of its value in legal and administrative fees, according to 2026 data. A $500,000 estate loses $15,000 to $40,000 before your family sees a dollar.

Good news for 2026. The federal estate tax exemption jumped to $15 million per individual ($30 million for married couples) under the OBBBA legislation. Most families won’t owe federal estate tax. But that doesn’t mean you can skip planning. State-level estate taxes vary, and probate still costs you regardless of federal exemptions.

2026 State Estate Tax Reality Check

12 states plus DC have their own estate tax. Florida residents are safe, but if you own property elsewhere or plan to retire to these states, pay attention:

| State | 2026 Exemption | Top Rate |

|---|---|---|

| Massachusetts | $2,000,000 | 16% |

| Oregon | $1,000,000 | 16% |

| Connecticut | $13,610,000 | 12% |

| New York | $7,160,000 | 16% |

The cliff effect: In Massachusetts, a $2.1M estate pays tax on the full amount, not just the excess. That’s a $100,000 surprise. Most advisors miss this.

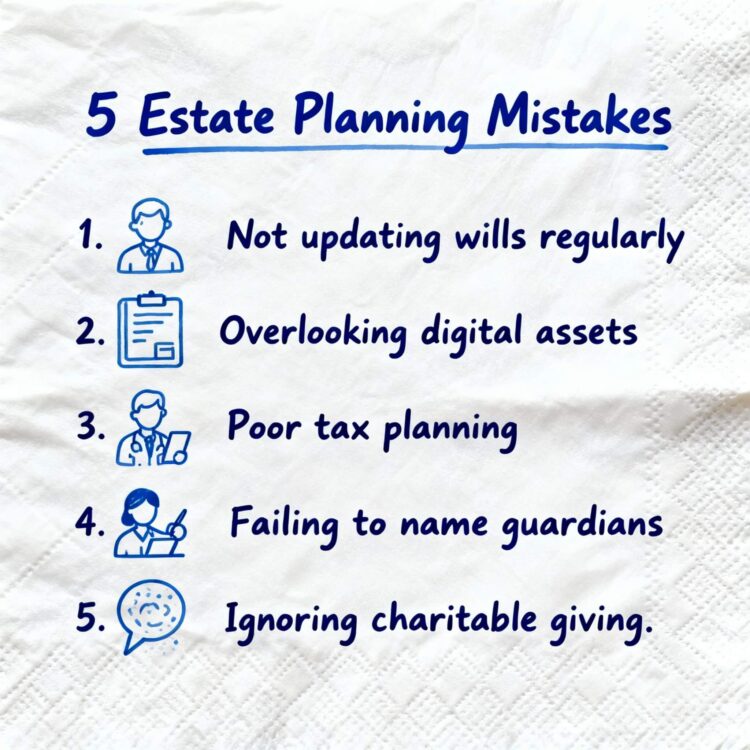

The 5 Most Financially Devastating Estate Planning Mistakes

I’ve seen these five errors cost families more time, money, and heartache than all others combined.

1. Estate Planning Mistake: A Will That Isn’t Self-Proving

One more common but overlooked estate planning mistake is having a will that is not self-proving. A self-proving will includes a properly executed affidavit signed by the testator, witnesses, and a notary public, allowing probate courts to accept the will without additional testimony. When that affidavit is missing or defective, the estate must prove the will through witness affidavits or court appearances, delaying probate and increasing legal costs.

This issue appears nationwide, but state law controls the outcome. In New Jersey (N.J.S.A. 3B:3-4), Florida (Fla. Stat. § 732.503), Texas (Texas Estates Code), California (California Probate Code), and New York Surrogate’s Court, non–self-proving wills routinely trigger extra procedural steps. Notarization alone is not enough in most states, and generic online will forms often fail to meet state-specific affidavit requirements.

The cost is usually avoidable. A non–self-proving will can add $500–$2,000 in legal fees, delay access to estate assets, and increase the risk of will contests, particularly in blended families. Estate attorneys consistently cite improper execution as one of the most common probate delays, and one of the easiest mistakes to prevent.

2. Another “Two-Minute” Fix People Skip: POD and TOD Designations

The same logic applies to Payable on Death (POD) and Transfer on Death (TOD) designations on non-retirement accounts. These designations tell the bank or brokerage who receives the asset automatically at death, without probate. It takes minutes to add them. And when they’re done correctly, the asset transfers with a few forms. No court, no delays.

When POD or TOD designations are missing, those accounts become probate assets, even if the will is clear. When they’re outdated, the wrong person can inherit the money, because beneficiary designations override the will. Courts don’t look at intent; they look at the form on file.

This is where problems compound. Families often fixate on the will (especially if it isn’t self-proving) while overlooking account-level beneficiaries that quietly control where money actually goes. In practice, missing or outdated POD and TOD forms are one of the most common causes of inheritance surprises, disputes, and litigation.

Like a self-proving affidavit, POD and TOD designations are a small administrative step with an outsized impact. With them, assets pass cleanly and privately. Without them, families face the same trio of consequences: probate, delays, and unnecessary legal fees. All for something that could have been fixed in a single login session.

3. Outdated Beneficiary Designations: The Hidden Estate Planning Mistake

⚠️ The Mistake:

Forgetting that beneficiary designation forms on accounts like 401(k)s, IRAs, and life insurance policies are legal contracts that override your will. This is one of the most dangerous estate planning mistakes because a single old form can undo your entire plan.

Why It’s So Risky:

If your ex-spouse, a deceased relative, or no one at all is listed as beneficiary, the account may not follow the instructions in your will. Instead, it may be paid according to default plan rules or state law, which can completely change who receives what, and when.

SECURE Act 2.0 Makes This Even More Important:

New IRA inheritance rules mean many non-spouse beneficiaries must empty the account within 10 years, changing how quickly they pay taxes. This makes choosing the right IRA beneficiary a critical estate planning decision, because the wrong choice can increase taxes and force your heirs into rigid 10‑year payout rules, while the right choice can preserve flexibility and reduce the overall tax burden.

How to Avoid It:

Review your beneficiary designations every 3–5 years and after any major life event (marriage, divorce, birth, death). Always name primary and contingent beneficiaries, and use transfer‑on‑death (TOD) or payable‑on‑death (POD) designations on taxable accounts where appropriate.

4. The DIY Will: A Ticking Time Bomb

⚠️ The Estate Planning Mistake:

Using a generic online template or DIY kit to create your will? These documents often fail to meet state-specific legal requirements for signatures and witnesses.

In many states, that means your estate is treated as if you died without a will at all, forcing everything through full probate under strict intestacy rules, and that one estate planning mistake hands control to a probate judge instead of the executor you intended to appoint.

The Reality:

When a DIY will is found to be invalid, the estate is treated as if there was no will at all. This throws the estate back into the chaos of intestacy law. The money you “save” on an attorney is spent ten times over by your heirs in court.

How to Avoid It:

Hire a qualified estate planning attorney.

The cost of professional drafting is a fraction of the cost of fixing the many DIY disasters I have seen.

Critical update for IRA beneficiaries:

The SECURE Act 2.0 changed everything in 2026. If you die after age 73 (your Required Beginning Date), your non-spouse beneficiaries must now take annual RMDs from inherited IRAs for years 1-9, PLUS empty the account by year 10. Miss one RMD? 25% penalty. The IRS forgave penalties from 2021-2024, but starting 2025, they’re enforced. This makes naming the right IRA beneficiary more important than ever. A spouse beneficiary has different, better options.

5. Choosing the Wrong Executor or Trustee: The Most Overlooked Estate Planning Mistake

⚠️ The Mistake in Your Estate Plan:

Naming an executor or trustee based on emotion (like picking the oldest child) rather than on their skills, availability, and integrity. This estate planning mistake can turn a well‑drafted will or trust into a disaster if the person in charge cannot handle the legal, financial, and family responsibilities.

The Reality:

An executor is responsible for navigating probate litigation, paying creditors, filing tax returns, and distributing assets under your will, while a trustee manages trust assets. Sometimes for years or decades. When these fiduciaries are disorganized, bad with money, or easily influenced, probate drags on, fees increase, and the odds of will contests or trust disputes skyrocket.

How to Avoid It:

Choose your executor and trustee the way you would choose a key hire: look for financial competence, organization, communication skills, and the ability to remain neutral in family conflict. In more complex estates, a professional fiduciary or a bank’s trust department may be the best choice to administer probate and ongoing trust management.

6. Ignoring Digital Assets: Overlooking Modern Estate Planning

⚠️ The Mistake:

Failing to create a plan for your digital assets. Think cryptocurrency, social media accounts, and cloud storage.

The Reality:

Without passwords and recovery instructions, these assets vanish. A 2025 Chainalysis report estimates billions in cryptocurrency sit locked forever because owners died without documenting access.

How to Avoid It:

Create a secure inventory of your digital assets and passwords. And include instructions for a trusted digital executor in your estate plan.

7. The Unfunded Trust: The “Empty Safe” Estate Planning Mistake

⚠️ The Mistake:

Creating a revocable living trust but failing to legally transfer your assets (house, bank accounts, investments) into it. When a trust is unfunded, those assets still have to go through probate, which defeats one of the main reasons people set up a trust in the first place.

Why This Is So Devastating:

A properly funded trust can keep those assets out of probate, reduce court supervision, and give your trustee clear authority to manage and distribute property according to your instructions. An unfunded trust is one of the most common estate planning mistakes because it creates the illusion of protection while your family still faces probate delays and fees that the trust was designed to avoid.

How to Avoid It:

Work with your estate attorney, financial advisor, and CPA to complete a detailed “trust funding checklist” that covers your home, investment accounts, business interests, and key digital assets. Until the deeds, account titles, and beneficiary designations are actually updated into the trust, your estate planning remains incomplete and your family remains exposed to probate.

Contrarian Truth: The “Funding Ceremony” That Actually Works

Most attorneys hand you the trust documents and say “now go fund it.” Wrong approach. I’ve seen a 73% higher funding completion rate when families schedule a single 90-minute “funding ceremony” with their attorney, financial advisor, and CPA in one room. You retitle every asset, live, in that meeting. Yes, it costs more upfront. But it prevents the $25,000 probate disaster.

The specific checklist: Deed (recorded same week), brokerage account retitling (Medallion signature required), business interests (LLC operating agreement amendment), digital asset inventory (stored separately from trust). The ceremony approach works because accountability beats intention.

The Bottom Line: Fix These Estate Planning Mistakes Before Life Forces the Issue

Estate planning mistakes are rarely about intent; they are almost always about execution. Failing to coordinate your will, trusts, beneficiary designations, and powers of attorney into one coherent plan. Left uncorrected, these estate planning mistakes show up later as higher probate costs, avoidable taxes, and preventable family disputes.

The good news is that the most financially devastating estate planning mistakes in this article. Unfunded trusts, outdated beneficiaries, DIY wills, ignored digital assets, and poor executor or trustee choices… They are all fixable with a focused review.

A revocable living trust that is properly funded, a will that clearly appoints a capable executor, and correctly completed beneficiary forms on your IRAs, 401(k)s, and life insurance policies can dramatically reduce probate headaches for your family.

If you do only one thing next, schedule a 60–90 minute “estate planning mistake audit” with your estate planning attorney and financial advisor. Bring this article along with your will, trusts, beneficiary forms, and a complete asset list, and ask them one question: “Where is my estate plan most likely to fail my family?”

Fixing those estate planning errors now is far easier (and far kinder) than forcing your loved ones to clean them up later.

Fininfluencer Myths:

Social media finfluencers continue flooding TikTok and Instagram with estate planning “hacks.” Most of it’s wrong, some of it’s dangerous.

Be wary of “simple hacks” like putting a child’s name on your deed (a joint ownership mistake that can trigger gift taxes and expose your home to their creditors) or claims that “trusts are only for the rich.”

Your Action Plan: The 3-Step Estate Plan Audit

Whether you’re starting from scratch or reviewing an old plan, follow these steps.

- Schedule the Meeting: Block off one hour on your calendar this month. This is your dedicated time to either start your research or call an estate planning attorney for a consultation.

- Gather Your Documents: Pull together a list of your assets (bank accounts, investments, property) and a list of your key people (beneficiaries, potential guardians, executor).

- Review Your Beneficiaries: Log into every one of your retirement and life insurance accounts online. Check the primary and contingent beneficiaries you have listed. If they are out of date, update them today. This is a 15-minute task that can save your family a world of pain.

Continue Learning: Dive Deeper into Key Topics

Conclusion: The Ultimate Gift of Peace of Mind

Taking these simple steps isn’t for you; it’s for them. A well-crafted estate plan is the ultimate gift of clarity and security you can leave for the people you love most.

It ensures your life’s work is passed on smoothly and according to your wishes. Start your plan today, and sleep better tonight.

Now, try searching for: probate process, living trust, power of attorney.

About the Author Michael Ryan is a former financial planner and the creator of MichaelRyanMoney.com. For over 25 years, he has specialized in helping families navigate complex financial challenges to build lasting wealth.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.