Every tax season, it starts with a phone call. Last week, it was a client I’ll call Amanda. She’s a diligent saver and a sharp professional, but she sounded completely frustrated.

“Michael,” she said, “I just got my annual fee statement, and I can’t find where to enter it in my tax software. I thought I could deduct the fees I paid my financial advisor!“

Amanda’s frustration is perfectly logical. You’re paying for a professional advisor to manage your financial life, so it feels like it should be a business expense. Her call is why I’m writing this guide.

I’ll give you the direct answer right away: for the vast majority of individual investors like Amanda, the answer is no.

But that’s not the end of the story. The simple “no” misses the critical exceptions and, more importantly, the smarter strategies we now use to maximize tax efficiency. A major tax law change in 2017 shifted the landscape, and just knowing the old rules isn’t enough. This guide is for Amanda, and for you.

Who Should Care Most About This Change?

🎯 High Priority

Pay $10K+ annually in fees

- Portfolios $1.5M+

- Complex planning needs

- Demand aggressive tax-loss harvesting

⚠️ Medium Priority

Pay $3K-$10K annually

- Portfolios $400K-$1.5M

- Focus on asset location

- Consider robo + CPA hybrid

💡 Lower Priority

Pay <$3K annually

- Portfolios <$400K

- Old deduction rarely applied

- Keep costs low

The TCJA didn’t kill tax planning. It just moved the chess pieces

⚠️ Critical 2026 Update: This Just Got Permanent

Due to the Tax Cuts and Jobs Act of 2017 (TCJA), investment advisory fees, financial planning fees, and other miscellaneous itemized deductions were suspended for individuals from tax years 2018 through 2025.

NEW in July 2025: Congress passed the One Big Beautiful Bill Act (OBBBA), which permanently eliminated miscellaneous itemized deductions. This means you can never deduct financial advisor fees on your personal federal tax return (Form 1040) under current law. The sunset provision that would have restored these deductions in 2026 has been removed.

Bottom Line: The strategy shift from “deductible fees” to “tax-efficient portfolio management” is now permanent. Smart advisors focus on tax-loss harvesting, asset location, and Roth conversions—strategies that save far more than the old 2% AGI deduction ever did.

Advisor Fee Deductibility: A Quick Summary

| Who You Are | Are Your Fees Deductible? | The Fine Print / Key Strategy |

|---|---|---|

| Individual Investor | ❌ No | Focus on tax-loss harvesting and asset location. Consider paying fees from a Traditional IRA to use pre-tax dollars. |

| Business Owner / Self-Employed | ✅ Yes, but only the portion directly related to the business. | Requires clear documentation. Deductible on Schedule C, not Schedule A. Personal investment advice is not deductible. |

| Trust or Estate Fiduciary | ✅ Yes | Fees must be for the administration of the trust/estate and are deducted on Form 1041. |

Quick Links: Are Financial Advisor Fees Tax Deductible

The Big Change: Why Your Advisor Fees Are No Longer Deductible

Prior to 2018, you could deduct investment-related expenses, including financial advisor fees, as a “miscellaneous itemized deduction” on Schedule A. However, there was a catch: you could only deduct the amount that exceeded 2% of your Adjusted Gross Income (AGI). For many, this threshold was hard to meet.

Most high-income earners who could afford financial advisors rarely qualified for the pre-2018 deduction due to AMT limitations. Losing it affected fewer people than industry headlines suggested.

While everyone focuses on losing the deduction, smart investors actually save more through asset location than the old 2% AGI rule ever provided.

The Tax Cuts and Jobs Act (TCJA) completely changed the game. It suspended all miscellaneous itemized deductions subject to this 2% floor, a change that was originally set to expire at the end of 2025. However, in July 2025, Congress passed the One Big Beautiful Bill Act (OBBBA), which permanently eliminated these deductions. Under current law, financial advisor fees will never be deductible again for individual investors.

What fees does this impact?

- Assets Under Management (AUM) fees: The percentage fee you pay an advisor to manage your portfolio.

- Financial planning fees: Flat or hourly fees for creating a financial plan.

- IRA Custodial fees: Fees paid directly for the maintenance of your IRA accounts (if paid out-of-pocket).

Commission-based products effectively provide “deductible” advice through embedded costs, making the fee-only vs. fee-based decision more complex post-TCJA.

Don’t focus on the fee you can’t deduct. Focus on the value and tax efficiency you should be getting.

The Planner’s Edge: Understanding Section 212 and Fee Structures

The historical rule that allowed for deducting advisor fees fell under IRC Section 212, which permitted deductions for expenses related to producing or collecting income. The TCJA didn’t repeal Section 212, but it suspended the miscellaneous itemized deductions category where these fees were claimed by individuals.

This has led to a strategic conversation, explored by industry experts like Michael Kitces, about fee structures. While advisory fees are no longer deductible, the costs within certain commission-based products or mutual funds (known as embedded commissions or expense ratios) effectively reduce your investment returns on a pre-tax basis. This isn’t a “deduction,” but it achieves a similar tax-efficient outcome, making the choice between “fee-only” and “fee-based” advice more nuanced than ever.

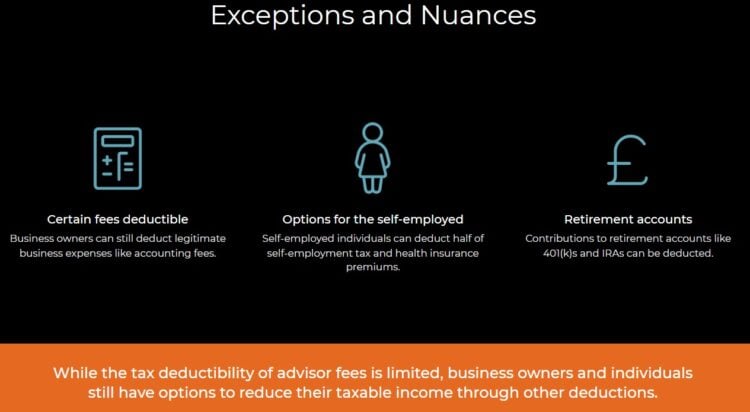

The Exceptions: When You Can Still Deduct Advisory Fees

This is where having professional guidance matters. While the door closed for most individuals, a few important windows remain open.

For Business Owners (Schedule C Filers)

If you are a sole proprietor, freelancer, or single-member LLC owner who files a Schedule C, you can deduct financial advisory fees as an ordinary and necessary business expense.

The key distinction:

The advice must relate directly to your business. For example, if you consult a planner about your business’s cash flow, succession planning, or setting up a SEP IRA, those fees are generally deductible against your business income.

CLIENT SPOTLIGHT: The Consultant’s Advantage

I have a client, a freelance marketing consultant, who pays for a comprehensive financial plan each year. We carefully document the portion of my time spent on her business strategy—optimizing her SEP IRA contributions and managing her business’s cash reserves. That portion of my fee is a legitimate business expense on her Schedule C, directly reducing her taxable business profit. This is a perfect example of a Schedule C deduction for financial advice.

- Learn more about business expenses from the IRS Publication 535

For Trusts and Estates (Form 1041 Filers)

Fees related to the administration of a trust or an estate are not considered miscellaneous itemized deductions and are therefore still deductible. This includes:

- Trustee fees

- Estate administration expenses

- Investment advisory fees paid directly by the trust or estate

These deductions are taken on the trust’s or estate’s tax return (Form 1041), not on your personal return.

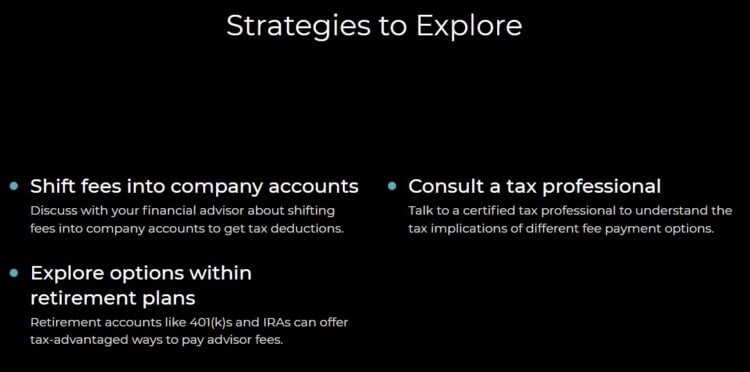

The Planner’s Pivot: Smarter Ways to Get Tax Value

Since you can no longer deduct fees directly, the modern focus has shifted to maximizing tax efficiency within your portfolio. This is often far more valuable than the old deduction ever was.

💰 The Math That Changes Everything

Scenario: $1M Portfolio, $8,000 Annual Advisory Fee

| Strategy | Annual Tax Savings |

|---|---|

| Old 2% AGI Deduction $8,000 fee – $3,000 AGI threshold = $5,000 × 24% bracket |

$1,200/year |

| Tax-Loss Harvesting Harvest $25K losses × 15% LTCG rate |

$3,750/year |

| Strategic Asset Location Moving bonds to IRA: 4% yield × 24% bracket |

$2,400/year |

Bottom Line: Modern strategies save $6,150/year — more than 5x what the old deduction provided. The OBBBA forced advisors to deliver real value.

Here are the key strategies I use with my clients:

Maximize Tax-Advantaged Accounts:

The first and best way to reduce your tax burden is to use accounts designed for it. Contributions to Traditional 401(k)s and IRAs are tax-deductible, and the investments grow tax-deferred. Contributions to Roth accounts grow tax-free. An advisor helps you optimize which accounts to use and in what order.

Strategic Asset Location:

This is a powerful but often overlooked strategy. It involves placing your least tax-efficient assets (like corporate bonds or active mutual funds that generate high turnover) inside your tax-advantaged accounts (like your IRA). Your more tax-efficient assets (like index funds or individual stocks you plan to hold long-term) are better suited for your taxable brokerage accounts.

Tax-Loss Harvesting:

At the end of the year, an advisor can help you sell investments in your taxable account that have lost value. These losses can be used to offset any capital gains you’ve realized. If your losses exceed your gains, you can use up to $3,000 per year to offset your ordinary income.

Deduct Margin Interest (Often Overlooked)

One deduction that still exists: investment interest expense under IRC Section 163(d). If you borrow on margin to purchase taxable investments, that interest is deductible up to your net investment income.

📌 Key Limitations

- Deductible only up to net investment income (capital gains, dividends, interest)

- Cannot be used for municipal bonds or retirement accounts

- Must itemize to claim (Schedule A, Form 4952)

- Excess carries forward to future years

Frequently Asked Questions

Are fees paid for a 401(k) or IRA tax-deductible?

No. If fees are paid directly from within your 401(k) or traditional IRA, they are not deductible, but they are paid with pre-tax dollars, which provides a similar benefit. If you pay them out-of-pocket for an IRA, they fall under the suspended miscellaneous itemized deductions and are not deductible on your personal return.

What about the fees for my robo-advisor?

Robo-advisor fees are treated the same as traditional advisor fees. They are considered investment management fees and are not deductible for individuals under the current tax law (TCJA).

Will the tax deduction for financial advisor fees ever come back?

No. In July 2025, Congress passed the One Big Beautiful Bill Act (OBBBA), which permanently eliminated miscellaneous itemized deductions, including financial advisor fees. The original TCJA provisions were set to expire at the end of 2025, which would have restored these deductions in 2026. However, the OBBBA removed this sunset provision, making the elimination permanent. Under current law, these deductions will never return unless Congress passes new legislation specifically restoring them.

Example: You borrow $100,000 on margin at 8% ($8,000/year interest). If you earn $15,000 in investment income (dividends + capital gains), you can deduct the full $8,000, saving $1,920 at the 24% bracket.

Final Word from Michael Ryan Money

While losing a tax deduction is never ideal, the changes from the TCJA have forced a shift towards more impactful, strategic tax planning. A good financial advisor should be saving you far more through smart strategies like asset location and tax-loss harvesting than the old deduction was ever worth.

Don’t focus on the fee you can’t deduct. Focus on the value and tax efficiency you should be getting. That’s the real measure of a successful advisory relationship.

I would suggest you read my related article about What You Need To Know About Finanical Advisor Fees as well!

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.