Most IRMAA Income calculators start by asking for your MAGI. Right?

Okay… but what if that is the number you are trying to figure out? Welcome to my IRMAA Income Checker tool – find out which of your income counts towards MAGI and IRMAA

Does an IRA withdrawal count? What about a Roth withdrawal? Capital gains? Social Security? Municipal bond interest that is supposedly “tax-free”?

That is where people get tripped up.

The part most IRMAA Income calculators skip.

IRMAA MAGI is not simply every dollar that hits your bank account. Some income counts in full. Some counts only to the extent it is taxable. Some normally does not count at all. And municipal bond interest? Tax-free does not mean IRMAA-free.

This IRMAA Income Checker helps you sort through it.

- Select the income sources or financial events that apply to you. You will get the quick answer first. “Yes, usually no, or it depends.”

- Then, only if you want the deeper answer, you can add amounts and see whether the income could push you across an IRMAA threshold.

Medicare income tool

IRMAA Income Checker

Select the income or financial events that apply to you. Get the fast answer first, then add amounts only if you want to test an IRMAA threshold.

Step 1

What income are you concerned about?

Popular choices

Retirement Income 9 choices

Investments and Savings 7 choices

Work and Business Income 4 choices

Home and Real Estate 5 choices

Other Money Received 6 choices

No matching income type found. Try a broader word such as "retirement," "property," or "interest."

Please select at least one income source.

Your quick answer

What generally counts toward IRMAA MAGI

Could these amounts push you into a higher Medicare tier?

Add your base AGI and only the proposed amounts not already included in it. The estimator compares your IRMAA cost before and after the selected income.

Step 2 - optional

Estimate the threshold impact

Selected proposed income not already in base AGI

Enter the amount described for each item. Excluded items stay visible so you can see why they add $0.

Please enter a valid base AGI of $0 or more.

Your estimated result

IRMAA threshold comparison

Quick note before you use the tool

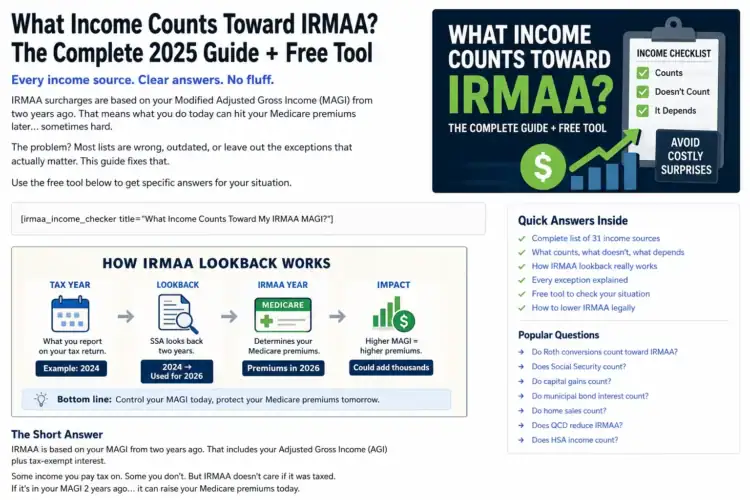

IRMAA is based on your tax return, generally from two years earlier. Your 2026 Medicare premiums are usually based on your 2024 income. The checker shows both years so you do not have to keep doing that mental math.

Key Takeaways Ahead

What Does the IRMAA Income Checker Tell You?

The tool answers the question most people actually have:

▶ Will this income or financial move count toward the MAGI Medicare uses for IRMAA?

You can use it for one income source or select several.

The first result is intentionally simple:

- Yes: It generally increases IRMAA MAGI.

- Generally no: It normally stays out of IRMAA MAGI when the rules are met.

- It depends: Only part may count, or another fact changes the answer.

That is enough for plenty of people who just want a straight answer without the financial jargon.

But money is rarely that clean. So the checker can also explain what portion counts, which exception matters, where the income usually appears on your tax return, and what question you should ask next.

Choose IRA withdrawals, capital gains, Social Security, pensions, home sales, municipal bonds, or other events.

See whether it counts, generally does not count, or needs more information.

Add amounts only if you want to estimate whether the income could move you into a higher IRMAA tier.

What Income Counts Toward IRMAA MAGI?

Here is the basic formula… IRMAA MAGI formula

IRMAA MAGI = Adjusted Gross Income + Tax-Exempt Interest

Simple formula.

Not always a simple number.

Your adjusted gross income can include wages, taxable retirement distributions, pensions, taxable Social Security, interest, dividends, capital gains, business income, rental income, and other taxable income.

Then tax-exempt interest gets added back.

That last part surprises people. Municipal bond interest can be exempt from federal income tax and still increase the MAGI used for Medicare premiums.

Again… tax-free does not mean IRMAA-free.

Social Security defines IRMAA MAGI as AGI plus tax-exempt interest. It normally uses tax information from two years before the Medicare premium year. For example, 2026 premiums are generally based on 2024 tax information.

▶ Need the full explanation behind the formula? Read what income counts toward IRMAA MAGI.

Quick IRMAA Income Reference

This is the scan-it-and-go version.

The word taxable matters. A lot.

Usually Counts

- Wages and self-employment income

- Taxable traditional IRA withdrawals

- Taxable 401(k), 403(b), and TSP withdrawals

- Required minimum distributions

- Taxable Roth conversions

- Net taxable capital gains

- Taxable interest and dividends

- Municipal bond interest

- Taxable pension and annuity income

- Net rental and business income

Usually Does Not Count

- Qualified Roth distributions

- Qualified HSA withdrawals

- Qualified charitable distributions excluded from income

- Loan proceeds

- Reverse mortgage proceeds

- Gifts received

- Cash inheritances received

- Tax-free life insurance death benefits

- Return of your own principal

It Depends

- Social Security benefits

- Home sale proceeds

- Nonqualified Roth withdrawals

- Nonqualified annuity payments

- Inherited IRA withdrawals

- Legal settlements

- HSA withdrawals for nonmedical expenses

- 1031 exchanges

- Employer stock and NUA transactions

This table is a starting point, not the entire tax code shoved into three boxes.

For example, saying an IRA withdrawal counts does not mean the gross distribution always counts dollar for dollar. If the IRA contains nondeductible contributions, part of the withdrawal may be a nontaxable return of basis.

A home sale is another easy one to misunderstand. The sale price does not simply become IRMAA income. The taxable gain after basis, selling costs, improvements, exclusions, and other rules is what may flow into AGI.

That is why the checker asks follow-up questions only when they matter.

https://www.reddit.com/r/RealWorldMoney/s/unqrOzE0cJ

Why Your Income Can Raise Medicare Premiums Two Years Later

IRMAA has a delayed punch.

You make a move this year. The Medicare bill may show up two years later.

- Sell appreciated stock in 2024? That gain may affect 2026 Medicare premiums.

- Complete a Roth conversion in 2025? The income may affect 2027 premiums.

- Take a large RMD in 2026? You may feel it in 2028.

This delay is why people get blindsided. They remember what their income looks like now. Social Security is looking backward.

Real-life example

Jim retires and his current income drops. Great. But two years earlier he sold stock and completed a large Roth conversion. His Medicare premium is based on that higher-income tax return, not the smaller checks hitting his account today.

That does not automatically mean the IRMAA determination is wrong. It means the two-year lookback is doing exactly what it was designed to do.

If retirement, work stoppage, marriage, divorce, death of a spouse, or another qualifying life-changing event reduced your income, you may be able to ask Social Security for a new determination. Start with my SSA-44 IRMAA appeal guide or use the IRMAA life-changing event checker.

The Income Sources That Surprise Retirees Most

Municipal Bond Interest

This is the classic trap.

- Municipal bond interest may be federally tax-exempt. But it gets added back when IRMAA MAGI is calculated.

- So yes, the income can avoid federal income tax and still help push you into a higher Medicare tier.

- It is not “bad” income. That is not the point.

- The point is to compare the real after-tax and after-IRMAA result. Not just the yield printed on the statement.

Roth Conversions

A Roth withdrawal and a Roth conversion are not the same thing.

- A qualified Roth withdrawal generally does not increase AGI.

- A Roth conversion generally does, to the extent the converted amount was not already taxed.

- That income can raise Medicare premiums two years later.

Does that make the conversion a mistake? No.

A conversion can still reduce future RMDs, improve survivor planning, create tax-free flexibility, and help heirs. But ignoring the IRMAA cost when you run the numbers is sloppy.

▶ Use my Roth conversion and IRMAA tradeoff guide when the checker flags a conversion.

Capital Gains

- Capital gains count.

- The entire sale price does not.

- If you sell $150,000 of stock with a $120,000 cost basis, you did not create $150,000 of gain. You created a $30,000 gain before considering losses and other adjustments.

- Same idea with a house. Sale price and taxable gain are two completely different numbers.

This sounds obvious until someone types the sale proceeds into a calculator and panics.

Social Security

Social Security is a “maybe” because the taxable portion depends on your other income.

- Up to 85% of benefits can become taxable. That does not mean Social Security is taxed at an 85% tax rate. It means up to 85% of the benefit may enter taxable income.

- That taxable portion becomes part of AGI and can affect IRMAA.

- The ugly part? More IRA income can make more Social Security taxable, which raises AGI further. Income stacking on income. Fun.

▶ See the Social Security tax threshold and IRMAA trap for a deeper example.

Required Minimum Distributions

RMDs are not optional because you do not need the money.

The taxable portion still enters AGI.

That is why IRMAA planning often starts years before the first RMD. Smaller Roth conversions in lower-income years may reduce future RMDs. Qualified charitable distributions may keep eligible charitable gifts out of AGI.

Timing matters.

▶ Read what to do with RMDs you do not need and my QCD and IRMAA guide.

How Close Are You to the Next IRMAA Threshold?

This is where the detailed part of the checker earns its keep.

IRMAA uses income tiers. It is not a smooth little percentage that rises one penny at a time.

You can be below a threshold and owe no surcharge for that tier. Cross it, even slightly, and the higher Part B and Part D amounts can apply for the year.

The $1 IRMAA problem

One extra dollar does not always cost you anything. But the dollar that pushes you across an IRMAA threshold can trigger hundreds or thousands of dollars in additional annual Medicare costs.

That is the logic behind one of the bluntest ways I explain IRMAA:

Every dollar of MAGI-increasing income can effectively cost $0.12 to $0.85 in IRMAA when it pushes you across a Medicare income threshold.

The exact result depends on filing status, household Medicare enrollment, the transaction size, and which tier you cross.

The tool compares your estimated MAGI before and after the selected income. It then shows:

- Your estimated IRMAA tier

- How far you are from the next threshold

- The projected annual household surcharge

- Whether the selected income appears to move you into another tier

- The effective IRMAA cost of that move

That does not tell you to avoid the income.

Sometimes paying IRMAA is the right tradeoff. A Roth conversion can still make sense. Selling a concentrated investment can reduce risk. Selling the house may fund the retirement you actually want.

IRMAA is a cost to include. Not a reason to let the tax tail wag the financial dog.

What Can You Do If Income May Trigger IRMAA?

- First, do not start rearranging your entire financial life to save one year of Medicare surcharges.

- Run the actual numbers.

- Then look at the moves that fit the situation.

Spread Flexible Income Across Tax Years

- Capital gains, Roth conversions, and discretionary retirement withdrawals may be flexible.

- Instead of bunching everything into one year, compare the cost of spreading the income across multiple years.

- But check the tax brackets too. Avoiding IRMAA while creating a larger federal tax bill is not exactly a win.

Use Qualified Charitable Distributions When Eligible

- A QCD can satisfy part or all of an RMD while keeping the qualifying distribution out of AGI.

- That can be more valuable than taking the distribution, writing a check to charity, and claiming an itemized deduction you may not even use.

Use Roth and HSA Money Strategically

- Qualified Roth distributions and qualified HSA withdrawals generally do not increase AGI.

- That gives retirees something incredibly useful: control.

- You can fund a large expense without automatically stacking more taxable income into the same year.

Harvest Losses Against Capital Gains

- Capital losses can offset capital gains under the tax rules.

- That may reduce the net gain reaching AGI. Read my tax-loss harvesting and IRMAA guide before assuming the gross gain is the final number.

Appeal When the Rules Actually Allow It

- IRMAA is not appealable merely because the bill feels unfair.

- But a qualifying life-changing event or corrected tax information may support a new determination or reconsideration.

- Use the right process for the right problem. Throwing Form SSA-44 at every situation is not a strategy.

▶ My complete guide to avoiding or reducing IRMAA walks through the planning options in more detail.

What This Tool Cannot Know

The checker is designed to be useful without pretending it can see your entire tax return.

It cannot automatically know:

- Your cost basis

- Your IRA basis from nondeductible contributions

- Your exact taxable Social Security amount

- Your annuity exclusion ratio

- Your home-sale basis and exclusions

- Suspended passive losses

- Whether a settlement is taxable

- What the IRS or Social Security will ultimately accept

Where the answer depends on one of those facts, the tool says so.

That is better than fake precision.

Best way to use the detailed estimate?

Use the taxable amount expected to appear on your tax return, not the cash received. If you are unsure, check the relevant tax form or ask your tax professional before treating the estimate as final.

IRMAA Income Checker FAQs

What income is included in IRMAA MAGI?

IRMAA MAGI generally starts with adjusted gross income and adds tax-exempt interest. That means taxable wages, retirement distributions, pensions, interest, dividends, capital gains, business income, rental income, taxable Social Security, and other income included in AGI can affect IRMAA. Municipal bond interest is added back even when it is federally tax-exempt.

Do IRA withdrawals count toward IRMAA?

Yes. The taxable portion of a traditional IRA withdrawal generally increases AGI and counts toward IRMAA MAGI. If the IRA contains nondeductible contributions, part of the distribution may be a nontaxable return of basis. A qualifying QCD may also be excluded from AGI.

Do Roth IRA withdrawals affect IRMAA?

Qualified Roth IRA distributions generally do not increase AGI or IRMAA MAGI. A nonqualified distribution may contain taxable earnings. Roth conversions are different and generally increase income to the extent converted amounts have not already been taxed.

Do capital gains affect Medicare premiums?

Yes. Net taxable capital gains are included in AGI and can affect IRMAA. The amount that matters is the taxable gain after basis, losses, exclusions, and other adjustments. It is not automatically the total sale proceeds.

Does municipal bond interest count toward IRMAA?

Yes. Tax-exempt interest is added to AGI when IRMAA MAGI is calculated. Municipal bond interest may be federally tax-free and still increase the income Medicare uses for IRMAA.

Does Social Security count toward IRMAA?

The taxable portion of Social Security benefits enters AGI and can affect IRMAA. The nontaxable portion does not. The taxable amount depends on filing status and other income.

Does selling a house trigger IRMAA?

It can. The full sale price does not count. Any taxable capital gain remaining after basis, selling expenses, improvements, exclusions, and other applicable rules may increase AGI and affect IRMAA.

Do inheritances count toward IRMAA?

Receiving cash or property as an inheritance generally does not create income by itself. Income later produced by inherited assets, inherited retirement-account distributions, and taxable gains from selling inherited property can affect IRMAA.

Which tax year does Medicare use for IRMAA?

Social Security generally uses tax-return information from two years before the Medicare premium year. For example, 2026 IRMAA is generally based on 2024 tax information.

Can one dollar really trigger IRMAA?

Yes. IRMAA uses income thresholds. Crossing a threshold by a small amount can place you in a higher premium tier for that year. That does not mean every extra dollar always creates a surcharge. It means the dollar that crosses the threshold can be expensive.

Is this an official Social Security calculator?

No. This is an educational planning tool. Social Security makes the actual IRMAA determination using IRS tax information and applicable Medicare rules.

Build the Right MAGI Number Before You Plan Around It

IRMAA planning starts with the right income number.

- Not gross cash flow.

- Not whatever number happened to be easiest to find.

- Not a guess based on what feels taxable.

Start with AGI. Add tax-exempt interest. Understand which proposed transactions change that result.

Then look at the threshold.

That order matters.

Because avoiding IRMAA based on the wrong MAGI number is not planning. It is just guessing with a calculator.

Your next step?

▶ Run the IRMAA Income checker with the income sources you are concerned about. If a result says “it depends,” answer the short follow-up questions. Then use the linked guide for the one issue that actually needs a deeper look.

Official sources: The tool’s premium amounts and thresholds are based on published Medicare data from CMS. The MAGI formula and two-year lookback follow Social Security guidance. Rules and thresholds change, so confirm current figures before completing a major transaction.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.