Medicare open enrollment IRMAA planning starts now—the deadline is December 7th, 2026.It’s that time of year again. Your mailbox is full of Medicare Advantage flyers, and you have until December 7th to pick your Medicare Advantage plan for 2026. But here is the trap most retirees fall into:

They think once they pick a plan, they are done

Here is the bottom line: The Open Enrollment Period (AEP) only locks in your insurance carrier. It does not lock in your premium cost.

Your final premium for 2026 is actually determined by your income (MAGI) from 2024. Learn more about IRMAA income brackets here. Learn more about how Part B is calculated here. (Use my IRMAA Checklist here) But for your future premiums (2027 and beyond), the clock is ticking right now. You have a second, hidden deadline, December 31st, to manage your income and avoid the dreaded IRMAA surcharge. Understanding Medicare’s surcharge implications can significantly impact your budget, ensuring you aren’t caught off guard.

If you ignore this second deadline, you might save $20 a month on a drug plan only to get hit with a $2,000 surcharge from Social Security.

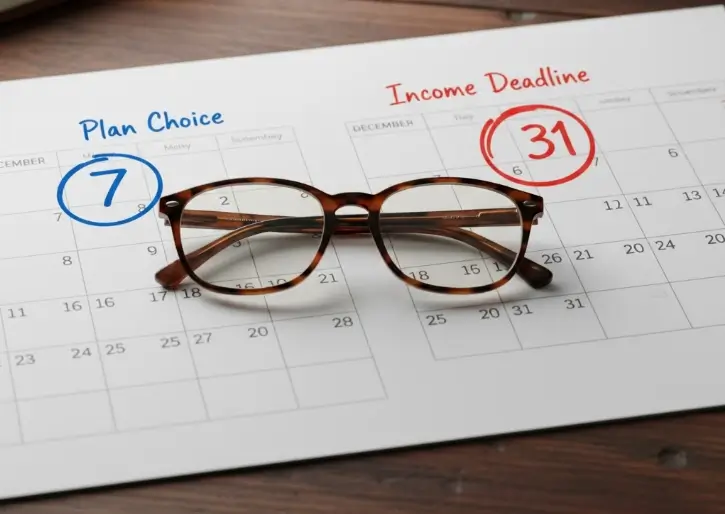

⚡ The Two-Deadline Strategy

- Deadline 1 (Dec 7): You must select your Medicare Advantage or Part D plan for 2026. This determines your base premium.

- Deadline 2 (Dec 31): You must finalize your 2025 taxable income. This determines your IRMAA surcharge for 2027.

- The “Base + Surcharge” Rule: Your total cost is the plan premium plus the IRMAA surcharge. A “cheap” plan can still be expensive if you are in Tier 3.

- The Action: Use the checklist below to align your plan choice with your income strategy.

Key Takeaways Ahead

The “Base + Surcharge” Medicare Advantage Trap

Many retirees use the Medicare Advantage Plan Finder, sort by “Lowest Premium,” and enroll in a $0 or $15/month plan. They feel like they won.

Then, in January, they get a bill from Medicare for $500+ a month. Why?

Medicare Plan Finder only shows the Base Premium. It does not include your personal IRMAA Surcharge.

- Part B Surcharge: Added to your standard $202.90 premium.

- Part D Surcharge: Added to whatever drug plan you choose.

🧮 Real Cost Calculator

If you are a Tier 1 single filer with a $0 Medicare Advantage plan, your bill isn’t zero. It looks like this:

- Part B Base: $202.90

- Part B IRMAA (Tier 1): +$81.20

- Part D Plan: $0.00

- Part D IRMAA (Tier 1): +$14.50

- Your REAL Monthly Cost: $298.60

💡 Stop overpaying for retirement.

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Avoid hidden fees like IRMAA

- → Lower your taxes legally

- → Protect your nest egg

Use this timeline to ensure you don’t miss a critical window.

The end of the year is a critical time for managing your health care costs and taxes. The following timeline outlines key deadlines for Medicare’s Annual Enrollment Period (AEP) and strategic financial actions to avoid future IRMAA surcharges. Paying attention to these dates can save you significantly on premiums and ensure your plan continues to meet your needs for 2026 and beyond.| Dates | Action Item | Why It Matters |

|---|---|---|

| Oct 1 – Oct 15 | Review ANOC Letter | Check if your current plan is dropping your doctors or drugs. This is your “early warning.” |

| Oct 15 – Dec 7 | Compare Plans | Shop for 2026 coverage. Pro Tip: Check if your drugs moved to a higher tier. |

| Nov 15 – Dec 31 | Project 2025 MAGI | Estimate your total income for this year. This sets your IRMAA for 2027. |

| Before Dec 31 | Execute “Income Defense” | Harvest losses, do QCDs, or defer income to stay under an IRMAA cliff. |

Case Study: The “December Surprise”

Let’s look at a real scenario involving a couple, “Jim and Sarah.”

The Setup:

- Date: December 6th.

- Action: Jim and Sarah enroll in a new Part D plan with a $40/month premium. They are happy.

- Income Status: Their projected 2025 MAGI is $215,000 (just under the $218,000 Tier 1 cliff).

The Failure:

- Date: December 20th.

- Event: Their mutual fund pays out a large year-end capital gain distribution of $5,000.

- Result: Their MAGI jumps to $220,000. They cross the cliff.

The Consequence:

Because they didn’t check their income after open enrollment ended, they enter 2027 in Tier 2.

- Part B Surcharge: ~$2,448/year (for the couple).

- Part D Surcharge: ~$700/year (for the couple).

- Total Loss: Over $3,100 in avoidable premiums.

The Lesson: Open Enrollment ends Dec 7, but IRMAA Enrollment effectively ends Dec 31. You must monitor your income until the ball drops on New Year’s Eve. Feel free to use my IRMAA Calculator to assist. Use my IRMAA Checklist to help …

Defensive Move: The “December Distribution Watchlist”

Action Step: Log into your fund provider’s website in November. Search for “Estimated Capital Gains Distributions.” If a big payout is coming and you are near an IRMAA cliff, consider selling the fund before the record date to avoid the phantom income.

💡 Stop overpaying for retirement.

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Avoid hidden fees like IRMAA

- → Lower your taxes legally

- → Protect your nest egg

Frequent Reader Questions About AEP & IRMAA

📚 Deepen Your IRMAA Defense

Don’t let surcharges eat your retirement. Check out these guides:

- 2026 IRMAA Brackets & Surcharges – See the exact income thresholds for next year.

- Capital Gains Spiking Your IRMAA? Use Tax-Loss Harvesting – How to lower your MAGI before Dec 31.

- IRMAA Appeal Guide (Form SSA-44) – What to do if you already crossed the line due to a life event.

Does changing my plan affect my IRMAA?

No. Changing your insurance carrier (e.g., switching from Humana to UnitedHealthcare) has zero impact on your IRMAA tier. Your tier is determined solely by your income reported to the IRS. However, your total cost changes because the IRMAA surcharge is added on top of your new plan’s premium.

If I retire this year, will I still pay IRMAA?

Possibly, because Social Security looks at your income from two years ago (when you were working). However, retirement is a “Life-Changing Event.” You can file Form SSA-44 to request an immediate reduction in your premiums based on your new, lower retirement income. You do not have to wait two years.

Can I pay my IRMAA directly to the plan?

No. IRMAA surcharges are paid directly to Medicare, usually deducted from your Social Security check. You pay your plan premium to the insurance company, and your surcharge to the government. They are separate bills.

What is the IRMAA income threshold for 2026?

For 2026, the IRMAA thresholds are: Individual filers start paying surcharges at $109,000 Modified Adjusted Gross Income (MAGI), and married couples filing jointly at $194,000. However, these thresholds increase throughout the year with eight different income tier brackets. If your income exceeds the highest tier ($500,000+ for individuals), you could pay up to $560/month in additional Part B premiums alone.

Conclusion: Finish the Drill

Most retirees sprint to the December 7th deadline and then stop. That is a mistake.

The period between December 7th and December 31st is the “Red Zone” for tax planning. This is your final window to harvest losses, make charitable donations, or defer income to keep your MAGI in check.

Your Next Steps:

- Finalize Plan Choice: Pick your 2026 Part D/Advantage plan by Dec 7.

- Check YTD Income: Log into your brokerage account and check your Year-to-Date realized gains.

- Look for Dividends: Check for upcoming mutual fund distributions.

- Execute Offsets: If you are near a cliff, use Tax-Loss Harvesting before Dec 31.

For a clearer picture of your overall retirement health, use our IRMAA Calculator to project your potential surcharges. See the 5-step plan Jane used to erase her $2,400 Medicare surcharge.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.