You think you’re being responsible by working past 65 and maxing out your Health Savings Account (HSA). A strategy often favored by financially savvy individuals like yourself. The IRS thinks you’re breaking the law.

There is a hidden tripwire in the Medicare enrollment process that catches my smartest clients every year. It’s called the Medicare HSA 6-Month Rule or Lookback. In my experience working with hundreds of high-net-worth retirees, this Medicare/HSA coordination failure is the #1 unexpected tax penalty I see for clients approaching Medicare age.

If you apply for Medicare after age 65, the government automatically backdates your Part A coverage by up to six months. While “retroactive coverage” sounds like a bonus, it is actually a tax grenade. It retroactively disqualifies you from contributing to your HSA for those months. Turning your legal contributions into “excess contributions” subject to immediate taxes and penalties.

Unlike generic advice to “just stop contributing,” we will dive into the precise mechanics that turn your responsible savings into an IRS penalty, and exactly how to fix it. I’ve seen retirees forced to unwind thousands of dollars in savings (and pay a 6% excise tax) because they missed this one deadline.

Here is the math on the trap, the story of how “Efficient Eric” lost money by saving it, and the exact date you must stop contributing to stay safe.

⚡ Key Takeaways

- The Rule: Medicare Part A coverage is mandatory and retroactive for up to 6 months if you enroll after age 65.

- The Consequence: You cannot contribute to an HSA for any month you have Medicare coverage (even retroactive coverage).

- The Penalty: Contributions made during the lookback period are “excess,” subject to income tax + a 6% cumulative excise tax.

- The Fix: You must stop all HSA contributions (including your employer’s) 7 months before you apply for Medicare or Social Security.

Key Takeaways Ahead

How the Trap Works: The “Retroactive” Disqualification

The problem isn’t Medicare itself; it’s the timeline.

To legally contribute to a Health Savings Account, the IRS requires you to be an “eligible individual”. A specific status defined by having a high-deductible health plan and no other health coverage (including Medicare). The moment you are covered by Medicare, even retroactively, you immediately lose your status as an eligible individual for HSA contributions for that month.

Here’s the detail most people miss: Enrollment date ≠ Application date.

If you sign up for Medicare (or Social Security) at age 66, 67, or later, the Social Security Administration (SSA) automatically backdates your Part A coverage start date by six months (but no earlier than your 65th birthday).

You cannot decline this retroactive coverage. It is statutory. This nuance often goes overlooked because the SSA and IRS rarely cross-reference their public guidance on this specific interaction.

Important Distinction: Part A vs. Part B/D

While this article focuses on the often-automatic and retroactive nature of Medicare Part A enrollment (the primary trigger for HSA disqualification) it’s important to distinguish it from Medicare Parts B and Medicare Part D. Many individuals choose to delay Part B and D enrollment if they continue working and have qualifying employer health coverage, often without penalty.

However, remember that Part A enrollment is often triggered automatically upon applying for Social Security benefits past age 65, and cannot typically be declined retroactively. This distinction is crucial as you plan your retirement healthcare strategy .

Case Study: The “Efficient Eric” Disaster

Let me tell you about a client I’ll call Eric. My experience, built over nearly 3 decades of direct client guidance, confirms this is a pervasive and often misunderstood issue.

In 2026, Eric is 68 years old and planning to retire in June. Being financially efficient, he fully funded his HSA in January ($5,400 including the catch-up contribution) to get the tax deduction upfront.

- June 1: Eric retires and applies for Social Security & Medicare.

- The Lookback: Because he was over 65, Medicare backdated his Part A coverage 6 months. To December 1st of the previous year.

- The Result: Eric was retroactively enrolled in Medicare for all of 2026.

- The Penalty: His HSA contribution limit for 2026 dropped to $0. His entire $5,400 deposit became an “excess contribution.”

Eric had to scramble to remove the funds, pay income tax on the earnings, and refile paperwork.

If he hadn’t caught it, he would have owed a 6% penalty every single year the money stayed in the account.

💡 Michael Ryan Money Tip

If you are still working and have employer coverage, you may be able to delay Medicare Part A if your employer has more than 20 employees. However, once you apply for Social Security benefits, Part A becomes mandatory and the 6-month lookback clock starts ticking immediately.

💡 STOP THE 6% IRS PENALTY

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Avoid hidden Medicare & HSA tax traps

- → Get the exact “Safe Stop” dates you need

- → Protect your retirement savings from IRS clawbacks

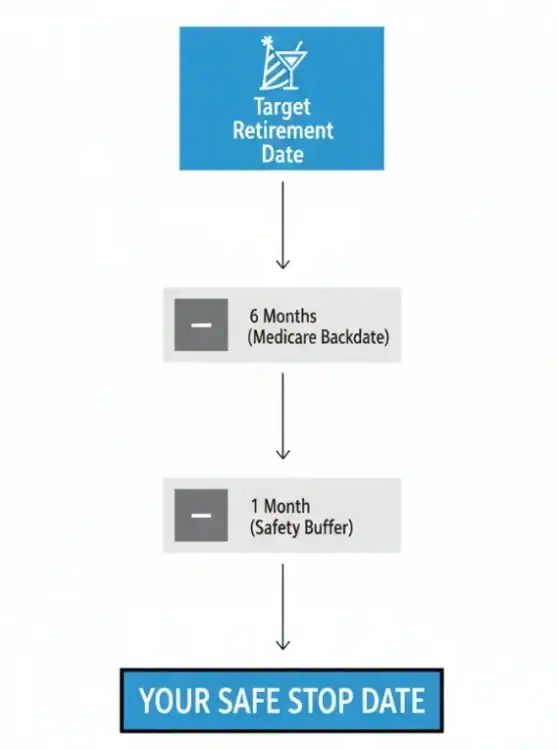

The Math: Calculating Your “Safe Stop Date”

You need to perform a specific calculation to determine your personal stop date. Do not guess.

The Formula

- Determine your Target Retirement/Application Date. (e.g., September 2026).

- Subtract 6 Months. (March 2026).

- Subtract 1 More Month (The Safety Buffer). (February 2026).

Why the Safety Buffer is Critical: Understanding the “Last Month Rule”

Why the buffer? This crucial extra month protects you from the IRS’s “Last Month Rule” (outlined in IRS Pub 969). This states that if you are not an HSA-eligible individual on December 1st (the first day of the last month of your tax year), you cannot contribute to an HSA for any month of that entire year under the full-contribution rule.

Given that Medicare Part A can backdate up to six months, this buffer helps ensure your eligibility remains intact through the prior year-end.

HSA contribution limits are calculated on a monthly pro-rata basis; if you are covered by Medicare for even one day in a month, you are ineligible for that entire month.

Real Numbers Example

- You apply for Medicare: October 15, 2026.

- Coverage backdates to: April 1, 2026.

- Ineligible Months: April through December (9 months).

- Eligible Months: January through March (3 months).

- Your Limit: You can only contribute 3/12ths of the annual max.

- Your Safe Stop Date: You should have stopped contributing on March 1st.

🚀 The Michael Ryan Money “Safe Stop” Checklist

Before you make your next HSA deposit, check these three boxes:

- [ ] Are you over 65? If yes, the 6-month lookback applies to you.

- [ ] Are you applying for Social Security soon? Remember, applying for Social Security automatically triggers Part A enrollment. You cannot separate them.

- [ ] Is your employer contributing? Their contributions count toward your limit. You must tell HR to stop the “free money” 6 months early too.

The “Double-Dip” Penalty: It’s Not Just Your Money

This is the unspoken truth that catches employees off guard: Your employer’s contributions count against you.

If your company puts $1,000 into your HSA as a perk, and you trigger the 6-month lookback, that $1,000 is considered an excess contribution by you.

The IRS Logic (IRS Notice 2008-59):

- Employer contributions are excluded from your gross income.

- If you weren’t eligible for the HSA, that exclusion is invalid.

- You must withdraw the $1,000 and pay income tax on it.

💡 STOP THE 6% IRS PENALTY

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Avoid hidden Medicare & HSA tax traps

- → Get the exact “Safe Stop” dates you need

- → Protect your retirement savings from IRS clawbacks

How to Fix It (If You’re Already in the Trap)

If you are reading this and realizing you’ve already over-contributed, don’t panic. But you must act fast.

The “Removal of Excess” Protocol

You cannot just withdraw the money and spend it. That counts as a non-qualified distribution (20% penalty). You must follow a specific IRS procedure.

- Contact your HSA Custodian.

- Tell them you have an “Excess Contribution.” Do not say “withdrawal.”

- Request a “Return of Excess Contribution.”

- Your HSA Custodian will then accurately calculate the original excess contribution amount and any Net Income Attributable (NIA) to it. NIA refers to the specific gains or losses associated with the excess funds. It’s critical that both the excess contribution and the NIA are removed. Your custodian will handle these complex calculations, but understanding the term ensures you’re following the precise IRS procedure.

- Receive the Check.

- The custodian will send you the money.

- Report it on Taxes.

- The contribution amount is added back to your “Other Income” (Line 8z on Schedule 1).

- The earnings are reported as investment income.

Deadline: You must do this before the tax filing deadline (April 15) of the following year to avoid the 6% excise tax.

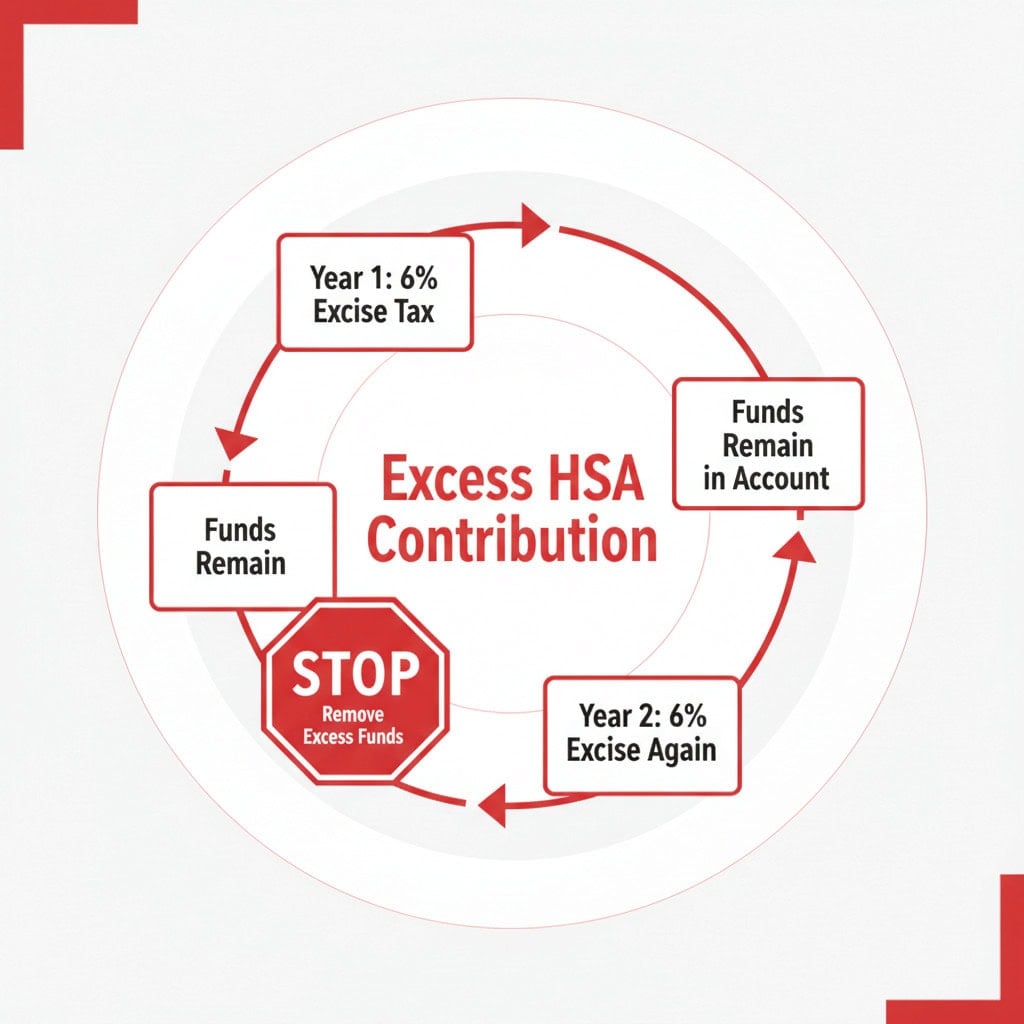

⚠️ Myth Busted: “I’ll just pay the penalty.”

Some people think the 6% penalty is a one-time fee. It is not. The 6% excise tax (Form 5329) repeats every single year that the excess money remains in the account. It is a cumulative bleed on your wealth. You must remove the funds immediately to stop the 6% penalty from compounding year after year.

📚 Further Reading & Resources

- Using Your HSA for Retirement: Learn how to maximize this account before you hit the Medicare cutoff.

- IRMAA & Medicare Planning: High income can also trigger higher Medicare premiums. See how to plan for it.

- Comprehensive Retirement Planning: A broader look at how Medicare fits into your full financial picture.

The Bottom Line on the 6-Month Rule

Medicare Part A is often called “free,” but for the diligent saver, it carries a hidden price tag. The retroactive coverage rule is a coordination failure between the tax code and the healthcare system, and you are the one paying for it.

If you are working past 65:

Stop HSA contributions 6-7 months before your target retirement date .

If you are applying for Social Security:

Understand that this triggers Part A immediately and retroactively. Stop your HSA first.

If you already messed up:

File a “Return of Excess” request immediately. The paperwork hassle is better than the perpetual 6% IRS fine.

Communicating with HR

When communicating with your HR or benefits department, be specific. Clearly state that you are making this request due to upcoming Medicare enrollment and the Medicare HSA 6-Month Lookback Rule affecting HSA eligibility.

Document your request in writing (email is ideal) to create a paper trail, ensuring all contributions (both yours and the company’s) cease by your calculated Safe Stop Date. This proactive communication can prevent missteps and protect you from unnecessary penalties.

By taking these steps, you can confidently navigate this complex intersection, ensuring your diligent savings remain exactly that: savings, not penalties.

Your Next Steps

- Check your pay stub. Is your HSA deduction still active?

- Calculate your “Safe Stop Date” using the formula above.

- Download Form 8889. Review Part VII to understand how the penalty is calculated if you don’t fix it. Download Form 8889 from IRS.gov .

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.