As a financial planner for over 25 years, I’ve seen more household budgets broken by health insurance premiums than by any other expense. It’s a pain point I know well. You feel trapped between paying a staggering monthly bill and the terrifying risk of being uninsured in an emergency.

With the American Rescue Plan Act (ARPA) subsidy extensions set to expire at the end of 2025, many families are facing potential premium hikes of 75% or more in 2026. A recent KFF poll found that nearly three-quarters of adults are worried about affording unexpected medical bills.

But here’s the good news: you have more control than you think.

This guide is my professional playbook. We’ll go beyond the basics to give you a step-by-step guide to navigating the Health Insurance Marketplace, maximizing any available tax credits, and leveraging advanced strategies like the Health Savings Account (HSA) to turn your healthcare costs into a wealth-building machine.

Key Takeaways: Your 2026 Health Insurance Strategy

- Master the Marketplace:

The #1 way to save money on health insurance premiums is by using the HealthCare.gov Marketplace to access potential premium tax credits (subsidies), especially before key provisions expire in 2026. - Choose Structure Over Premium:

Don’t just pick the lowest premium. A High-Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA) can offer significant long-term savings for healthy individuals. - Unlock the HSA Superpower:

An HSA provides a triple tax advantage (tax-deductible contributions, tax-free growth, tax-free withdrawals) and can be used as a powerful tool for both medical expenses and retirement. - Don’t Go It Alone:

Using a licensed health insurance broker costs you nothing and can help you find plans and discounts you might otherwise miss. - Myth Bust for Savings:

Believing common myths, like “HSAs are use-it-or-lose-it”, can cost you thousands. Proactive planning is essential.

Key Takeaways Ahead

1. The #1 Way to Save Money on Health insurance Premiums: Understanding ACA Marketplace Subsidies

For anyone who doesn’t get insurance through an employer (freelancers, gig workers, early retirees) the Affordable Care Act (ACA) Marketplace is your starting point. Its most powerful feature is the premium tax credit, commonly known as a subsidy.

A subsidy is money from the government to help lower your monthly premiums. It’s not just for low-income individuals; thanks to the extended provisions of the American Rescue Plan Act, millions of middle-income families now qualify.

How do you qualify for ACA subsidies in 2026?

ACA subsidy eligibility is based on your estimated Modified Adjusted Gross Income (MAGI) and household size for the coverage year. You can get an estimate of your potential savings by using the official tools on your state’s marketplace or the federal site.

💡 Michael Ryan’s Tip

Don’t assume you earn too much to qualify. The current rules cap the amount anyone has to pay for a benchmark plan at 8.5% of their household income through 2025. This means a family with a six-figure income can still receive significant subsidies if their insurance costs are high.

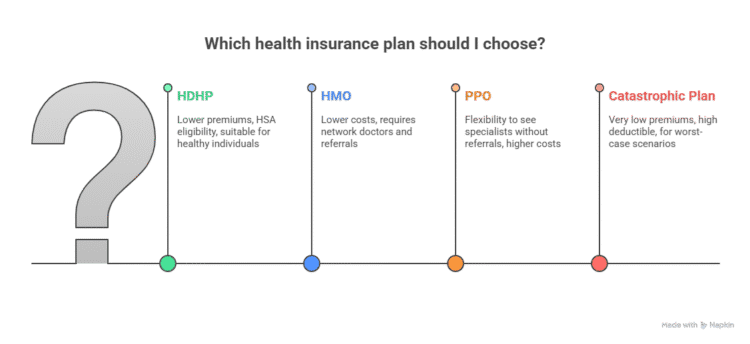

2. Smart Healthcare Plan Selection: Choosing a Structure That Fits Your Life

Once you’re on the ACA Marketplace, you’ll see plans categorized by “metal levels” (Bronze, Silver, Gold, Platinum) and network types. Choosing the right structure is key to saving money.

High-Deductible Health Plan (HDHP):

These plans have lower monthly premiums but higher deductibles. They are an excellent choice for individuals who are generally healthy. The real power of an HDHP is that it makes you eligible for a Health Savings Account (HSA).

HMO (Health Maintenance Organization):

HMOs typically have lower premiums and out-of-pocket costs but require you to use a specific network of doctors and get referrals from a primary care physician.

PPO (Preferred Provider Organization):

PPOs offer more flexibility to see specialists without a referral and to go out-of-network (at a higher cost).

Catastrophic Health insurance Plan:

If you are under 30 or have a hardship exemption, you can buy a catastrophic plan. It has a very low premium but an extremely high deductible, designed to protect you from worst-case scenarios, not for routine care.

3. The HSA Superpower: The Ultimate Medical 401(k)

If you choose an HDHP, you unlock access to a Health Savings Account (HSA). In my 25 years as a planner, I believe the HSA is the single most powerful but misunderstood account in personal finance. For a deeper dive, check out my full guide on using an HSA as a stealth retirement account.

An HSA offers a unique triple tax advantage:

- Tax-Deductible Contributions: The money you put in is pre-tax, lowering your taxable income for the year.

- Tax-Free Growth: The funds can be invested and grow completely tax-free.

- Tax-Free Withdrawals: You can take money out tax-free at any time to pay for qualified medical expenses.

For 2026, you can contribute up to the IRS-specified limits to your HSA. These funds never expire and are yours to keep, even if you change jobs or insurance plans.

⚠️ Myth Busted

“HSAs are ‘use-it-or-lose-it’ accounts.”

This is false and a common confusion with Flexible Spending Accounts (FSAs). HSA funds roll over indefinitely. Many of my clients use their HSA as a stealth retirement account, paying for current medical costs out-of-pocket and letting their HSA balance grow for decades.

4. Other Proven Tactics for Lowering Your Healthcare Costs

Beyond plan selection, use these insider strategies to chip away at your total healthcare spending.

- Work with an Insurance Broker:

A licensed health insurance broker can be an invaluable resource. They can help you navigate the maze of plans and find options you might miss. - Take Advantage of Wellness Incentives:

Many employers offer wellness credits or incentives for healthy behaviors, which can directly reduce your premiums. - Use Prescription Discount Programs:

Never pay the sticker price for medication. Apps like GoodRx can find coupons and discounts that are often cheaper than your insurance copay. - Explore ICHRAs with Your Employer:

If you work for a small business, ask about an Individual Coverage Health Reimbursement Arrangement (ICHRA). This is a newer type of employer benefit where the company gives you tax-free money to buy your own individual marketplace plan.

5. Common Health Insurance Myths & Costly Pitfalls to Avoid

⚠️ Myth #1: “The lowest premium plan is always the cheapest.”

This is a dangerous trap. A low-premium Bronze plan might have a $9,400 deductible. If you have a significant medical event, you could be on the hook for that full amount. It is crucial to analyze the out-of-pocket maximum (the absolute most you would have to pay in a year) not just the premium.

⚠️ Myth #2: “I’m too old for an HSA.”

As long as you are enrolled in an HSA-eligible HDHP and are not yet enrolled in Medicare, you can contribute to an HSA. In fact, if you are 55 or older, you can contribute an extra $1,000 “catch-up” contribution each year. After you enroll in Medicare at 65, you can use your accumulated HSA funds tax-free to pay for Medicare premiums.

⚠️ Myth #3: “I can’t negotiate my medical bills.”

Always ask for an itemized bill after a hospital stay to check for errors. Many hospitals also offer prompt-pay discounts for those who can pay in cash or have financial assistance programs for those who qualify. It never hurts to ask.

Get Smarter About Your Health & Wealth

Join thousands of readers who receive my weekly, no-fluff tips on insurance, retirement, and tax strategies that actually save you money. No spam, just actionable financial wisdom.

Continue Learning: Build Your Financial Fortress

- Deepen your knowledge on HSAs – Learn how this powerful account can become a cornerstone of your retirement savings.

- Create your complete financial plan – Integrate your health insurance strategy into a bigger picture for long-term wealth.

- Master your monthly budget – Use the money you save on premiums to accelerate your financial goals with the best budgeting tools.

Conclusion: Take Control of Your Healthcare Costs

Navigating health insurance in 2026 will be challenging, but you now have the key to unlocking affordable coverage. By understanding subsidies, strategically selecting your health insurance plan, and leveraging powerful tools like the HSA, you can take control of your healthcare costs.

The power is in your hands to make informed decisions that protect both your health and your financial future.

Now, try searching for: HSA retirement strategy, disability insurance, best budgeting apps.

About the Author Michael Ryan is a former financial planner and the creator of MichaelRyanMoney.com. For over 25 years, he has specialized in helping families navigate complex financial challenges, from federal student aid and retirement planning to mastering the art of personal finance.