If you’re reading this in 2026, your Medicare premiums for the year are already determined by your 2024 income—in fact, the Social Security Administration finalized your IRMAA brackets in early 2026 using your 2024 Modified Adjusted Gross Income (MAGI). Same with Part D too. And if you experienced any significant income changes in 2024, you may not have known the full impact at the time. Many people turn to online forums for insights, leading to frequent discussions about common concerns like the top IRMAA questions from reddit.

The Income-Related Monthly Adjustment Amount (IRMAA) is one of the most frustrating, counterintuitive traps in retirement tax planning. It’s not based on what you earn today. It’s based on what you earned two years ago. That means the tax decisions you make in 2024; every Roth conversion, every capital gain, every IRA withdrawal will determine whether you pay the standard Medicare premium or get hit with surcharges that can exceed $6,936 per year in 2026. Stay a step ahead with my IRMAA Checklist here Your capital gains may impact your IRMAA penalty too.

Most retirees discover this the hard way: a single large income event (selling a rental property, taking a big RMD, or executing a poorly-timed Roth conversion) triggers a notice from the Social Security Administration 18-24 months later. By then, the damage is done, and there’s almost nothing you can do to reverse it.

The good news? Once you understand the forensic mechanics of how IRMAA is calculated. And more importantly, when it’s calculated. You can legally engineer your income to stay below the thresholds. This isn’t about gaming the system. It’s about understanding the two-year lookback rule and planning accordingly. All to avoid having to file an IRMAA appeal.

In this guide, I’ll walk you through:

- The exact MAGI formula the Social Security Administration uses (it’s simpler than you think, but critical to get right)

- Which income sources count toward IRMAA, and which powerful exceptions you can exploit (like QCDs and Roth withdrawals)

- The official 2026 IRMAA brackets (based on 2024 MAGI) and how to model your own tax-cliff risk using our free calculator here:

- The SSA’s behind-the-scenes process when they pull your data, when they send notices, and the only four “life-changing events” that qualify for an appeal

This isn’t theory. This is the same forensic IRMAA playbook I used with clients for almost 3 decades to save them tens of thousands in avoidable Medicare surcharges. Let’s get started.

💡 Get Smarter About IRMAA Planning

Receive one clear, actionable money move each week—designed to help you:

- Sidestep costly Medicare surcharges & tax traps

- Master the two-year lookback rule before it’s too late

- Apply proven retirement tax strategies in minutes

✅ Join thousands of readers already protecting their premiums.

📬 No spam. Unsubscribe anytime.

Key Takeaways Ahead

The 2026 IRMAA Lookback: The True Date That Determines Your Premiums

The first and most frustrating lesson I teach clients about the Income-Related Monthly Adjustment Amount (IRMAA) is that the government is looking at your past, not your present. The IRMAA determination for your 2026 Medicare premiums (Parts B and D) is based entirely on your 2024 tax return.

The two-year lookback period is like trying to drive while looking in the rearview mirror: the money decisions you made in 2024 are the ones steering your premium costs in 2026. This time lag is why the IRMAA Medicare surcharge blindsides so many people. Especially when NUA is involved with IRMAA.

Insight From Michael Ryan: I’ve seen clients like Sandra, who had a one-time income spike in 2024 (large capital gain from selling a rental property). When her SSA notice arrived in late 2025, she was shocked. Her income was back to normal, but that single event from 2 years ago meant she was penalized for the entirety of 2026. This two-year lookback trap requires planning now.

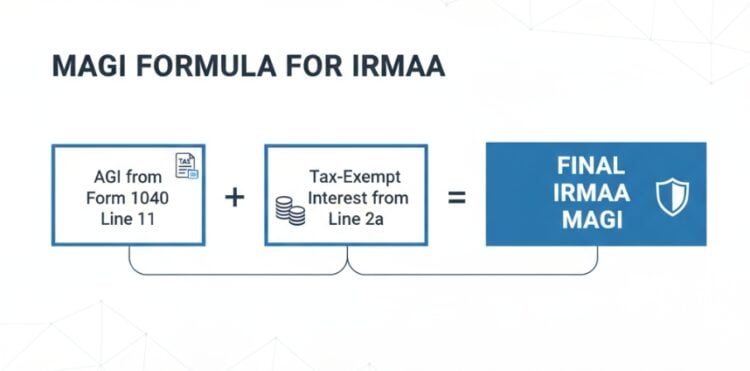

Forensic Breakdown: How to Calculate Your 2024 MAGI for 2026 IRMAA

The key factor behind your IRMAA calculation is one number: your Modified Adjusted Gross Income (MAGI). The Social Security Administration uses a specific, precise formula to calculate it that is different from the MAGI used for other things (like ACA subsidies).

The MAGI Formula Decoded: Your Actionable Plan

Your 2024 MAGI for 2026 IRMAA is:

- Adjusted Gross Income (AGI):

- From Line 11 of your 2024 Form 1040

- PLUS: Tax-Exempt Interest:

- From Line 2a of your 2024 Form 1040

- The Sum = Your Final IRMAA MAGI.

This forensic, line-by-line method is the official, verifiable formula directly sourced from the Social Security Administration’s Program Operations Manual System (POMS HI 01101.010).

Michael Ryan Insight : You might wonder why tax-exempt interest (like that from municipal bonds) is added back when it’s otherwise tax-free. It’s the ‘Nice Try‘ Clause. Congress knew high-earning retirees would park millions in municipal bonds to duck the tax. Adding it back into the IRMAA calculation prevents this high-income tax avoidance.

If you want to run your own scenarios to check your MAGI against the official 2026 IRMAA thresholds (based on 2024 MAGI), use our calculator below.

IRMAA Bracket Calculator for 2026

2026 IRMAA Calculator

Estimate your Medicare Part B & D premiums based on your 2024 income

Total Annual IRMAA Cost

(Part B + Part D surcharges × 12 months)

Understanding Your Results

- Two-Year Lookback: Your 2026 premiums are based on your 2024 income (the two-year lookback rule)

- MAGI Formula: AGI (Line 11) + Tax-Exempt Interest (Line 2a) = IRMAA MAGI

- Cliff Effect: Going $1 over a threshold triggers the full surcharge for that tier

- Appeals: You can appeal using Form SSA-44 only if you had a qualifying life-changing event

- Planning Tip: Use strategies like Qualified Charitable Distributions (QCDs) or phased Roth conversions to manage MAGI

What Counts and What Doesn’t: The Income Source Matrix

Knowing the precise IRMAA MAGI calculation is useless if you don’t know what income is included in your starting AGI. The three most common IRMAA triggers are Capital Gains, RMDs, and unmanaged Roth Conversions.

| Income Source | Counts Toward IRMAA? | Planner’s Note |

|---|---|---|

| Wages, Salary, Tips | YES | Fully taxable and included in AGI. |

| Taxable Interest & Dividends | YES | Includes bond interest and stock dividends. |

| Tax-Exempt Interest | YES | Added back into AGI (Form 1040, Line 2a). |

| Capital Gains | YES | Both short-term and long-term gains count fully. |

| Roth Conversions | YES | Taxable in the year of conversion; affects IRMAA 2 years later. |

| Standard IRA/401(k) RMDs | YES | Required distributions are taxable income. |

| Roth IRA Withdrawals | NO | Qualified distributions are tax-free and IRMAA-free. |

| QCDs (Charitable) | NO | Bypasses AGI entirely, protecting you from the cliff. |

- Use my free RMD Calculator here.

Strategic Tip: Timing Your Roth Conversions for the IRMAA Lookback

This tax-free status is why advanced retirement tax planning frequently centers on Roth conversion timing. Not to reduce current tax, but to legally mitigate future IRMAA penalties. Remember, the conversion itself counts as taxable income in the year you do it (e.g., converting in 2025 affects your 2027 IRMAA).

The primary goal of the savvy pre-retiree (like Planning Paul) should be to run MAGI projections to forecast the ‘empty‘ years where income is low (e.g., after retiring but before RMDs start). This is the window to execute a series of phased Roth conversions, taking the tax hit early to keep your MAGI below the IRMAA thresholds later on.

This is a powerful retirement tax planning strategy.

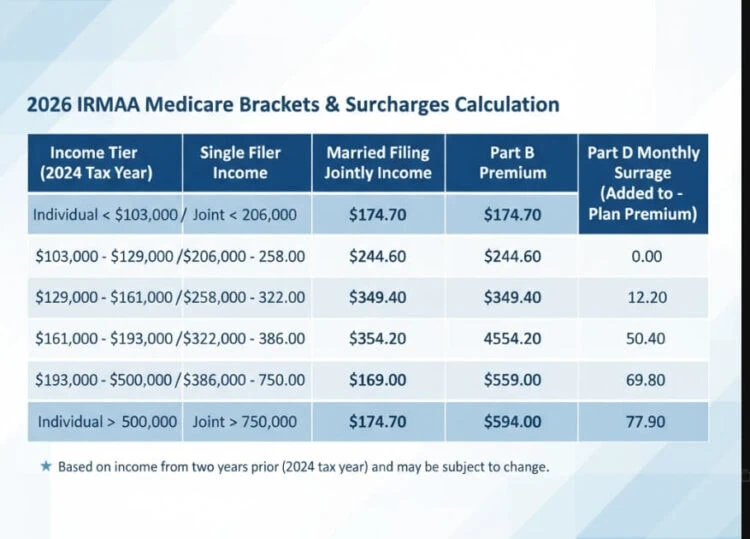

Avoiding the Tax Cliff: 2026 IRMAA Brackets & Thresholds (Based on 2024 MAGI)

Here’s where Medicare planning strategies pay off. The system is designed with steep IRMAA thresholds, the tax cliff effect. Going just one dollar over a threshold forces you to pay the full surcharge for the entire tier.

Technique: “The true cost of a single dollar of income is not 50 cents in tax, but potentially $800+ in Medicare penalties.”

The 2026 IRMAA brackets (based on 2024 MAGI) were officially announced by CMS in November 2025. The standard Medicare Part B premium for 2026 is $202.90 per month. The first IRMAA tier begins at $109,000 (Single) or $218,000 (Joint), with surcharges ranging from $81.20 up to $487.00 (Part B) and $14.50 to $91.00 (Part D) per month for the highest income earners.

(Note: The 2026 IRMAA brackets are official and were published by CMS on November 14, 2025, based on 2024 MAGI data. These figures are final for 2026 coverage.)

| 2024 MAGI (Single) | 2024 MAGI (Joint) | Total Part B Premium | Part D Surcharge |

|---|---|---|---|

| ≤ $109,000 | ≤ $218,000 | $202.90 | +$0.00 |

| $109,001 – $137,000 | $218,001 – $274,000 | $284.10 | +$14.50 |

| $137,001 – $171,000 | $274,001 – $342,000 | $405.80 | +$37.50 |

| $171,001 – $205,000 | $342,001 – $410,000 | $527.50 | +$60.40 |

| $205,001 – $500,000 | $410,001 – $750,000 | $649.30 | +$83.40 |

| > $500,000 | > $750,000 | $689.90 | +$91.00 |

*Part B totals include the $202.90 base premium plus the applicable IRMAA surcharge.

Proactive Planning: Use Our 2026 IRMAA MAGI Calculator to Model Your Tax-Cliff Risk Now (Free Tool).

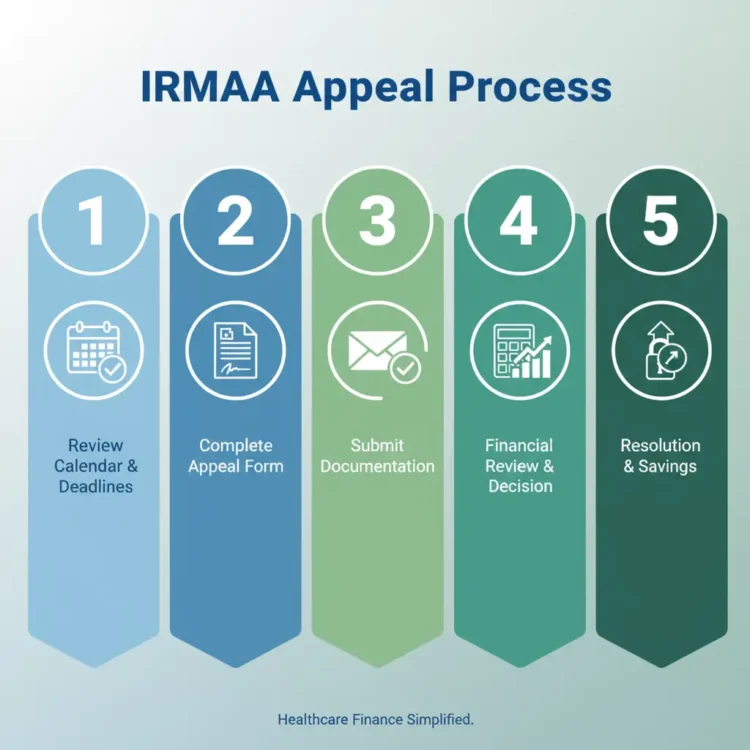

The Behind-the-Scenes: How the SSA Operates & When to Appeal

Many of the questions revolve around one thing: “When do I get the bad news?” Here is the operational process the Social Security Administration (SSA) uses to determine your IRMAA.

- Data Exchange (November 2025):

- The SSA electronically requests your Modified Adjusted Gross Income data from the IRS (specifically, your 2024 return).

- Predetermination Notice (Late 2025):

- If your MAGI exceeds a threshold, the SSA sends you an Initial IRMAA determination notice, often in November or December.

- Final Determination (January 2026):

- After allowing for time to review or appeal, the final IRMAA amount is set and the higher premium is reflected in your statement or Social Security withholding.

The 4 Qualifying ‘Life-Changing Events’ for Appeal (Form SSA-44)

Can you appeal an IRMAA determination? Yes, but only for very specific reasons. Planning Paul needs to know that simply retiring or having your income drop is not enough. You must have a Life-Changing Event that caused the drop.

- Work Stoppage: You or your spouse stopped working or reduced work hours.

- Loss of Income: Loss of Income from an Income-Producing Asset or Pension.

- Marital Changes: Marriage, divorce, annulment, or death of a spouse.

- Property Change: Loss of income-producing property due to a casualty loss or sale.

Could You Qualify for an IRMAA Appeal?

See if you're eligible to reduce your Medicare premiums with our free interactive tool

This is the cold truth about appeals: a one-time spike from a large, isolated capital gain (like selling your primary home for a gain that exceeds the exclusion) will likely not qualify for an appeal. Why? Because it wasn’t a “Life-Changing Event.” You must tie the drop in income to one of the four categories on Form SSA-44.

For the official rules on Form SSA-44 and the appeals process, always check the source.

Frequent Reader Questions (FAQ)

Does Social Security count as income for IRMAA?

No, your full Social Security benefits are not counted. Only the taxable portion of your Social Security (which is determined by a separate calculation on Form 1040) is included in your AGI and thus contributes to your IRMAA MAGI.

What is the income limit for Medicare tax in 2026?

For 2026, the first IRMAA bracket begins when 2024 MAGI is above $109,000 for single filers and above $218,000 for married couples filing jointly. These are the official thresholds published by CMS in November 2025.

What is the difference between AGI and MAGI for Medicare?

AGI (Adjusted Gross Income, Form 1040 Line 11) is your starting point. MAGI (Modified Adjusted Gross Income) is AGI plus any tax-exempt interest (Form 1040 Line 2a).

When does the SSA send IRMAA notices?

The SSA typically sends the initial IRMAA determination notice, which is based on the data exchange with the IRS, in November or December of the year before the premiums are set (e.g., late 2025 for 2026 premiums).

Master Your Retirement Tax Strategy

- How to time Roth conversions to avoid IRMAA penalties – Use the two-year lookback to convert tax-free in low-income windows.

Planner’s Bottom Line

The most common trap in retirement planning isn’t market volatility; it’s falling victim to a poorly managed Medicare & tax lookback. Learn how you can avoid the IRMAA trap with some planning. You have the power to decide your IRMAA, but the decision must be made two years in advance.

Don’t simply track your MAGI. Actively manage it below the cliff using strategies like phased Roth conversions. Get ahead of the two-year rule, and you’ll keep thousands of dollars in your pocket.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.