Have questions on Medicare costs? Wondering about IRMAA Brackets and surcharges for your Medicare Parts B & D? We’re going to unpack the hidden expense that catches thousands of Medicare beneficiaries off guard every year. Along with my IRMAA Checklist.

A surcharge that’s being determined by financial decisions you made back in 2024. These surcharges can significantly increase your premium costs, creating financial strain during retirement. Therefore, understanding Medicaid IRMAA impacts is crucial.

Picture this: You’ve just opened your 2026 Medicare statement, ready for another routine monthly premium. But instead of the expected $206.50, you’re staring at a bill for over $700. Your heart races. In 2024, one retiree thought selling a second home wouldn’t matter. Her Part B surcharge could jump ~$1,400.

What happened? Thousands of Medicare beneficiaries experience this same shock every year, blindsided by a surcharge they never saw coming.

The culprit? IRMAA, the Income-Related Monthly Adjustment Amount. And here’s the thing. The income decision that triggered this 2026 surcharge? You made it back in 2024, long before you ever thought about Medicare costs.

Welcome to the Medicare “time machine” where your financial past directly determines your healthcare future. What you can do is understand the rules, plan strategically, and potentially appeal if life threw you a curveball.

I’ll walk you through everything you need to know about IRMAA brackets and surcharges for Medicare Parts B and D, including the 2026 thresholds based on your 2024 income, common income triggers, and your safety net if circumstances have changed. Let’s get through this hidden Medicare expense together.

💡 Quick Takeaway: The IRMAA Cliff

Your 2024 income determines your 2026 Medicare Part B and Part D premiums. Exceeding an IRMAA bracket threshold by just $1 can push you into a higher tier, costing you over $900 per person annually in extra premiums.

TL;DR Summary of Medicare IRMAA Brackets & Surcharges

- Problem:

- Most Medicare recipients don’t realize their 2024 income directly determines their 2026 premiums. And crossing an IRMAA threshold by just $1 can increase your full calculated annual surcharge over $900 extra per year.

- Answer:

- Understanding IRMAA’s two-year lookback system and knowing the exact 2026 thresholds ($109,000 single/$218,000 married) allows strategic income management to avoid costly surcharges before they hit.

- Insight:

- While most income spikes (like Roth conversions and property sales) don’t qualify for appeals, eight specific life-changing events (including retirement, marriage, divorce, and death of a spouse) create an appeal pathway using Form SSA-44 to reduce premiums based on current lower income.

Key Takeaways Ahead

The IRMAA Problem: Why 2024 Income Determines 2026 Medicare Costs

That jaw dropping figure on your 2026 Medicare statement? It’s likely the IRMAA surcharge, a stealthy addition to your Part B and Part D premiums. We know this can feel overwhelming; here’s the step-by-step path to understanding the delayed income cycle.

This unexpected cost isn’t based on your current earnings, but on your Modified Adjusted Gross Income (MAGI) from your 2024 federal tax return. It’s a financial ‘IRMAA time machine‘ that often leaves retirees wondering, ‘What just happened to my budget?‘ This 2 year lookback mechanism catches thousands off guard annually.

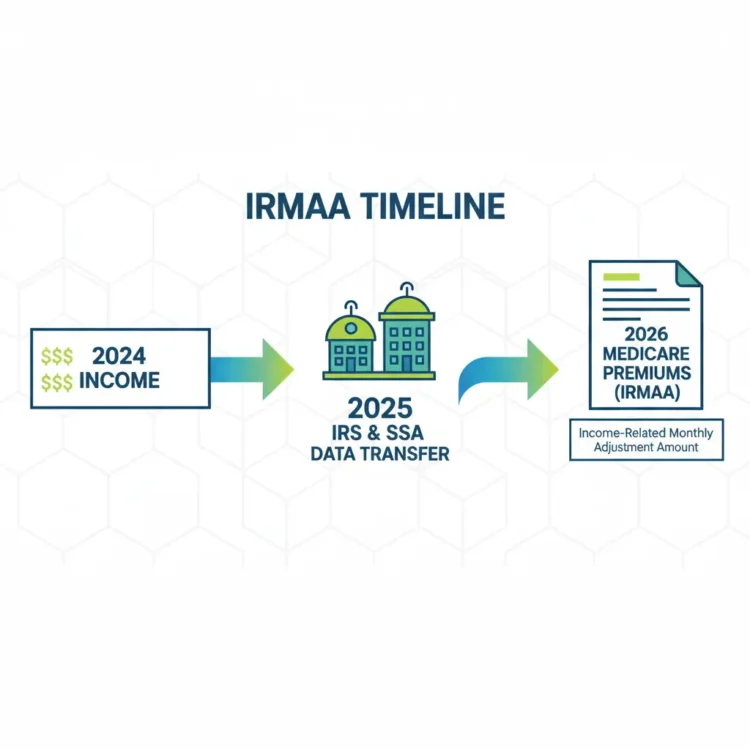

The 2-Year Lookback Rule: Your IRMAA Time Machine

The 2-year look back rule creates a delayed connection between your income and your Medicare costs. As you can see in the attached infographic, here is the three-step IRMAA timeline:

- Step 1 (2024):

- Back in 2024, your income was reported on your tax return, filed with the IRS in early 2025.

- Step 2 (2025):

- By late 2025, the IRS shared that 2024 MAGI data with the Social Security Administration (SSA).

- Step 3 (2026):

- Fast forward to 2026: the SSA uses that two-year-old income data to set your current Medicare Part B and Part D premiums. This is the year you’re actually paying the higher costs.

I met with a retired teacher recently who will learn this the hard way. A small bonus in 2024 led to an extra $1,200 annually on his 2026 Medicare bill. This is a delayed financial consequence that demands proactive strategies, a concept often missing in simpler explanations. Don’t let your financial past surprise your healthcare future.

🔍 Explained Simply: Your IRMAA Time Machine

The IRMAA system forces you to plan two years ahead. Your income reported on your 2024 taxes (filed in 2025) directly dictates your Medicare Part B and D costs for 2026. This disconnect is why proactive financial planning around retirement is absolutely critical. In this context, implementing effective tax strategies can make a significant difference in managing your healthcare costs. For instance, employing taxloss harvesting strategies explained can help you optimize your taxable income, potentially reducing your IRMAA tier and associated costs.

How to Understand What is MAGI for IRMAA?

Your Modified Adjusted Gross Income (MAGI) isn’t just your AGI. It’s your Adjusted Gross Income (AGI) from line 11 of your tax return, plus certain typically non-taxable deductions like tax-exempt interest from municipal bonds. This distinction is crucial, yet often overlooked.

💡 Michael Ryan Money Tip: Calculating Your MAGI for IRMAA

To pinpoint your exact MAGI for IRMAA purposes, start with your Adjusted Gross Income (AGI) from line 11 of your 2024 federal tax return. Then, add back any tax-exempt interest (e.g., from municipal bonds). That final number is what the SSA will use.

Example: If your AGI was $95,000 and you had $5,000 in tax-exempt bond interest, your MAGI for IRMAA is $100,000. But missing that $5,000 can cost you!

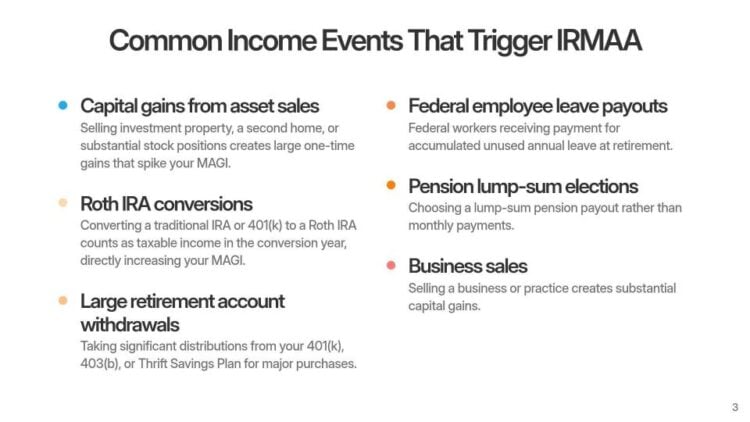

Common Income Events That Trigger IRMAA

What types of financial moves accidentally push retirees over IRMAA thresholds?

- Business sales: Selling a business or practice creates substantial capital gains.

- Capital gains from asset sales: Selling investment property, a second home, or substantial stock positions creates large one-time gains that spike your MAGI.

- Roth IRA conversions: Converting a traditional IRA or 401(k) to a Roth IRA counts as taxable income in the conversion year, directly increasing your MAGI.

- Large retirement account withdrawals: Taking significant distributions from your 401(k), 403(b), or Thrift Savings Plan for major purchases can unexpectedly push you into a higher bracket.

- Federal employee leave payouts: Federal workers receiving payment for accumulated unused annual leave at retirement can see a substantial, unexpected MAGI increase in that retirement year.

- Pension lump-sum elections: Choosing a lump-sum federal pension payout rather than monthly payments concentrates taxable income, making IRMAA a very real risk.

Watch this quick YouTube video I put together that summarizes this article. Just press play:

⚠️ Myth Busted: “Only the Rich Pay IRMAA”

Many believe IRMAA only impacts the “super-rich.” This is a dangerous myth! Even middle-income retirees can trigger IRMAA with a one-time income spike like a Roth conversion or selling a rental property. Crossing a threshold by just $1 makes you pay the full surcharge.

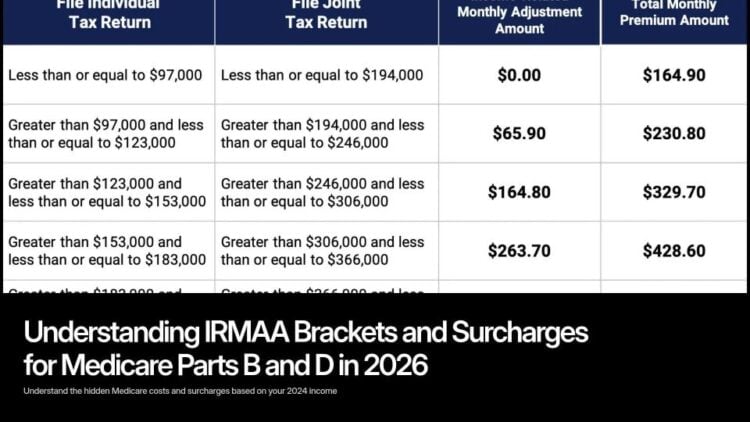

2026 IRMAA Brackets and Medicare Part B Premiums

The 2026 standard Medicare Part B premium is $202.90 per month, and the standard Part B deductible is $283.00. This baseline applies to beneficiaries below the first IRMAA threshold.

High-income beneficiaries pay this standard premium plus an IRMAA surcharge. And that goes for Part D Drug coverage too. The highest bracket reaches approximately $702 per month total, based on 2024 MAGI.

| Bracket | Single Filer MAGI (2024) | Total Monthly Part B Premium (2026) | Part B Surcharge | Monthly Part D IRMAA (2026) |

|---|---|---|---|---|

| 1 (Standard) | ≤ $109,000 | $202.90 | $0.00 | $0.00 |

| 2 | $109,001 – $137,000 | $284.10 | $81.20 | $14.50 |

| 3 | $137,001 – $171,000 | $405.80 | $202.90 | $37.50 |

| 4 | $171,001 – $205,000 | $527.50 | $324.60 | $60.40 |

| 5 | $205,001 – < $500,000 | $649.20 | $446.30 | $83.30 |

| 6 (Highest) | ≥ $500,001 | $689.90 | $487.00 | $91.00 |

*Source: CMS 2026 Fact Sheet & SSA POMS IRMAA Tables

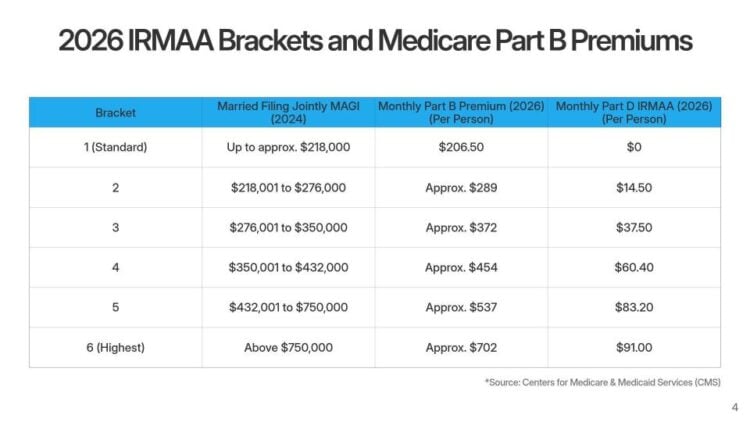

It’s important to understand the ‘cliff effect’ with IRMAA brackets. If your MAGI goes over a threshold by even $1, you are subject to the full surcharge for that higher bracket for the entire year. There is no partial surcharge within a bracket.

2026 IRMAA Brackets and Surcharge Amounts (Based on 2024 MAGI)

The income-related monthly adjustment amount IRMAA brackets 2026 operate on a progressive scale with six income brackets. The table below shows the thresholds and costs for married couples filing jointly.

| Bracket | Married Filing Jointly MAGI (2024) | Total Monthly Part B Premium (2026) | Part B Surcharge | Monthly Part D IRMAA (2026) |

|---|---|---|---|---|

| 1 | $218,000 or less | $202.90 (CMS) | $0.00 | $0.00 (SSA) |

| 2 | $218,001 – $274,000 | $284.10 (CMS) | $81.20 | $14.50 (SSA) |

| 3 | $274,001 – $342,000 | $405.80 (CMS) | $202.90 | $37.50 (SSA) |

| 4 | $342,001 – $410,000 | $527.50 (CMS) | $324.60 | $60.40 (SSA) |

| 5 | $410,001 – $750,000 | $649.20 (CMS) | $446.30 | $83.30 (SSA) |

| 6 | $750,001+ | $689.90 (CMS) | $487.00 | $91.00 (SSA) |

💡 Get Smarter About Medicare Costs

Receive one clear, actionable money move each week—designed to help you:

- Sidestep costly tax traps & penalties

- Save thousands in Medicare IRMAA surcharges

- Apply proven retirement planning strategies in minutes

✅ Join thousands of readers already protecting their wealth.

📬 No spam. Unsubscribe anytime.

The Life-Changing Event Appeal: Your Safety Net

Direct Answer: If your income has dropped significantly since 2024 due to a major life event, you can file a Life-Changing Event Appeal using Form SSA-44 with the Social Security Administration (SSA) to request that your 2026 Medicare premiums be based on your new, lower current income.

What if circumstances beyond your control have reduced your income since 2024? Are you stuck paying higher premiums based on income you’re no longer earning? Fortunately, no. The Social Security Administration provides a critical safety valve called the life-changing event appeal.

Qualifying Life-Changing Events

The Centers for Medicare and Medicaid Services recognizes several major life events that can significantly reduce your income:

- Work stoppage or reduction: Retirement from your primary job, being laid off, or reducing work hours.

- Marriage: Getting married can change your income situation, potentially impacting your joint MAGI.

- Divorce or annulment: Separation of assets and income streams drastically alters individual MAGI.

- Death of spouse: Loss of a spouse’s income often reduces household MAGI.

- Loss of income-producing property: Loss due to disaster, bankruptcy, or other circumstances beyond your control.

- Loss of pension income: Cessation of pension payments through no fault of your own.

- Employer settlement payment: Certain one-time employer settlement payments that affected a prior year’s income may be appealed if they are truly non-recurring.

The tool you need for this process is Form SSA-44, officially titled “Medicare Income-Related Monthly Adjustment Amount – Life-Changing Event.”

🛠️ How to File Your Appeal: Don’t Pay More Than You Owe!

Filing the appeal correctly is essential to get your premium reduced quickly. You’ll need specific documentation to prove your life-changing event and reduced income. Get our Step-by-Step Guide on Filing Form SSA-44 and Required Documentation.

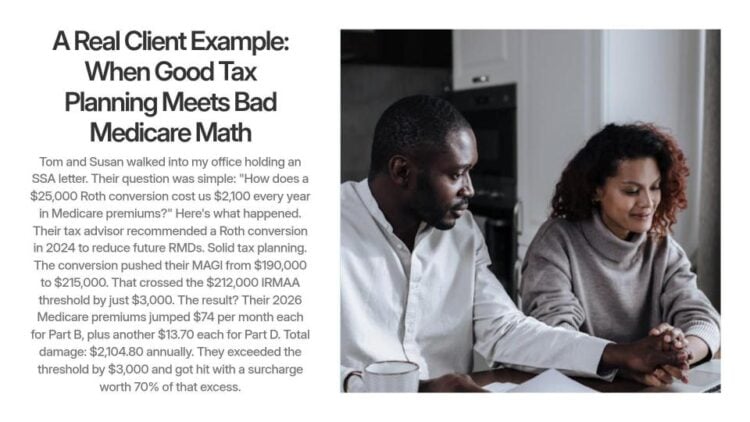

A Real Client Example: When Good Tax Planning Meets Bad Medicare Math

Tom and Susan walked into my office holding an SSA letter. Their question was simple: “How does a $25,000 Roth conversion cost us $2,296.80 every year in Medicare premiums?”

Client Story: Tom & Susan’s $2,296.80 IRMAA Mistake

Here’s what happened. Their tax advisor recommended a Roth conversion in 2024 to reduce future RMDs. The conversion pushed their MAGI from $190,000 to $221,000. That crossed the crucial $218,000 IRMAA threshold by just $3,000.

The result? Their 2026 Medicare premiums jump $81.20 per month each for Part B, plus another $14.50 each for Part D. Total damage: $2,296.80 annually. They exceeded the threshold by $3,000 and got hit with surcharges worth the full amount for that higher bracket.

Here’s the thing: if they’d split that conversion into two years ($12,500 in 2024 and $12,500 in 2025, or better yet, carefully managed 2024 and 2025 conversions) they’d have stayed under the threshold both years and paid zero IRMAA. Same long-term tax benefit, $2,100 less in annual Medicare costs.

💰 Avoid Tom & Susan’s $2,100 Mistake

Get weekly strategies that coordinate your tax moves with Medicare costs:

- Learn exactly when to time Roth conversions

- Understand how capital gains trigger IRMAA surcharges

- Use proven income-smoothing playbooks

✅ Join thousands of readers making smarter retirement decisions.

📬 No spam. Unsubscribe anytime.

Final Thoughts: Taking Control of Your Medicare Costs

The two-year IRMAA look-back can feel like a trap, a delayed consequence that catches you off guard. But reframe it as a two-year planning window, and you gain tremendous control over your Medicare Part B and Part D premiums.

Your 2024 income is now history, setting your 2026 Medicare costs. This means your primary action for 2026 is determining if you qualify for the life-changing event appeal. But remember, your 2025 income, which you’re earning and reporting right now, determines your 2027 premiums.

- Avoid the Roth-to-IRMAA Trap How conversion income spikes Medicare premiums two years later.

- Navigate RMDs Without Triggering IRMAA Strategic withdrawal planning that keeps you below premium brackets.

- Choose the Right Health Insurance Plan Complete guide to understanding HMOs, PPOs, and ACA marketplace options.

🚀 Your Next Steps: Immediate Action Plan

- Locate Your 2024 Tax Return: Find your AGI (Line 11) and check for tax-exempt interest to calculate your MAGI.

- Compare to 2026 Brackets: Cross-reference your 2024 MAGI with the table above to see your potential 2026 IRMAA bracket.

- Assess Life-Changing Events: Did you retire, get divorced, or lose a spouse since 2024? You might qualify for a “life-changing event appeal“.

- Plan for 2025: Strategize income management now to avoid 2027 IRMAA surcharges.

- Consult an Expert: Connect with a financial advisor specializing in Medicare and retirement taxes.

The real question is whether you’ll be surprised by IRMAA or whether you’ll plan for it proactively.

Feel free to use my Medicare IRMAA Surcharge Calculator as well.

Share this guide with a friend turning 65!

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.