As a financial planner for nearly 30 years, I’ve seen more families stressed out by the FAFSA website than by the stock market. You’ve spent hours gathering tax documents and personal information. Only to be stopped by a confusing financial aid form that feels more like a roadblock to college than a gateway.

Take a deep breath. If you’re feeling overwhelmed, you’re not alone. The launch of the (alleged) Better FAFSA for the 2025-26 academic year has been plagued by significant technical issues. It actually led to a 9% drop in first-time submissions. Families are getting stuck in login loops, hitting parent contributor walls, and struggling to find clear answers.

After all, I’m a dad too. My youngest son is still in college, so I can realte to all your frustration.

This guide is the exact playbook I’ve used to get my clients unstuck. We’re going to skip the confusing government jargon and give you a simple, linear checklist. From the documents you need to gather today to the ‘submit’ button. And explain the critical changes you need to know to get it right.

Key Takeaways Ahead

What is the FAFSA, and Why Is It So Crucial?

The Free Application for Federal Student Aid (FAFSA) is the single most important form you will fill out to get help paying for college. It is the official application used by the U.S. Department of Education to determine your eligibility for more than $150 billion in federal student aid.

Think of FAFSA as the master key that unlocks the door to:

- Grants: Free money you don’t have to pay back, like the Federal Pell Grant.

- Work-Study Programs: Part-time jobs to help you earn money for education expenses.

- Federal Student Loans: Low-interest loans from the government.

- State & Institutional Aid: Most states and colleges also use your FAFSA information to award their own grants and scholarships.

💡 Michael Ryan Money Tip

Even if you think your family’s income is too high to qualify for need-based aid, you should still file the FAFSA. Many colleges require it for merit-based scholarships, and all students who file are eligible for Direct Unsubsidized Federal Loans, which are often a better option than private student loans.

The BIG Change for 2025-26: The FAFSA Simplification Act

If you’ve heard stories from older siblings or friends, be aware: the FAFSA has changed significantly. Thanks to the FAFSA Simplification Act, the old formula, known as the Expected Family Contribution (EFC), has been replaced.

The new system uses the Student Aid Index (SAI).

What is the Student Aid Index (SAI)?

The SAI is a number calculated from your FAFSA that determines your eligibility for aid. Unlike the EFC, the SAI can be a negative number (as low as -1,500), which helps financial aid officers better identify students with the highest need. A lower SAI generally means more eligibility for financial aid.

Who Can Apply for FAFSA?

Eligibility for Title IV federal student aid is broad, but there are some key requirements. You must:

- Be a U.S. citizen or an eligible noncitizen.

- Have a valid Social Security number (with some exceptions).

- Be enrolled or accepted for enrollment in an eligible degree or certificate program.

- Maintain satisfactory academic progress in college.

🔍 For Non-U.S. Citizens

Eligibility can be complex. This includes DACA recipients and students from certain Pacific Islands. For detailed criteria, consult the official Federal Student Aid eligibility page. For families needing language assistance, the FAFSA form is available in Spanish, and help is available in multiple languages through the FSAIC hotline.

Your FAFSA Pre-Flight Checklist: Gather These Documents First

From my experience, the biggest source of stress is starting the form unprepared. Before you even go to the website, gather these items.

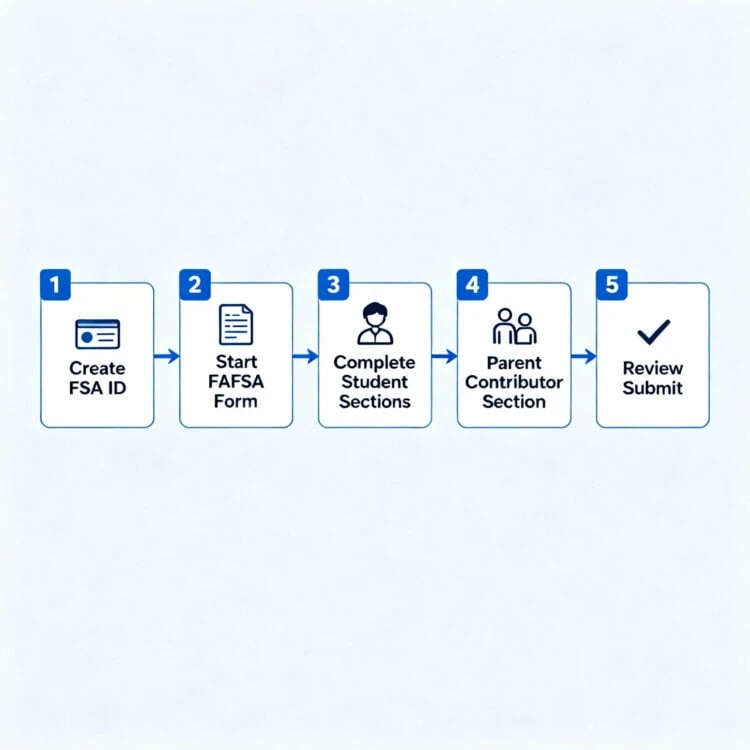

How to Fill Out the FAFSA: Michaeal Ryan Money 5-Step Guide

Step 1: Create Your FSA ID (The Mandatory First Step)

Before you can even touch the FAFSA form, both the student and at least one parent contributor need to create their own FSA ID at StudentAid.gov. This is your electronic signature and account login.

- Crucial: You must use separate, unique email addresses for the student and parent accounts. Mixing these up is a primary cause of FSA ID login problems.

- Troubleshooting: If your account gets locked or you have 2-step verification not sending, use the official FSA ID account recovery portal immediately.

Step 2: Start the FAFSA Form

Go to the official U.S. government website: StudentAid.gov. Do not use any other site, as they may charge unnecessary fees.

Step 3: Complete the Student Sections

The form will ask for the student’s demographic and financial information. This part is generally straightforward.

Step 4: Invite and Complete the Parent Contributor Section

This is the most common failure point for the 2025-26 FAFSA.

- The student will invite a parent to be a “contributor” using the parent’s name, DOB, SSN, and email address.

- Common Error: The parent contributor invitation not received error is often caused by a simple SSN/DOB mismatch. The data entered by the student must match the parent’s FSA ID profile exactly.

- The parent will then receive an email, log in with their own FSA ID, and provide their financial information.

Step 5: Review, Sign, and Submit

Both student and parent(s) must electronically sign the application using their individual FSA IDs. A missing signature is a common signature error workaround can’t fix—you must log back in and sign.

⚠️ Loan Default Traps for Re-Filers

For adult learners like Elena who may have had previous student loans, the FAFSA system cross-references against loan default records. If you have a loan in default, it can trigger an error and block new aid. Before re-filing, check your status on StudentAid.gov and resolve any defaults through rehabilitation or consolidation.

What Happens After You Submit the FAFSA?

- Confirmation: You’ll receive a confirmation page and email almost immediately.

- Processing: The Federal Student Aid processing center systems will process your application in 1-3 days.

- Student Aid Report (SAR): You will receive a Student Aid Report (SAR), which is a summary of your FAFSA information and your calculated Student Aid Index (SAI). Review this carefully for any errors. If you find one, you’ll need to enter the FAFSA correction window to fix it. A common issue is Reject Code 68, which indicates a potential duplicate application that needs resolution.

- Colleges Receive Your Info: The schools you listed will receive your Institutional Student Information Record (ISIR) and use it to create your financial aid award package.

Common FAFSA Myths vs. Reality

Frequently Asked Questions (FAQ) About FAFSA

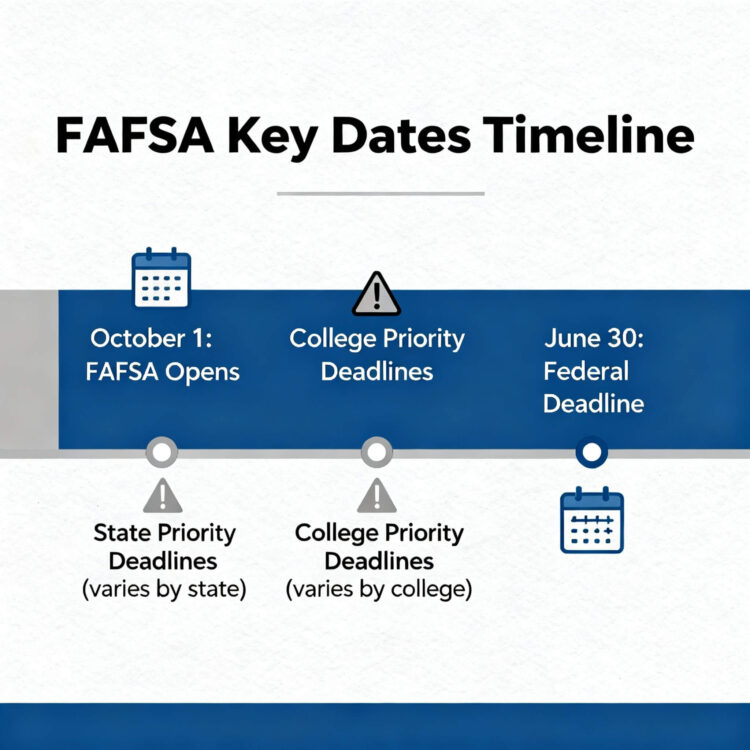

What if I miss the FAFSA deadline?

You can still file the federal FAFSA, which makes you eligible for Pell Grants and federal loans. However, you may have missed out on state and institutional aid that had earlier priority deadlines.

Do I have to repay FAFSA money?

It depends. Grants and scholarships are free money that you do not repay. Work-study funds are earned through a job. Federal student loans must be repaid with interest.

What if my family’s financial situation has changed since we filed taxes?

This is considered a FAFSA special circumstance. After you submit the FAFSA with the required tax information, contact each college’s financial aid office directly to request a “professional judgment review.” You will need to provide documentation of the change (e.g., layoff notice, medical bills).

Now, try searching for: FAFSA deadlines, common FAFSA mistakes, Student Aid Report.

📚 Continue To Master Your Financial Aid Journey

- What to do if you miss the FAFSA deadline – Learn the critical steps to take and what aid you might still be eligible for.

- Build a strong foundation with the best finance books for college students – Equip yourself or your student with the essential money skills for college and beyond.

- Go beyond FAFSA with our guide to basic financial planning – Create a complete financial roadmap to turn educational goals into reality.

Conclusion: Your First Investment in Your Education

Completing the FAFSA is your first major investment in your education. It’s not just a form; it’s a proactive step toward making your college dreams affordable. By following this guide, you’ve taken control of the process, armed yourself with the right information, and opened the door to billions of dollars in financial aid. You’ve got this!

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.