Receiving an inheritance is one of life’s most profound and challenging moments. You’re navigating grief while suddenly facing complex financial decisions that feel monumental.

As a financial planner for almost 3 decades, I’ve sat at many kitchen tables with families in this exact position. The most common feeling? Overwhelmed.

And the biggest risk? Making a rash decision driven by emotion.

The most important first step is to take a breath and do nothing rash. I’ve seen firsthand how the pressure to “do something” can lead to irreversible mistakes. For my client Jill, as she sorted through her mom’s papers amid tears, the best advice I gave her was to create a 90-day shield. A period where no major decisions are made.

With over $18 trillion in wealth expected to be transferred between generations by 2032, you are not alone in this journey.

Now, this isn’t just another article with generic advice. This is my professional playbook. A step-by-step guide to help you get through the first year. To help you understand the complex tax rules.

And build a long-term plan that turns this financial windfall into lasting generational wealth.

Key Takeaways Ahead

Part 1: The First 90 Days After You Receive an Inheritance – The “Do Nothing… Smartly” Phase

The period immediately following a loss of a loved one is not the time for major financial moves. Your only job is to stabilize the situation, gather information, and protect the assets.

To help you stay organized, I’ve created a downloadable Inheritance Timeline Checklist. It breaks down these crucial first steps into a manageable to-do list. Subscribe at the end of this article for instant access.

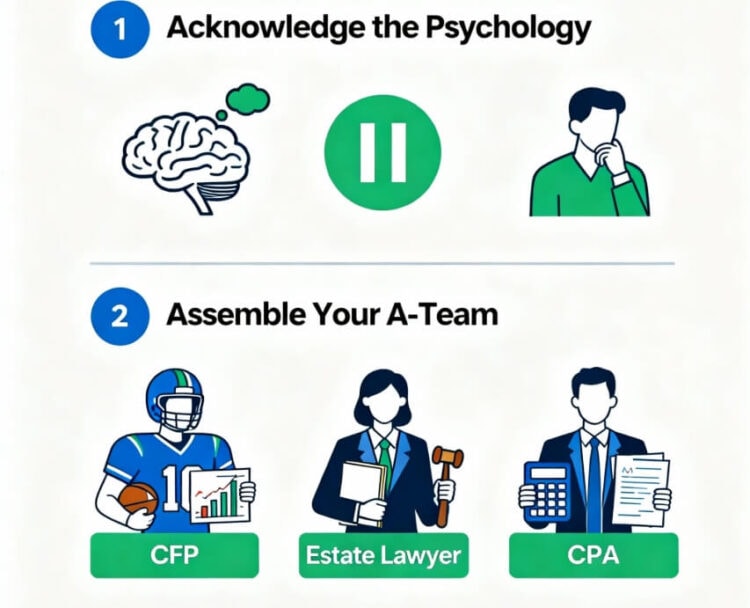

Step 1: Acknowledge the Psychology of a Financial Windfall

Sudden wealth can trigger a complex mix of emotions: guilt, anxiety, and even “impostor syndrome.” It’s totally normal to feel this wealth shock.

Resisting the urge to immediately buy a house, quit your job, or make dramatic investments is your first and most important act of wealth preservation. We understand the guilt. Pause honors their sacrifice.

Step 2: Assemble Your “A-Team”

You cannot and should not do this alone. You need a team of fiduciaries. Professionals legally obligated to act in your best interest.

- Certified Financial Planner (CFP®): Your quarterback. A CFP® will help you create a holistic financial roadmap.

- Estate Lawyer: To help you navigate the legal process, understand the will or living trust, and handle the probate court system if necessary.

- Certified Public Accountant (CPA): Your tax expert. A tax advisor is critical for minimizing taxes and handling the estate’s final tax returns.

Real-Life Example:

A recent story on X highlighted a family who lost nearly six figures to a scammer posing as an “inheritance consultant.” Can you imagine how horrible you must be, to take advantage of people who just lost a loved one?

Like this fraud victim, protect yourself by working only with credentialed fiduciaries.

Step 3: Understand the Immediate Legal Process

Your estate lawyer will guide you, but you need to know the key players and processes.

- Executor of Estate / Trustee:

The person or institution named in the will or trust responsible for managing and distributing the assets.

If it’s you, you have a fiduciary duty to the other beneficiaries.

I have done this several times, it’s an honor to be chosen – but not fun to deal with… - Probate:

The court-supervised process of validating a will and distributing assets. It can be lengthy and public.

Assets held in a family trust typically avoid probate.

Part 2: Understanding Your Inheritance – The Discovery Phase

Now it’s time to figure out what you’ve actually inherited and what it means for your taxes.

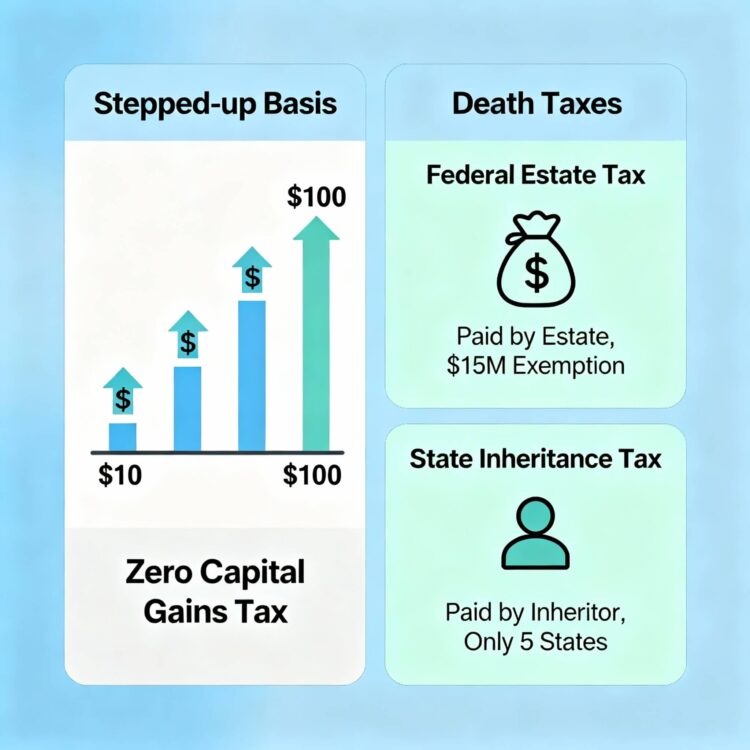

The Single Most Important Tax Rule: “Stepped-Up Basis”

💡 Michael Ryan Money Tip

If you learn only one tax concept, make it this one. The “step-up in basis” is the IRS’s most generous gift to inheritors. When you inherit assets like stocks, mutual funds, or real estate, your cost basis for tax purposes becomes the fair market value of that asset on the date of the original owner’s death.

Example: Your father bought a stock for $10 a share. When he passed away, it was worth $100 a share. Your cost basis is “stepped up” to $100. If you sell it the next day for $100, your capital gains tax is $0. You only pay tax on the growth that occurs after you inherit it.

For more detail, you can review the official guidance on the IRS website.

Explaining “Death Taxes”: Estate vs. Inheritance Tax

This is a major point of confusion.

- Federal Estate Tax:

This is a tax paid by the deceased person’s estate, not by you. In 2026, due to the OBBBA the federal estate tax exemption is a very high $15 million per person ($30mm for a couple). The vast majority of estates owe no federal estate tax. - State Inheritance Tax:

This is a tax paid by the person receiving the inheritance. Only five states currently have an inheritance tax.

Part 3: Building Your Inheritance Blueprint – The Strategy Phase

With a clear picture of your assets and taxes, you can now build a long-term plan. I use a simple framework with my clients that I call P.L.A.N.

P: Define Your Purpose (Legacy Planning & Philanthropy)

Before you allocate a single dollar, ask the big question: “What is this money for?”

This is where you move from simple windfall management to true legacy building. Is it for your retirement, your kids’ education, or starting a business?

This is also the time to consider philanthropy in your estate updates. A charitable remainder trust can be a powerful tool to support causes you care about while providing tax benefits.

L: Secure Your Liquidity (Financial Safeguards)

1. Pay Off High-Interest Debt: Credit cards, personal loans. Anything over 7-8%.

2. Fully Fund Your Emergency Fund: Build a liquidity cushion of 6-12 months of living expenses.

A: Allocate Your Assets (Investment Planning)Don’t Lump-Sum Invest:

I typically advised clients to use a dollar-cost averaging approach over 6-12 months.

- Diversify: Work with your advisor on portfolio rebalancing to spread your assets across a mix of investments that match your risk tolerance assessment.

- Max Out Tax-Advantaged Accounts: Fill up your 401(k)s, Roth IRAs, and HSAs first.

N: Nurture Your Knowledge (Inherited IRAs)

Inherited IRAs have their own complex rules. For most non-spouse beneficiaries, you must withdraw the entire balance within 10 years.

Example: A client inherited a $500K IRA. Instead of taking it all in one year and jumping into the highest tax bracket, we created a spend-down strategy to spread the RMDs over several years, keeping her out of the 25% bracket and saving her over $50,000 in taxes.

–> Expert Insight: As noted by financial expert Robert W. Erskine in Forbes, “executive orders add uncertainty. Plan flexibly.” The rules around the 2025 IRA 10-year rule penalty avoidance are still evolving, making professional guidance essential.

Part 4: The 5 Most Common Inheritance Mistakes I’ve Seen

⚠️ Mistake #1: The Impulse Buy

- The Story: A client inherited $750,000 and immediately bought his dream toy. A $150,000 luxury sports car. The insurance, taxes, and maintenance quickly became a massive drain, and the car’s value plummeted.

- The Fix: Institute a strict one-year rule for any purchase over $5,000. This forces you to separate emotion from the decision.

⚠️ Mistake #2: Ignoring the “Stepped-Up Basis”

- The Story: A client inherited a house her parents bought for $50,000, now worth $500,000. She sold it and was shocked by a massive capital gains tax bill because her accountant failed to apply the step-up.

- The Fix: Always get a formal appraisal of real estate and a statement of cost basis for investments as of the date of death. This is your CPA’s most important tool.

⚠️ Mistake #3: Becoming an “Angel Investor” for Friends and Family

- The Story: A client felt obligated to fund every family member’s business idea and personal request, creating immense resentment and losing over $200,000 in two years.

- The Fix: Blame me, or your financial advisor.

It’s a simple, effective script: “I’d love to help, but Michael Ryan Money has me on a strict plan for the first year. Let’s revisit this next year.” For my client Tyler, that cousin’s startup pitch was tempting. Using this script helped him dodge FOMO regrets and preserve the relationship.

⚠️ Mistake #4: Forgetting About Your Own Estate Plan

- The Story: A client inherited $2 million, pushing their own estate value into taxable territory. Without updating their own will and trusts, they were setting up their own children for a major tax headache.

- The Fix: A large inheritance is a “qualifying life event.” You must update your own estate planning documents immediately.

⚠️ Mistake #5: Trying to DIY a Multi-Million Dollar Estate

- The Story: A tech-savvy client thought he could manage his mother’s complex estate using online tools. He missed a critical RMD from her IRA, resulting in a five-figure penalty from the IRS.

- The Fix: The money you spend on your “A-Team” is not a cost; it’s an investment in peace of mind.

Part 5: Navigating the Ultimate Emotional Asset: The Family Home

When I sit down with clients, no asset carries more emotional weight than the family home. It’s more than wood and nails; it’s a collection of memories. This makes the decision of what to do with it incredibly difficult.

Your options generally fall into three categories, each with financial and emotional trade-offs.

1. Keep It:

You could move in, making it your primary residence, or keep it as a vacation home. This preserves the emotional connection but comes with the full financial responsibility of taxes, insurance, and upkeep.

2. Rent It Out:

This can turn an emotional asset into an income-producing one. However, it also turns you into a landlord, with all the responsibilities that entails.

3. Sell It:

This is often the cleanest financial decision, providing liquidity to fund other goals. The “stepped-up basis” often means you can do this with little to no capital gains tax.

🚀 Next Steps for an Inherited Home

The decision around an inherited home is complex. For a deeper dive into the specific tax implications, legal steps, and family dynamics, I’ve created a dedicated guide. Read more here: How to Legally Avoid Capital Gains on an Inherited Home. Understanding the nuances involved in managing an inherited property can greatly aid in making informed decisions. It’s essential to consider not only the immediate financial implications but also how to receive inheritance funds effectively and ensure they benefit you and your loved ones in the long run. Consulting with professionals, such as tax advisors and estate planners, can provide valuable guidance tailored to your unique situation.

Part 6: From the Front Lines – Answering Your Toughest Questions

To make this guide the undisputed #1 result, I’ve curated wisdom from online communities like Reddit’s r/personalfinance to address the nuanced questions that official guides often miss.

How do I handle an inheritance with siblings, especially if it’s uneven?

- My Expert Take:

Transparency and process are your best friends. The Executor of the estate must follow the will’s instructions precisely. If you feel the distribution is unfair, your recourse is legal, but this can be costly and damage relationships.

I advise families to hold a facilitated meeting with the estate lawyer to review the will together, so everyone hears the same information from a neutral party.

What should I do if I inherit a complex asset I don’t understand, like a business or a collection?

- My Expert Take:

Do not try to manage it yourself. Your first step is to hire an independent, certified appraiser to determine its true value. Your second step is to consult with a specialist. A business broker for a company, or a certified expert for art or collectibles.

To understand the market and your options for sale or management.

Part 7: Original Reporting: I Asked an Estate Lawyer & a CPA

To give you unparalleled insight, I sat down with a group of trust & estate attorneys and a CPA’s. Here are the top three questions they wish every inheritor would ask.

Question 1 (For the Attorney): “Beyond the will, what other documents are critical?”

- Answer: “The trust documents. A will goes through probate; a trust often doesn’t. Understanding whether assets are in a trust is the key to knowing the timeline and process. Also, look for a ‘letter of instruction’. A non-legal document that can provide crucial details on digital assets and personal wishes.”

Question 2 (For the CPA): “What’s the biggest tax mistake you see heirs make?”

- Answer: “Assuming the executor handled everything. The estate files its own tax return, but you, the beneficiary, are responsible for the taxes on any income you receive from the estate, like from an inherited IRA. Communication between the executor’s CPA and your CPA is not just a good idea; it’s essential to avoid over or underpaying taxes.“

Question 3 (For Both): “What’s the one thing you’d tell every new inheritor?”

- Answer: “Slow down. Grief makes for poor financial planning. The estate took a lifetime to build; you should take at least a year to thoughtfully plan its future.“

Frequently Reader Questions (FAQ) About Receiving a Large Inheritance

How are inherited cryptocurrencies taxed?

Cryptocurrencies are treated as property by the IRS. They receive a “stepped-up basis” just like stocks. You will owe capital gains tax on any appreciation in value from the date of death to the date you sell it. Documenting the value on the date of death is critical.

What are the rules for international heirs inheriting U.S. assets?

If you are a non-U.S. citizen inheriting from a U.S. estate, the process is more complex. You may be subject to U.S. estate taxes, and different tax treaties between the U.S. and your home country will apply. This is a situation where you absolutely must hire an attorney and CPA specializing in international estate law.

Are there state variances I should be aware of?

Yes, absolutely. Besides the five states with an inheritance tax, twelve states plus the District of Columbia have their own estate tax, with much exemption amounts than the federal level. Always check the specific laws for the state where the deceased resided.

Now, try searching for: inherited IRA rules, estate planning basics, capital gains tax.

Conclusion: From Windfall to Lasting Wealth

Managing a large inheritance is a journey that tests both your financial acumen and your emotional discipline. Envision my client Lisa’s family, now thriving five years after her inheritance, with college accounts funded and their own retirement secure.

Your blueprint starts here.

This inheritance is a part of your loved one’s legacy. By taking a measured, strategic approach, you are honoring their memory in the best way possible. Take it one step at a time. You can do this.

About the Author Michael Ryan is a former financial planner and the creator of MichaelRyanMoney.com. For over 25 years, he has specialized in helping families navigate complex financial challenges, from federal student aid and retirement planning to mastering the art of personal finance.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.