A military family sits down 20 years after separation, staring at a $1,100/month VGLI bill. They’re healthy. Their kids are grown. The mortgage is paid off. Yet they’re locked into a government program that costs nearly $14,000 annually. Money that could fund vacations, healthcare, or grandchildren’s education. This is the VGLI Veterans Group Life Insurance trap in action.

Key VGLI Takeaways Ahead

The 60-Second VGLI Decision Framework

The 2026 Rate Drop Masked a Bigger Truth:

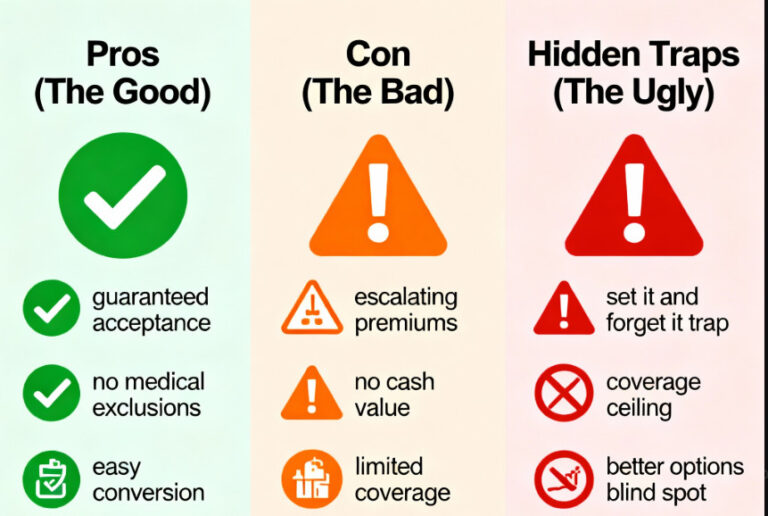

Yes, Veterans’ Group Life Insurance (VGLI) premiums decreased 2–17% on July 1, 2025. But they’re still dramatically more expensive than private term insurance across your career.

A 30-year-old veteran pays $420/year for $500k VGLI coverage; by age 50, that’s $6,600/year. By 60, it’s $13,200/year. VGLI uses attained age pricing with guaranteed renewable coverage—meaning premiums increase automatically in five-year age bands.

You Have a 240-Day Window (Then It Gets Harder):

You have 240 days after separation to enroll in VGLI without a medical exam. After that window closes, you’ll need proof of good health, which defeats the main advantage.

This makes Veteran Group Life Insurance policies perfect as a temporary bridge while you shop for private coverage. But dangerous as a permanent solution.

VGLI Isn’t Your Only Option:

Healthy veterans can almost always find cheaper, more flexible life insurance on the private market from veteran-focused insurers like Navy Mutual, AAFMAA, or USAA.

For more, read my helpful guide to understanding your life insurance options.

Veteran Group Life Insurance Coverage Has Hard Limits:

As of March 1, 2023, VGLI’s maximum coverage cap is $500,000. You can increase coverage by $25,000 increments every five years (after the first year) up to $500k, with no medical underwriting required.

But you cannot increase coverage after age 60. This ceiling may not match your actual income replacement needs.

What Is Veterans’ Group Life Insurance (VGLI)?

Veterans’ Group Life Insurance is a government-sponsored group term life insurance program administered by Prudential Financial under contract with the Department of Veterans Affairs. It allows service members to convert their Servicemembers’ Group Life Insurance (SGLI) into a civilian renewable policy after leaving the military.

Think of VGLI as a renewable term policy with guaranteed renewable coverage. You pay a premium to maintain protection, and if you pass away while active, your beneficiaries receive a tax-free death benefit. Unlike SGLI, which had one subsidized premium for all service members regardless of age, VGLI premiums are strictly age-based and increase over time.

The key difference:

VGLI uses attained age pricing with no level-premium locking period. Your rate climbs every five years as you age, regardless of your health or the broader economy.

VGLI vs. Private Term Life Insurance: The Real Cost Comparison

Here’s a direct premium comparison for a healthy 30-year-old veteran seeking $500,000 coverage:

Veterans’ Group Life Insurance (VGLI) provides crucial coverage for military service members, but premiums increase significantly with age. Comparing VGLI costs to private 20-year term life insurance reveals substantial price differences, particularly as you reach your 40s, 50s, and beyond. Understanding this cost comparison helps veterans make informed decisions about locking in rates early or exploring alternative coverage options.

| Age | VGLI Monthly | VGLI Annual | Private 20-Yr Term Annual | Annual Difference |

|---|---|---|---|---|

| 30 | $35 | $420 | $22 | +$398 (89% higher) |

| 40 | $70 | $840 | $22 | +$818 (3,600% higher) |

| 50 | $140 | $1,680 | $22 | +$1,658 (7,500%+) |

| 60 | $265 | $3,180 | $22 | +$3,158 (14,300%+) |

Lock in private term coverage before age 40 to avoid catastrophic premium increases—the difference between VGLI and private insurance grows exponentially as you age.

What this means in real money:

A veteran who enrolls in VGLI at separation and keeps it for 20 years will pay approximately $16,800 in total premiums. That same veteran in a level-term 20-year private policy would pay roughly $440. A difference of $16,360.

If that $398 annual difference (age 30–40) were invested at an 8% annual return, it would grow to $7,100 by age 48. That’s a down payment on a vacation home, funded by a single smart decision in your first 90 days of civilian life.

Common VGLI Myths vs. Reality

Myth #1: “My VA disability rating means I can’t get private life insurance.”

Reality: This is the most damaging myth in veteran financial planning. A VA disability rating is compensation for service-connected conditions, not a life expectancy sentence. Private insurers assess your specific health conditions, stability of management, and actual mortality risk.

Veterans with service-connected conditions like PTSD, traumatic brain injury (TBI), hearing loss, or back injuries frequently qualify for standard rate classes on private policies because these conditions don’t typically shorten life expectancy. The key factor underwriters evaluate is stability, not diagnosis.

Myth #2: “VGLI premiums stay the same for life.”

Reality: This is dangerously false and the root of the VGLI trap. VGLI premiums are on a fixed age-banded pricing schedule. Your rate jumps every five years regardless of your health status. By comparison, a private level-premium term policy locks your rate for 10, 20, or 30 years.

Private Insurance for Veterans: Understanding Underwriting with Disabilities

For veterans with service-connected disabilities, the idea of private insurance underwriting can feel intimidating. However, you have more pathways than you think.

Many insurers (particularly veteran-focused organizations like Navy Mutual and AAFMAA) specialize in policies for the military community and understand the nuances of service-related conditions.

Here’s what you need to know:

Stability Matters More Than Diagnosis:

Underwriters care about the stability and management of a condition more than the diagnosis itself. A veteran with well-managed PTSD who has been stable for 2–3 years may qualify for a standard rate. Someone with poorly controlled conditions may face substandard rates—but you’ll still have options.

Full Disclosure Is Non-Negotiable:

Always be honest and thorough on your application. Incomplete or misleading information gives an insurer grounds to void your policy during the underwriting period or deny a future claim.

Shop Around & Ask Directly:

Get quotes from multiple insurers and ask them directly about their underwriting guidelines for your specific conditions. Don’t assume you’ll be rejected based on a diagnosis alone.

Who Should Use VGLI? (And Who Should Avoid It)

The right choice depends entirely on your personal situation. Here are three scenarios based on real veteran financial planning:

Scenario 1: Transitioning Tom (Age 28, Healthy)

Situation: Tom separated from the Army in January 2026 at age 28. He’s healthy, married with one infant, and starting a civilian job paying $65,000. He needs $500,000 coverage to protect his family.

2026 Cost Comparison:

- VGLI: $35/month ($420/year)

- Private 20-year term: $22/month ($264/year)

Recommendation: Tom enrolls in VGLI immediately for guaranteed coverage during the 240-day window. Within 60 days, he applies for a private 20-year term policy. Once approved, he cancels VGLI.

The Math: Tom saves $156/year × 20 years = $3,120 in premium savings. If he invests that difference at 8% annually, he accumulates $7,100 in additional retirement savings by age 48.

Bottom Line: This is the textbook VGLI strategy. Use it as a bridge, never as a destination.

Scenario 2: Mid-Career Mike (Age 45, Service-Connected)

Situation: Mike separated in 2021 at age 40 with a 50% VA disability rating for back and knee injuries. He kept VGLI for “convenience” and is now 45. His 2026 VGLI premium just jumped from $180/month to $385/month—$4,620/year.

2026 Reality:

- VGLI Cost (Age 45): $385/month ($4,620/year)

- Private term (standard health): $310/year for $500k

- 5-Year cost difference: $21,550

Recommendation: Mike applies to 3–4 insurers specializing in veterans (Navy Mutual, USAA, AAFMAA). His stable, service-connected conditions don’t disqualify him—they move him from “preferred” to “standard” rates. He gets approved at $310/year.

The Math: Immediate savings: $4,310/year. Over the next 15 years until age 60: $64,650 in cumulative savings. That’s a down payment on a retirement home or a fully funded year of travel.

Bottom Line: Mike’s “set it and forget it” mentality cost him $21,550 over five years. The guaranteed acceptance he got in 2021 is worthless now—he’s been paying premium prices for outdated convenience.

Scenario 3: Retirement-Ready Rita (Age 58, Healthy)

Situation: Rita retired from the Air Force in 2016 at age 50 and kept VGLI. She’s healthy, but living on a fixed pension and Social Security. In 2026, her VGLI premium hit $1,100/month ($13,200/year) at age 60—eating 22% of her budget.

2026 Options:

- Current VGLI (Age 60): $1,100/month ($13,200/year)

- 10-year term ($200k): $850/year

- 10-year term ($100k): $475/year

Recommendation: Rita doesn’t need $500,000 anymore—her kids are grown, house is paid off, her pension covers living expenses. She applies for a senior-friendly 10-year, $100k policy at $475/year.

The Math: Immediate savings: $12,725/year. Over 10 years: $127,250—more than double the death benefit she’s purchasing. That’s a river cruise every year of retirement, or fully funded healthcare spending.

Bottom Line: Rita’s mistake was assuming she needed to keep the same coverage amount forever. Right-sizing your death benefit to match your current needs can save six figures in retirement.

How to Apply for VGLI: Step-by-Step

Step 1: Know Your Critical Deadlines

- First 240 Days Post-Separation (Guaranteed Issue Period):

- This is the best time to apply. You can apply online via VA.gov without answering any health questions. This is essentially a “free pass” to guaranteed coverage.

- Between 240 Days and 1 Year + 120 Days:

- You can still apply, but you’ll need to provide evidence of good health via medical questions or a medical exam. This defeats the main advantage of VGLI.

- After 1 Year + 120 Days: Y

- ou permanently lose the right to VGLI. This opportunity cannot be recovered.

Step 2: Gather Your Information

You’ll need:

- Your service number

- Social Security number

- Basic personal information

Step 3: Apply Online (The Easiest Route)

- Go to the official VA.gov life insurance page

- Log in with your DS Logon, My HealtheVet, or ID.me account

- Follow the prompts for the VGLI application

- Submit and confirm receipt

Step 4: Plan Your Exit (Within 60–90 Days)

- Request quotes from at least 3–4 private insurers

- Compare total 20-year costs (not just monthly premiums)

- Once approved for private coverage, cancel VGLI effective the date your new policy begins

- Document the cancellation to avoid duplicate premiums

Common VGLI Questions Answered

Is VGLI term or whole life insurance?

VGLI is term life insurance. It provides a death benefit but has no cash value or investment component. Unlike whole life insurance, you build no equity.

Can I convert VGLI to a whole life policy?

Yes. VGLI policyholders have a conversion privilege, allowing conversion to a commercial whole life insurance policy at any time with participating private insurers—guaranteed regardless of your health. However, whole life is significantly more expensive than term.

Is VALife (VA Whole Life) better than VGLI?

No. Veterans Affairs Life Insurance (VALife) is a whole life program for veterans with service-connected disabilities offering up to $40,000 in coverage, with a two-year waiting period for the full death benefit. VGLI offers much higher coverage amounts ($500k) and is available to a broader group of veterans. For most, VGLI is superior to VALife—but private term is superior to both

What happens if I miss the VGLI application deadline?

If you miss the 1 year and 120-day deadline, you are permanently ineligible for VGLI. Your opportunity to convert your SGLI is gone forever. This is why the 240-day window is so critical.

Your 2026 VGLI Action Plan

After extensive financial planning work with veteran families, here’s the strategic framework:

Treat VGLI as a bridge, not a destination.

The 6-Step Action Sequence

Days 1–30: Enroll in VGLI

- Apply online via VA.gov

- Secure guaranteed coverage during the 240-day window

- File confirmation documents

Days 31–60: Request Private Insurance Quotes

- Contact Navy Mutual, AAFMAA, and USAA

- Request quotes for 20-year level-term policies

- Ask about their underwriting guidelines for your specific health situation

- Full disclosure on medical history (non-disclosure voids policies)

Days 61–90: Complete Medical Underwriting

- Undergo medical exam if required

- Respond promptly to insurer requests for documentation

- Compare 20-year total cost, not just monthly premiums

Days 91–120: Receive Approval & Lock in Private Coverage

- Confirm approval from your chosen private insurer

- Schedule your policy’s effective date

- Provide written cancellation notice to VGLI, effective the date your new coverage begins

Days 121–180: Verify Cancellation & Redirect Savings

- Confirm VGLI cancellation in writing

- Check your next statement to ensure no duplicate premiums

- Invest the premium difference in a Roth IRA or taxable brokerage account

Ongoing: Annual Review

- Every year, confirm your private policy is active

- Periodically review coverage amount to ensure it matches your life stage

- Consider term insurance conversion options as you approach the end of your term (if relevant)

The Bottom Line: Why This Matters in 2026

The veterans who regret VGLI most are the ones who “meant to shop around” but never did. Five years later, they’re hemorrhaging money on premiums that could have funded:

- A $12,725/year vacation budget (Rita’s scenario)

- Children’s college education (Tom’s scenario)

- Healthcare expenses and living improvements (Mike’s scenario)

The transition from military to civilian life is overwhelming. VGLI feels safe, familiar, and “already set up.” But that single default decision—made without thinking in your first 90 days—can cost you $50,000–$200,000 over your working lifetime.

Your family deserves better than the default option. Take control of this decision in 2026, and your future self will thank you with every premium you didn’t pay.

Additional Resources for Veterans

- VA.gov Life Insurance Overview – Official VA insurance information

- VA Disability Rating Guide – Understanding your service-connected conditions for insurance purposes

- USAA Veteran Life Insurance – Veteran-focused private insurer

- Navy Mutual Association – Veteran-owned insurer

- Financial Planning for Military Families – Comprehensive financial roadmap

- Life Insurance for Seniors – Options as you age out of traditional term coverage

- How to Calculate Your Liquid Net Worth – Understanding your financial position before major decisions

- Roth IRA Contribution Limits 2026 – Where to invest VGLI premium savings

- Retirement Planning for Veterans – Integrating VGLI/life insurance into broader retirement strategy

Disclaimer

This article is for educational purposes only and does not constitute financial or insurance advice. All insurance decisions should be made in consultation with a qualified licensed professional. VGLI rates, rules, and eligibility requirements are subject to change; please consult the official VA.gov website for the most current information. Private insurance quotes and underwriting outcomes vary by individual health status, age, and insurer—get personalized quotes before making a decision.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.