You’ve worked hard, saved diligently, and now you’re enjoying retirement. But have you considered life insurance as a senior? It might seem counterintuitive, but for many retirees, it’s a crucial piece of the financial puzzle.

- Quick answer: Life insurance for seniors can provide peace of mind, protect your loved ones from unexpected expenses, and even serve as a wealth transfer tool.

- Here’s the deal: Life insurance isn’t just for young families anymore. As a retirement planning expert, I’ve seen firsthand how the right policy can be a game-changer for seniors. It’s not about replacing lost income; it’s about smart financial planning.

Think about this:

- Did you know that funeral costs average $7,000 to $12,000? That’s a hefty bill to leave behind.

- Are you carrying any debt into retirement? Life insurance can ensure you don’t pass that burden to your family.

- Want to leave a legacy? Some policies can help you transfer wealth tax-efficiently.

But here’s the kicker: Finding the right policy at the right price can be tricky. Age and health issues can drive up costs, but don’t worry – I’ve got some insider tips to help you navigate this.

Key Takeaways Ahead

Quick Quiz for you. Which Life Insurance Best Fits Your Needs? Click the correct answers below:

1. Which type of life insurance typically has the lowest premiums for seniors?

2. Which policy type guarantees acceptance regardless of health status?

Stay with me, and I’ll show you how to secure your golden years without breaking the bank. Trust me, by the end of this article, you’ll see life insurance in a whole new light.

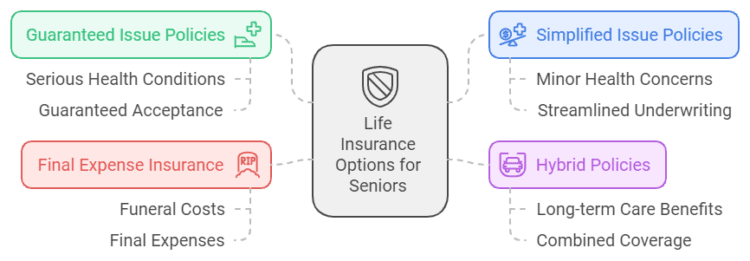

The world of life insurance for seniors has evolved dramatically in recent years. Gone are the days when your options were limited to basic term or whole life policies. Today’s market offers a variety of products tailored to the unique needs of older adults:

- Guaranteed issue policies: Perfect for those with serious health conditions

- Simplified issue policies: Ideal for seniors with minor health concerns

- Hybrid policies: Combining life insurance with long-term care benefits

- Final expense insurance: Focused on covering end-of-life costs

5 Surprising Reasons Seniors Need Life Insurance

Many seniors assume they no longer need life insurance after retirement. However, there are several compelling reasons why life insurance remains valuable for older adults. Let’s explore five surprising ways life insurance can benefit seniors and their families.

CBSNews: Why seniors should consider life insurance

Beyond the Grave: Protecting Your Loved Ones

Even in retirement, life insurance can provide crucial financial protection for your family. While you may no longer need to replace lost income, a life insurance policy can help:

- Pay off any remaining debts or mortgage balances

- Provide financial support for a surviving spouse

- Leave an inheritance for children or grandchildren

- Cover unexpected medical bills or long-term care costs

Life insurance gives seniors peace of mind knowing their loved ones will be financially secure after they’re gone.

The $9,000 Problem: Tackling Funeral Costs Head-On

Funeral expenses can be a significant financial burden for families. The average funeral costs between $7,000 and $12,000, including the viewing, burial, service fees, transport, casket, embalming, and other preparations.

📊 Quick Stat

According to the National Funeral Directors Association (NFDA), the median cost of a funeral with a viewing and burial is $8,300, and with cremation, it is $6,280. This does not include the cemetery plot, headstone, or flowers, which can easily push the total cost over $12,000.

A life insurance policy can cover these costs, ensuring your family doesn’t face financial strain while grieving. Some insurers even offer specific final expense or burial insurance policies designed to cover funeral costs and other end-of-life expenses.

Uncle Sam’s Cut: Navigating Estate Taxes with Ease

For seniors with substantial assets, estate taxes can take a significant bite out of the inheritance left for heirs. Life insurance can help offset these taxes, allowing more of your estate to pass to your beneficiaries.

While the federal estate tax exemption is currently high ( $13.61 million in 2024 & 2025.), some states have lower thresholds. A life insurance policy can provide liquidity to pay estate taxes without forcing your heirs to sell assets.

The Long-Term Care Lifeline: When Health Takes a Turn

Some life insurance policies offer riders or benefits that can help cover long-term care expenses. These options allow you to access a portion of your death benefit while you’re still alive if you need assistance with daily living activities or face a chronic illness.

This feature can provide a financial lifeline if you require extended care, helping to preserve your retirement savings and reduce the burden on your family.

Business Doesn’t Retire: Ensuring Your Legacy Lives On

For senior business owners, life insurance plays a crucial role in succession planning. It can:

- Provide funds for buy-sell agreements

- Equalize inheritances among heirs if the business is passing to one child

- Cover any estate taxes on the business

- Ensure the business has cash flow to continue operations after your death

Life insurance helps ensure your business legacy continues smoothly after you’re gone.

Did You Know?

📊 The Senior Coverage Gap

According to a 2021 study, only 46% of adults aged 65 and older own life insurance. This suggests many seniors may be underinsured and at risk of leaving unexpected financial burdens to their families. The right policy closes this gap and provides crucial peace of mind.

By understanding these surprising benefits, seniors can make informed decisions about whether life insurance fits into their overall financial and estate planning strategy.

Cracking the Code: Life Insurance Types Tailored for Seniors

Let’s face it – navigating life insurance options as a senior can feel like decoding a secret message. But don’t worry, I’m here to break it down in plain English. After years of helping seniors find the right coverage, I’ve seen firsthand how the right policy can provide peace of mind and financial security. So, let’s dive into the world of senior-friendly life insurance and find the perfect fit for you.

Senior Life Insurance at a Glance

| Feature | Term Life | Whole Life | Guaranteed Issue | Final Expense |

|---|---|---|---|---|

| Best For | Covering specific, large debts with a clear end date (like a mortgage). | Lifelong coverage, estate planning, and building cash value. | Seniors with serious health issues who can’t get other coverage. | Covering burial costs and other small end-of-life debts affordably. |

| Medical Exam? | Usually required for the best rates, but “no-exam” options exist. | Yes, a medical exam is typically required. | No medical exam or health questions required. | No medical exam, just a few health questions (“simplified issue”). |

| Coverage Amount | High ($100k – $1M+) | High ($50k – $1M+) | Low (Typically $5k – $25k) | Low (Typically $5k – $35k) |

| Typical Cost | Lowest initial cost. A healthy 70-year-old might pay $150-$250/mo for a $100k, 10-year policy. | Highest cost. A healthy 70-year-old could pay $500-$900+/mo for a $100k policy. | Very high for the coverage amount. A 70-year-old might pay $100-$200/mo for just $10k of coverage. | Affordable. A healthy 70-year-old might pay $50-$120/mo for a $10k-$15k benefit. |

| Cash Value? | No | Yes, it grows over time and can be borrowed against. | No | Yes, but it grows very slowly compared to Whole Life. |

| Key Pro | Most coverage for the lowest initial premium. | Permanent coverage that never expires and builds equity. | Guaranteed acceptance for almost everyone. | Simple, affordable way to cover funeral costs and give peace of mind. |

Compare prices among America’s top insurers with PolicyGenius

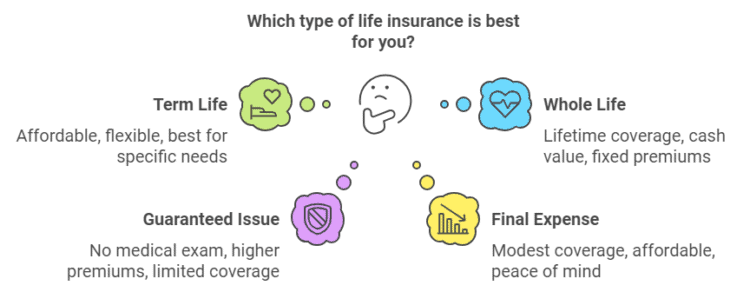

Term Life: Short-Term Solution or Senior Superhero?

Think of term life as the sprinter of the insurance world – fast, focused, and perfect for specific goals. Here’s the scoop:

- Affordability: Often the cheapest option, especially for healthy seniors

- Flexibility: Choose coverage lengths from 10 to 30 years

- Simplicity: No bells and whistles, just straightforward protection

But here’s a pro tip: Timing is everything. I once helped a client save 20% on her premiums by buying just two months before her next birthday. Insurance companies use age brackets, so strategic timing can be a game-changer.

When Term Life Shines:

- Covering a mortgage that’ll be paid off in 15 years

- Providing income replacement until your spouse reaches retirement age

- Protecting adult children who still depend on you financially

Remember, term life only pays if you pass away during the policy period. It’s not a lifetime solution, but it can be a superhero for specific needs.

| Policy Type | Premium Cost | Coverage Amount |

|---|---|---|

| Term Life Insurance | Lowest cost option; renewable every 5-10 years based on health status at time of renewal | Varies depending on age and health condition |

| Whole Life Insurance | Higher initial premium costs but fixed rates | Guaranteed death benefit amount regardless of age or health condition |

| Universal Life Insurance | Flexible premium payments with potential tax advantages | Can build cash value over time with higher coverage amounts available |

Whole Life: Building a Financial Fortress

Whole life is the marathon runner of insurance – in it for the long haul. It offers lifelong coverage plus a cash value component that grows over time. Here’s why some seniors love it:

- Lifetime Coverage: As long as you pay premiums, you’re covered

- Cash Value Growth: Build tax-deferred savings you can borrow against

- Fixed Premiums: Lock in your rate for life

Real-Life Example: I had a client use her whole life policy’s cash value to fund a dream vacation in her 70s. It’s not just about the death benefit – it can be a financial tool during your lifetime too.

When Whole Life Makes Sense:

- You want coverage that never expires

- You’re looking for an additional tax-deferred savings vehicle

- You want to leave a guaranteed inheritance

Guaranteed Issue: When “No” Isn’t an Option

Ever been turned down for insurance? Guaranteed issue policies say “yes” when others say “no.” Here’s the lowdown:

- No Medical Exam: Acceptance guaranteed, regardless of health

- Higher Premiums: You pay more for the guaranteed acceptance

- Limited Coverage: Death benefits are typically lower

Insider Tip: Some guaranteed issue policies have a “graded benefit” period. This means if you pass away in the first 2-3 years, your beneficiaries might only receive a refund of premiums paid plus interest. Always read the fine print!

When Guaranteed Issue Fits:

- You have serious health issues and can’t qualify for other policies

- You need a small amount of coverage for final expenses

- You’re willing to pay more for the guarantee of coverage

Final Expense: Small Policy, Big Peace of Mind

Final expense insurance is like the reliable compact car of the insurance world – it won’t take you on a cross-country road trip, but it’ll get you where you need to go. Here’s what you need to know:

- Modest Coverage: Usually $5,000 to $25,000

- Affordable: Lower premiums due to smaller coverage amounts

- Peace of Mind: Ensures loved ones won’t face burial costs

True Story: I once helped a client in her 80s get a final expense policy. She told me, “I don’t want my kids arguing over my funeral costs.” That $10,000 policy gave her incredible peace of mind in her final years.

When Final Expense Works:

- You want to cover funeral and burial expenses

- You’re on a fixed income and need affordable coverage

- You want to leave a small inheritance without breaking the bank

Remember, choosing the right life insurance isn’t just about comparing quotes. It’s about understanding your unique situation and thinking outside the box. I’ve seen too many seniors overpay or end up with inadequate coverage because they didn’t know all their options.

My tips? Work with an experienced agent who specializes in senior policies. They can help you navigate the complexities and find the perfect fit for your needs and budget. After all, the right life insurance policy isn’t just about money – it’s about peace of mind for you and your loved ones.

Compare prices among America’s top insurers with PolicyGenius

Your Roadmap to the Perfect Policy: 4 Steps to Success

Finding the right life insurance policy as a senior doesn’t have to feel like solving a Rubik’s cube blindfolded. Let’s break it down into four manageable steps that’ll have you feeling like a pro in no time.

A Can’t Miss Read – The Ultimate Guide & Overview of Insurance – All Things Insurance

Number Crunching: How Much Coverage Do You Really Need?

First things first: let’s figure out how big your safety net should be. It’s not about shooting for the stars here; it’s about smart planning.

Think about this: I once had a client, let’s call him Bob, who was adamant about getting a million-dollar policy. After we sat down and crunched the numbers, we realized he only needed about a third of that. The money he saved on premiums? Well, let’s just say his grandkids are enjoying some pretty sweet birthday presents now.

Here’s a quick checklist to get you started:

- Outstanding debts (mortgage, credit cards)

- Estimated funeral costs

- Any income you’re still providing for your family

- Legacy goals (leaving money for family or charity)

Now, subtract any savings or investments you already have. The result? That’s your ballpark coverage amount.

Pro tip: Don’t forget to factor in inflation. What seems like a lot now might not stretch as far in 10 or 20 years.

Health Check: Turning Medical History into Policy Gold

Now, let’s talk about the elephant in the room: your health. But here’s the thing – it’s not always the deal-breaker you might think it is.

I remember a client, Margaret, who was sure her diabetes would disqualify her from getting coverage. We dug a little deeper, found an insurer who specialized in policies for diabetics, and not only did she get coverage, but the premiums were way lower than she expected.

Here’s how to ace this step:

- Be upfront about your health conditions. Honesty is always the best policy.

- Highlight any positive changes. Quit smoking? Lost weight? Brag about it!

- Consider no-exam policies if you have serious health concerns.

Remember, insurers are getting smarter about health conditions. What might have been a red flag a decade ago could be totally manageable now.

Shop Smart: The Art of Quote Comparison

This is where the rubber meets the road. Getting quotes is like dating – you’ve got to play the field a bit before you find “the one.”

Here’s a secret from the trenches: prices can vary wildly between insurers for the exact same coverage. I once saved a client over $1,000 a year just by shopping around. That’s a nice vacation right there!

Your game plan:

- Use online comparison tools to cast a wide net.

- Talk to an independent agent who can access multiple insurers.

- Look beyond just the price. Consider the company’s reputation and financial strength too.

Pro tip: Don’t be shy about negotiating. Sometimes, a little back-and-forth can land you a better deal.

| Insurance Company | AIG Life Insurance For Seniors | American Family Life Insurance Company |

|---|---|---|

| Life Insurance Complaints | Low | High |

| Life Insurance Providers Options For Seniors | Extensive | Limited |

| Health Issues Covered By Policies | Yes | No |

Fine Print Detective: Unmasking Policy Features and Riders

This is where the good stuff (and sometimes the gotchas) hide.

I had a client once who almost missed out on a critical illness rider that would have been perfect for her situation. It was buried in the fine print, but boy, was she glad we caught it.

Here’s your investigation checklist:

- Understand the policy type (term, whole life, universal life)

- Check if premiums are fixed or if they’ll increase

- For permanent policies, get the lowdown on cash value

- Look into riders like accelerated death benefits or long-term care options

Pro tip: If something doesn’t make sense, ask. Then ask again. You’re not being a pain; you’re being smart.

Estimate Your Life Insurance Needs in 60 Seconds

Senior Life Insurance Needs Calculator

Remember, finding the right life insurance policy as a senior is like tailoring a suit. It needs to fit you perfectly, not just in size, but in style and function too. Take your time, do your homework, and don’t be afraid to ask for help. Your perfect policy is out there – now go find it! and budget. After all, the right life insurance policy isn’t just about money – it’s about peace of mind for you and your loved one

Red Flags and Pitfalls to Avoid

In my years of practice, I’ve seen seniors fall victim to various insurance pitfalls. Here are some key warning signs:

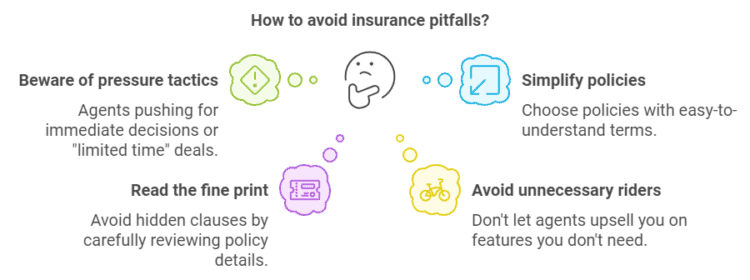

💡 Michael Ryan’s Advisor Tip: How to Spot a Bad Deal

In my years of practice, I’ve seen seniors get pushed into bad policies. Watch for these red flags:

- High-Pressure Tactics: An agent pushing for a decision “today” is a major warning sign.

- Overly Complex Policies: If the agent can’t explain it simply, don’t buy it.

- Unnecessary Riders: Avoid paying for bells and whistles you don’t need, like double indemnity for accidental death.

- Hidden Waiting Periods: Always ask, “When does the full death benefit become active?” Some policies have a 2-year waiting period.

Let’s tackle some common misconceptions about life insurance for seniors and reveal the truth behind these myths.

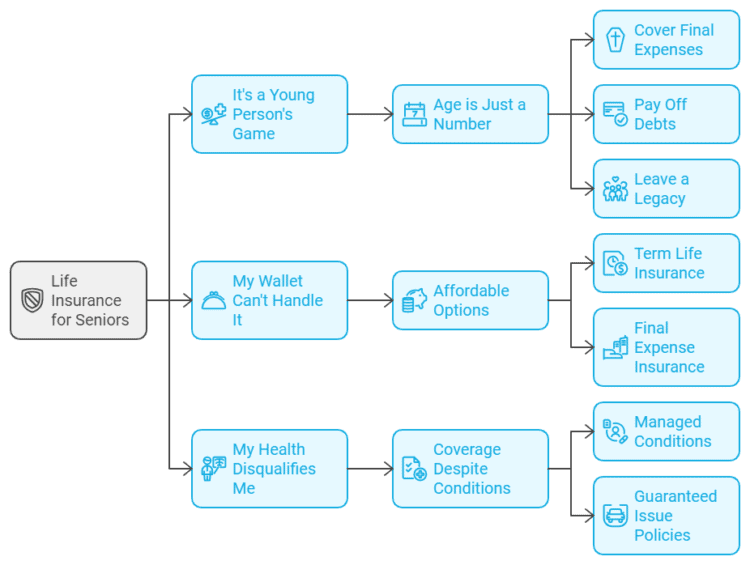

⚠️ Myth Busted: “It’s a Young Person’s Game.”

The Truth: Life insurance isn’t about age; it’s about needs. In fact, Baby Boomers lead all generations in policy ownership (57%). For seniors, it’s a powerful tool for covering final expenses, paying off debts, and leaving a tax-free legacy.

Why? Because life insurance can help seniors:

- Cover final expenses

- Pay off lingering debts

- Leave a legacy for loved ones

Remember, it’s not about your age – it’s about your needs and goals.

⚠️ Myth Busted: “My Wallet Can’t Handle It.”

The Truth: Many seniors overestimate the cost. While premiums are higher than for a 30-year-old, policies focused on final expenses can be very affordable, often ranging from $50 to $120 per month for a meaningful benefit that protects your family from debt.

Consider these affordable choices:

- Term life insurance: Great for specific, time-limited financial obligations

- Final expense or burial insurance: Lower coverage amounts mean lower premiums

Don’t let cost fears stop you from exploring your options. You might be surprised at what’s within reach.

⚠️ Myth Busted: “My Health Disqualifies Me.”

The Truth: This is rarely true anymore. Many insurers offer policies for managed conditions like diabetes. For more serious issues, “Guaranteed Issue” policies require no medical exam, ensuring almost everyone can get coverage to protect their loved ones.

Even if you have more serious health issues, guaranteed issue policies don’t require a medical exam. While these may have higher premiums or lower coverage amounts, they ensure almost everyone can get some form of coverage.

Compare prices among America’s top insurers with PolicyGenius

Success Stories: How Seniors Are Winning with Life Insurance

Let’s look at how real seniors have used life insurance to their advantage.

The Widow’s Financial Shield: Mary’s Story

Mary, 72, lost her husband unexpectedly. Thanks to their foresight in keeping a life insurance policy, Mary received a $250,000 death benefit. This allowed her to:

- Pay off their remaining mortgage and cover funeral expenses

- Maintain her quality of life without financial stress

Grandpa’s Education Fund: Building a Legacy of Learning

Tom, 65, wanted to ensure his grandchildren could afford college. His solution? A $100,000 whole life policy with his grandchildren as beneficiaries. The policy’s cash value component grew over time, providing a tax-advantaged way to contribute to their education funds.

The Business Continuity Masterstroke: Bob’s Brilliant Move

Bob, 70, owned a successful small business. He took out a $500,000 life insurance policy as part of a buy-sell agreement. When he passed away unexpectedly, the policy provided funds for his business partner to buy out Bob’s share, ensuring:

- A smooth business transition

- Financial security for Bob’s family

Insider Tips: Maximize Your Life Insurance Strategy

Ready to make the most of your life insurance as a senior? Try these expert strategies.

The Early Bird Special: Lock in Lower Rates Now

When it comes to life insurance, procrastination costs you. Each year of delay can bump up premiums by 9%-12%. If you’re considering life insurance, act now to lock in your best rate.

Policy Laddering: The Secret to Flexible Coverage

Instead of one large policy, consider multiple smaller policies with different term lengths. This strategy provides:

- Higher coverage when you need it most (like while paying off a mortgage)

- Lower coverage (and lower premiums) as your financial obligations decrease

It’s a smart way to tailor your coverage to your changing needs.

Your Next Steps: Securing Your Future Starts Today

Remember, it’s never too late to make smart decisions about your financial security. By taking action now, you’re not just buying a policy – you’re investing in peace of mind for yourself and your loved ones.

Don’t let another day pass without taking control of your financial future. Start your journey towards affordable, effective life insurance coverage today. Your future self (and your family) will thank you.

Additional Resources:

- NAIC

- American Bar Association

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.