When it comes to life insurance, being prepared is crucial. While it may seem like a complex topic, having the right coverage can provide vital financial /overview-of-the-financial-planning-process/security for your loved ones in the event of your passing. In this comprehensive guide, we will delve into all the essential aspects of life insurance.

💡 2026 Update

Life insurance costs rose 3-6% in 2026, but the federal estate tax exemption jumped to $15 million per person—making permanent life insurance more valuable for high-net-worth families. Term insurance remains the most affordable option for income replacement, with healthy 35-year-olds still locking in $500,000 of 20-year coverage for under $30/month.

From understanding the various policy types to determining costs, calculating the appropriate coverage amount, and discovering tips for securing the best rates, you will gain the knowledge necessary to make informed decisions. Our goal is to simplify the process, offering clear, actionable steps that will bring you peace of mind, knowing that your family’s future is protected.

What The Experts Have To Say About Life Insurance

Kevin Caballaro, Owner of Caballaro Agency

- Consider term insurance or permanent/cash value life insurance when choosing a life insurance policy, depending on your objectives.

- The financial strength of the insurance company is important to ensure the stability of your policy and the preservation of its features.

- Explore the availability of living benefits, which allow you to access the death benefit proceeds if diagnosed with a chronic or terminal condition, providing financial support during difficult times.

What’s The Purpose of Life Insurance?

“The benefits of having life insurance include providing financial security for your loved ones in the event of your passing, peace of mind, and potentially helping pay for final expenses.”

Kevin Caballaro, Owner of Caballaro Agency

- Do I have financial obligations, life events and family members who rely on me for financial security and financial support?

- Life expenses, final expenses, burial expenses, funeral expenses, income replacement, etc

- A mortgage to pay or credit cards?

- A spouse who would need day to day money and to save for retirement

- Dependent children who want a college education, etc?

- Can I afford to pay for all of those things today?

- Do I have enough saved that if I don’t make it home tonight, everything is more than covered?

- If I get hit by a drunk driver on the way home tonight, is this a risk I am willing to take?

- And leave the financial burden with my survivors?

- Or would I prefer to small a much lesser amount, and transfer this risk to someone else?

- Would I prefer to pay a small amount each month to make sure these things are taken care of with the advantages of life insurance?

- There are many types of affordable life insurance options, life insurance solutions and types of coverage – such as basic life insurance coverage – at affordable rates.

What Is Life Insurance?

Life insurance is an agreement, known as a contract, between you and an insurance company.

The agreement is that you will pay an amount of money, called premium payments, in return the insurance company will pay who you name (called “beneficiaries”) an amount of money or “death benefit amount”.

There are lots of types of life insurance policies, and they range in how much the cost. The most important factors of cost are how much insurance you want, your age, your health, and how long you want to own the policy. Before deciding how much life insurance you need or what type, let’s first get a better understanding of what goes into a life insurance policy.

A Can’t Miss Read – The Ultimate Guide & Overview of Insurance – All Things Insurance

Why Life Insurance is Important?

In my years as a financial planner, I’ve seen firsthand the incredible value of life insurance for protecting loved ones.

I’ve sat with too many grieving widows who were left struggling financially because they had no life insurance. The hardship and stress at an already difficult time was heartbreaking.

On the other hand, I’ve seen relieved widows able to grieve without the crushing weight of financial turmoil because their husband had life insurance. It made a tremendous difference in their ability to heal.

I’ve also witnessed the impact on children when a parent passes without life insurance. The family’s finances were ravaged and the kids’ education derailed. However, with life insurance, the children were able to pursue their dreams unhindered.

As a father myself, I sleep better at night knowing my family is protected if I were gone. The peace of mind is irreplaceable. I want that for my clients too.

After walking with so many clients through deep loss, I’m adamant about having life insurance. It allows you to fully focus on healing, not finances. My advice comes straight from the heart.

⚠️ The $180,000 Mistake

Most families choose whole life when term would save them $9,000/year over 20 years—that’s $180,000 that could’ve funded college or retirement. Only 3% of Americans actually need permanent insurance. Don’t let commission-driven advice cost you six figures.

- Financial Protection

- Peace of Mind

- Affordability

- Replacing Income

- Tax-Free Benefit

- Legacy Planning

- Cash Value

- Guaranteed Cash Value Growth

- Business Continuity

SUMMARY

- This guide will walk you through the entire process of getting life insurance

- The guide will also help you decide to stop procrastinating. And make decisions about life insurance today.

- There are lots of types of life insurance policies, and they range in how much they will cost you. Term insurance is temporary – coverage for a limited period of time. Usually 10, 20 or 30 years.

- Whole life insurance provides a “guaranteed” permanent death benefit amount that also builds a cash reserve over time.

- Term insurance is very cheap and protects your family, but there are some downsides. Term insurance is temporary. After x number of years – you will no longer have life insurance coverage.

- When Does Permanent Life Insurance Make More Sense Than Term Insurance? Do you need life insurance forever? I can’t decide that, only you can.

Key Points

- Before deciding how much life insurance you need or what type, let’s first get a better understanding of what goes into an insurance policy.

- There are different ways to calculate how much life insurance you need.

- How long do you want an insurance policy to last?

- The two main types of life insurance policies are term insurance and permanent life policies.

- The same way you build equity in your home, you can build equity in a permanent life insurance policy.

The simple answer to “what is life insurance”? Life insurance provides a lump sum of money to those who depend on you, in the event of your death.

michaelryanmoney.com

There are other purposes that insurance can be used for, but in most cases it is to provide for a spouse and/or surviving dependent children. This can include a stay at home parent – often people feel if they don’t work, they don’t need life insurance. They don’t realize that the cost of child care is about to go through the roof.

- There are multiple types of life insurance to choose from.

- There are different ways to calculate how much life insurance you need.

- By the end of this guide you will feel comfortable with all of your questions being answered and ready to protect your family.

Have you already decided that you are curious about getting life insurance for yourself?

if so, I highly suggest you head over to PolicyGenious and get quotes to compare prices and life coverages.

It’s a great no pressure way to start your research.

Compare prices among America’s top insurers

With PolicyGenius TodayWhat Types Of Life Insurance Do I Have to Choose From?

Let’s make this difficult subject a bit easier.

Pretend you are looking for a place to live. You can typically buy a home or rent a place. Then there are other deciding factors – cost, location, how long will we stay there, etc.

Insurance is not very different. You essentially have to ask yourself many of the same questions:

- How long do I want a life policy to last?

- Who do I want to be the beneficiary of the policy and why?

- What do I want to protect?

- How much will life insurance cost?

“Choosing the best life insurance policy for your needs can be overwhelming, but some factors to consider include your budget, the length of coverage needed, and any riders you may want to add to the policy.”

Kevin Caballaro, Owner of Caballaro Agency

What Is The Difference Between Whole Life and Term Insurance?

The two main types of life insurance policies are term insurance vs whole life insurance. How is this like finding a place to live?

- Term is temporary insurance

- Whole life insurance is more permanent – you keep it as long as you want it.

- Term insurance is like renting a home, whole life insurance is like buying a home.

The same way when you buy a home, you ‘build equity’ in your home as part of your monthly mortgage payment goes towards interest and part of it goes to principal. Allowing you to build equity. A whole life policy will also allow you to build equity. Let’s get into some more details.

Temporary Insurance:

- Term Life InsurancePolicy

- Inexpensive and temporary

Permanent Life Insurance

Expensive, permanent, guaranteed rate of return (like CDs)

Expensive, permanent, flexible premiums and death benefit

Expensive, permanent, more flexible investment choices

What is Term Life Insurance? What is Whole Life Insurance?

- What is Term Life Insurance?

- How Does Term Insurance Work?

- What is Whole Life Insurance?

- How Does Whole Life Insurance Work?

- Temporary – coverage for a limited period of time

- Usually 10, 20 or 30 years

- Meant to cover financial needs that won’t last forever

- Simple, and very inexpensive

- Makes sense if there is a future date that no one will be depending on you financially (kids frown, mortgage paid off)

- Good for replacing an income and paying off debts, or for business policies

- So you both agree “I will pay you $x a year for the next 20 years, and if I die between now and then you will pay $Y00,000 to my family”.

- The same way you agree with your landlord, “I will pay you $x a month for the next year to live here”.

- And when the agreed amount of time passes, you both move on.

- More expensive than term insurance. Typically 15 times more expensive than term insurance. But…

- Designed to last forever, or your lifetime

- Can also build a cash value that you may be able to access at any time.

- Premiums may be setup to stay the same forever

Whole life insurance is now a little bit more like buying your home. It is a bit more permanent. Just like with term insurance, if you die while you own the whole life policy – the insurance company will pay out to your beneficiaries. Unlike the set number of years like term insurance, a whole life insurance policy is designed to last for your lifetime.

Whole life policies cost more than term life policies for two reasons:

- The policy will last longer than a term life policy and will eventually pay a death benefit

- Part of the premium you pay goes into a ‘savings account like’ account, and builds equity.

In addition to providing a benefit when you pass away, a permanent policy has an added benefit. The same way you build equity in your home, you can build equity in your life insurance policy. The extra premiums get invested, and the earnings grow in a cash reserve account. You can even borrow from this amount in the future, if necessary.

There are many different types of permanent insurance, but whole life is by far the most popular. With whole life insurance, you have a “guaranteed” permanent death benefit amount that also builds a cash reserve over time.

There are three components of Whole Life Insurance

- The cost of the policy, or premiums

- Substantially more than Term Insurance, usually about 15 to 20 times higher

- The benefit of the policy, the amount of insurance paid to your beneficiaries

- This is permanent, not for a short fixed period like term insurance this is partially why it is so much more expensive than term insurance. You are paying a premium to cover your young years, and when you are 90!!

- The cash valuecomponent, the underlying investment option part of your policy.

- This is primarily where the extra premiums over term insurance is going. This is where the investment/savings component goes. Many people use the tax deferred growth potential of the cash value as part of their retirement plans.

- This is VERY important. Upon your death, your beneficiaries ONLY get the death benefit, not the cash value component.

- This keeps the cost of insurance down at your later years of life. You are essentially paying for coverage of the difference of the death benefit amount and your cash value.

- Example. You have a $500,000 death benefit and $200,000 of cash value. You are paying for insurance for that gap of $300,000 – not the full $500,000. You are partially self insured.

- You may be able to choose to cancel your life insurance policy and collect the net cash value. Speak with a tax advisor regarding any potential tax implications of doing so.

- You may be able to “borrow” against your cash value, if necessary

- Whole Life policies are typically very poor “investments”, earning on average less than 2.5% per year (stats, link). Think of it as insurance first, an investment second. This is where “buy term and invest the difference” became popular.

- Whole Life policies may have some cons and bad publicity, but many Fortune 500 companies purchase these policies every day.

Here is a Youtube Video that explains Whole Life Insurance better, and will help you visualize it as well.

- Term Life Insurance Quote

- Infographic – What Is Term Life Insurance?

- Infographic – How Does Term Life Insurance Work?

How Do I Choose a Life Insurance Policy? CBV: Cost – Benefit – Verbiage

This is the secret to buying life insurance, any type of insurance. Keep the process simple, and don’t over think it.

- First: Calculate how much life insurance coverage you need

- Second: How long do you need the life insurance coverage

- Third: Shop for a life insurance policy. if you have done the above two well, you do NOT NEED to work with a life insurance agent. You have already done the hard part, and that is determine the best policy and life coverage amount that you need. At this point, why be sold something that pays a better commission?

It will only take you a few minutes to get life insurance quotes. At a minimum, you will have the information you need to make a decision. Even better, you no longer procrastinate and sleep better tonight.

So back to the secret for how to buy life insurance… There is no magic. The life insurance premiums are set and each state regulates the insurance companies. This is not like buying a car, where you and your neighbor may pay completely different prices. The rates are fixed. So how do you get quotes that range in “price”?

- Cost

- Benefit

- Verbiage aka the details

You get to pick any two you want. The insurance company picks the third.

There are three parts to any insurance policy.

- “I want the best policy coverage for the cheapest amount”

No problem. We will give your beneficiaries ten million dollars when you die for a dollar a year of premium…

“that’s AWESOME, sign me up”

You didn’t let us finish. Ten million for a dollar a year. But you have to die April 1st. At 12:42 am while walking across this intersection. No other way.

“You’re kidding right”

That’s what you chose, isn’t it?

- “Well, I don’t want that. I want to make sure my benefit is there without any surprises in the fine print”

Ahhhh, so you are choosing the benefit and fine print. Okay, we will cover anything and everything, and pay your beneficiaries ten million dollars. That will cost you $500,000 a year

“WHAT!?!?!?”

You said you wanted the Rolls Royce plan didn’t you?

- “Okay, how do I balance all of this. This is more complicated than I thought“

That’s why I am here, with you. To help you figure this all out. Just remember the insurance company will always let you be in charge. You can pick ANY of the two, but they pick the third…

So prioritize right now. Which two do you want to pick! Are you on a tight budget? Is there a minimum amount of life coverage you feel you have to have? Do you want the best policy? What are you willing to give up of the three?

** Click here and get started immediately with life insurance quotes**

I. How much life coverage do you want?

II. How much additional life insurance coverage do you need?

III. How long or short do you want this life coverage to last, at minimum?

IV. How is your health? Height/weight? Do you smoke, or have you ever?

Have you already decided that you are curious about getting life insurance for yourself? if so, I highly suggest you head over to PolicyGenious and get quotes to compare prices and coverage. It’s a great no pressure way to start your research.

Compare prices among America’s top insurers with PolicyGenius Today

What Are The Other Types of Permanent Life Insurance Policies?

- Single Premium Life Insurance Policies:

- Universal Life Insurance Policies:

- Variable Life Insurance Policies:

- Variable Universal Life Insurance Policies:

Here you give a large lump sum of money to an insurance company, and you have life insurance for life. Typically the premium is much smaller than the life insurance benefit amount

This is like a whole life policy, except it has an added benefit of some flexibility. Flexible premiums and death benefits. You can change your coverage and your premiums over time, if necessary

This is where life insurance started to get a bit more complicated. People liked the idea of this little bundle of money building within their insurance policy. But didn’t like the idea of essentially investing in super safe investments over long periods of time. Some Variable universal life policies came out. Think of it as being able to add just a splash of spice to something that is ultra vanilla. The problem these policies had in the 1990’s were people invested in them with assumptions from the 1980’s – that were not exactly what came true. People who did not understand how these policies worked were not happy…

Have you ever wanted to have your cake and eat it too? This is the life insurance policy version of that. Mash them all together, and you have a VUL policy.

If you have ever heard the term “buy term and invest the difference”, this is the answer to that. The ability to invest your cash reserves like virtually any other portfolio with multiple choices. The danger here is if the investments don’t do well – your life insurance policy can literally run out of money.

Why Should I Buy Term Insurance?

- Term insurance will protect your family if you were to die for a set period of time.

- Term insurance is dirt cheap. For example, a 48 year old average healthy male non smoker can buy $500,000 of insurance for 20 years. For only about $100/m!!

- Younger healthier people are substantially cheaper.

- Renewable term life insurance – you can choose to lock in your rates for as long as you own the policy.

- Some term insurance policies will allow “convertibility” to a permanent policy. Sure your regular premiums would increase, but you may be able to change your mind in the future, even without having to prove you are still healthy. This is invaluable!

- Income tax free death benefits.

- The bottom line is term insurance is very cheap and protects your family. I will pay $x for y years, and if I die they will pay my family z dollars.

- Term insurance is temporary, after x years, you will no longer have life insurance coverage.

- In almost every single case, a term life insurance will expire without ever paying a death benefit. Call me crazy, but I consider that a pro.

- If your family never collects the death benefit, it is like rent. It is gone forever and you have nothing to show for it.

- You do not get to earn a cash value within your policy that may have tax advantages

- Very costly to renew the policy at the end of the policy. You are older, may be less healthy, etc.

Why Should I Buy Whole Life Insurance?

- You have a death benefit that is virtually guaranteed to be paid when you die, no matter when that is.

- You know how much you will pay in regular premiums without it going up. Other policies may offer flexible premiums.

- You will have a cushion of money in the cash reserves that will grow in a tax advantaged way that you can borrow from.

- Income tax free death benefits.

- Whole life insurance is wayyyy more expensive than term insurance. The same way buying a home is typically more expensive than renting.

- Do you really need an insurance policy forever? I can’t decide that, only you can. A majority of people feel they need life insurance until three main events in their life are achieved

- Their kids are finished with college

- They have reached retirement age and no longer need to save for retirement

- Their home mortgage is fully paid off.

Which is the best life insurance policy for you?

Which Life Insurance Should I Get?

There is no best life insurance policy for everyone. If there was, there would only be one kind of policy offered. Some say the best policy is the one that is in force on the day you die – but none of us can predict the future. That is why it’s is important to transfer the risk to an insurance company. Ask yourself some important questions, and the answer will be much simpler:

- How long do I think I need life insurance for?

Err on the side of caution, and go for the longest you are thinking about.

- How much additional life insurance benefits do you think you need?

Here is a great calculator to help with that.

- How much insurance do I WANT to have?

Maybe you feel more comfortable than having more than the minimum that you need. For many, the increase in cost is so much less than the increased peace of mind.

- How is your health? Do you smoke?

- How much extra money do you have to pay for life insurance premiums? A large lump sum today? A lot of extra income and you want to save money in the policy? You want to keep the regular premiums as low as possible?

(VGLI) Veterans Group Life Insurance – The Best Life Insurance Option for Veterans

By now you should have a good idea of which way you are leaning. If you are unsure at this point still – have your cake and eat it.

Consider applying for a term insurance policy that offers you the ability to lock in your rates and the ability to convert to a quality permanent insurance policy. Without having to prove your health down the road.

If you are still unsure about what to do: consider getting term insurance, period.

A vast majority of life insurance policies are term insurance. You can always cancel the policy if you change your mind. But if you don’t come home tonight, what financial protection will your family have without you?

GET COVERED TODAY, I cannot stress this enough.

Have you already decided that you are curious about getting life insurance for yourself? if so, I highly suggest you head over to PolicyGenious and get quotes to compare prices and coverage. It’s a great no pressure way to start your research.

Compare prices among America’s top insurers with PolicyGenius Today

How Do I Calculate How Much Life Insurance I Need?

“Calculating how much life insurance you need can be done by taking into account your current debts, future expenses, and any income replacement needs.”

Still want a better idea of exactly how much term insurance will cost you?

Good – that means you know what you want, and are ready to take action. DO NOT PROCRASTINATE ANY FURTHER.

Take just a few minutes and head over to the following calculator. If you have read this far – you clearly are curious as to how much life insurance you should have. Take a minute and visit

—> Click Her For a LIFE INSURANCE CALCULATOR <—

Did the number surprise you? Was it more or less than you expected it to be? Please comment below.

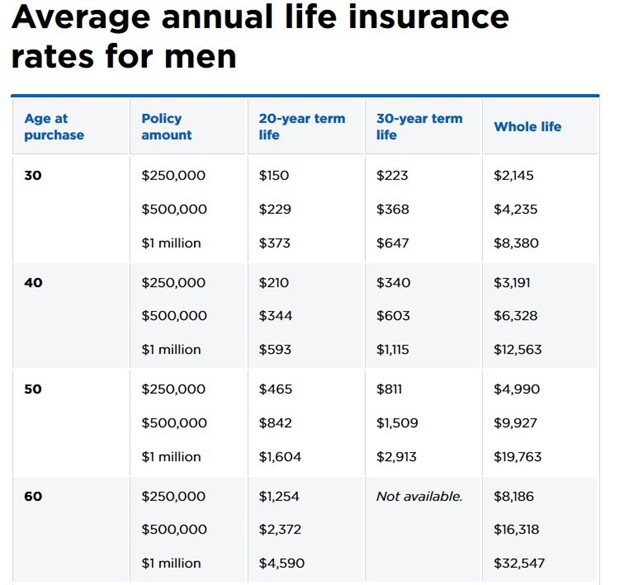

Best Life Insurance Rates – How Much Does Term Life Insurance Cost?

- It depends on your age, your health, whether you smoke, what state you live in, the specific insurance company you choose, if the rate is fixed and guaranteed, how much coverage you want, how long you want the coverage for. Here is a site that is absolutely amazing and takes what you put in and gives you a very good idea of how much a policy will cost you from a ton of different insurance companies. Do not assume how accurate this will be. Term4Sale.com

- Once you have a vague idea of the pricing, now you need to look at specific companies and get realistic quotes from them(CLICK HERE TO GET QUOTES).

The above two charts and the data can be found in a great article on a fantastic blog over at SBLI.COM

When Does Permanent Life Insurance Make More Sense Than Term Life Insurance Policies?

- When you expect your estate to be large enough to need life insurance as part of tax strategy. The federal estate and gift tax exemption increased to $15 million per individual ($30 million for married couples) in 2026 under the One Big Beautiful Bill Act, with permanent inflation indexing starting in 2027.

- When you know more about your health and family history than the insurance company does. If you are worried about your health declining in the future, a permanent policy may make more sense.

- There are times a business owner will want/need insurance, such as “Key Man Insurance”. This should be discussed with Financial Professionals: a Financial Coach such as myself or a Financial Advisor.

- If you are expecting a pension at retirement, there are strategies to use a permanent life insurance policy to maximize your pension payout

Retirement Savings Calculator – How Long Will My Money Last?

I hope this guide was helpful in some way. I cannot stress this enough if you have not done so already

- It is important to keep in mind that when you apply for life insurance coverage, you are not guaranteed to be approved. or approved at the premium you were expecting to pay. As part of your application for life insurance, there will be medical exams. Part of the medical exams are a health exam to check for any preexisting conditions and determine your life expectancy. You are always welcome to appeal the results of the medical exams.

- It is also import to consider the financial strength of life insurers when considering financial products and a life insurance program. I am not vouching for any of the following, but these are some of the more frequently companies people seek: Pacific Life Insurance company, Allianz Life Insurance company, Colonial Life Insurance company, Jackson National Life Insurance, Principal Life Insurance company, AETNA Life Insurance company.

- Life insurance and financial products are extremely important part of any comprehensive financial plan.

- Calculate how much life insurance you need

- Get a Quote ASAP

- Do NOT delay, accept the policy and get it in force TODAY

Have you already decided to get life insurance for yourself? if so, I highly suggest you head over to PolicyGenious and get quotes to compare prices and coverage. It’s a great no pressure way to start your research.

Compare prices among America’s top insurers with PolicyGenius Today

Next Steps

Getting the right life insurance coverage in place is one of the most important financial decisions you can make. To recap, we covered the key types of life insurance policies, factors to consider when choosing coverage, how to calculate the amount you need, and the main benefits of having a policy.

The key is working with a knowledgeable agent to select the right type of life insurance based on your budget, goals, and stage of life. Be sure to account for income replacement and future costs – not just immediate expenses. This ensures your loved ones are fully protected.

Life insurance provides crucial peace of mind knowing your family will be taken care of financially if something unexpected happens to you. It can help eliminate burdensome final costs while allowing your beneficiaries to maintain their standard of living.

Now that you’re armed with expert information, it’s time to take action. Reach out to me or schedule a consultation to discuss your specific needs and get personalized policy recommendations. I’m here to guide you every step of the way towards getting the ideal coverage.

To continue growing your financial knowledge, be sure to sign up for my exclusive newsletter below. You’ll get the latest tips and strategies directly from top experts to help you make smart money moves. I look forward to having you as part of my community!

What key takeaways resonated most with you in this life insurance guide? I encourage you to share your thoughts and questions in the comments section. And please spread the word by sharing this article – it could help someone you know gain financial security. Thank you for reading!

Frequently Asked Questions About Life Insurance

How much does term life insurance cost in 2026?

In 2026, a healthy 35-year-old can get $500,000 of 20-year term life insurance for approximately $25-40 per month for males and $20-35 per month for females. Costs vary based on age, health, smoking status, and coverage amount. Whole life insurance costs 15-20 times more for the same death benefit. Most people find term insurance significantly more affordable when they need income protection during their working years.

What is the difference between term and whole life insurance?

Term insurance is temporary coverage (typically 10, 20, or 30 years) that provides a death benefit if you die within that period. It’s very affordable and straightforward. Whole life insurance is permanent coverage that lasts your lifetime and builds cash value over time, like a savings account. Whole life costs 15-20 times more than term but guarantees a death benefit at any age. Most people use term for income replacement and buy whole life primarily for estate planning or when coverage is needed for life.

Do I need life insurance if I have no dependents?

Generally no, unless someone co-signed a loan with you or you want to cover final expenses (typically $7,000-$15,000). However, if you’re locking in rates while young and healthy for future needs, it can be smart. Many people buy a small amount of life insurance early as a safety net, then increase coverage when they have dependents or business obligations.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.