What parent doesn’t dream of a bright future for their child? As a personal financial planner for almost 30 years, I’ve sat with hundreds of Florida families who were planning for their kids college savings. And the conversation always turned to the same anxious question:

“How on earth are we going to afford college?” As a father of two who also lives in FL, I totally get it. The cost of saving for college can feel like a tidal wave building on the horizon.

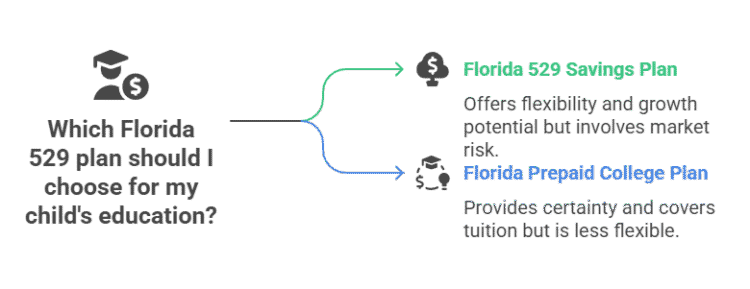

But Florida gives you two excellent life rafts: the Florida 529 Savings Plan and the Florida Prepaid College Plan. Choosing the right one is one of the most impactful financial decisions you can make for your child’s future. The problem is, they are fundamentally different. And picking the wrong one can be a costly mistake.

This guide will demystify clarify both options for you. We’ll go beyond the basics and into the real-world scenarios me and my clients faces as well.

- What happens if your kid gets the Bright Futures

- What happens if they decide to go to college out of state?

- We’ll cover the 2025 FAFSA changes

- And the powerful new 529-to-Roth IRA rollover rule.

Let’s build a clear, confident college savings plan together.

📌 Key Takeaways for 2025

- Florida’s Two Paths: The state offers two distinct 529 plans. The Savings Plan is a flexible investment account for nationwide use, while the Prepaid Plan locks in future tuition rates at Florida public colleges.

- No State Tax Deduction: Florida does not offer a state income tax deduction for contributing to a 529 plan, but you still benefit from tax-free growth and tax-free withdrawals for qualified expenses.

- New FAFSA Rules Help Grandparents: As of the 2024-2025 FAFSA, distributions from a grandparent-owned 529 plan no longer count as student income, making it a much more attractive way to gift for college.

- SECURE 2.0 Unlocks a New Exit Strategy: Unused 529 funds can now, under specific conditions, be rolled over into a Roth IRA for the beneficiary, providing a fantastic new safety net.

Key Takeaways Ahead

What Are Florida’s 529 Plans in 2025?

At its core, a 529 plan is a tax-advantaged account designed to encourage saving for future education costs. It’s named after Section 529 of the IRS code. The money you contribute can be invested, and any earnings grow federally tax-deferred. When you withdraw the money for qualified education expenses, the withdrawals are completely tax-free.

Florida is unique because it offers two powerful but very different types of 529 plans, both managed by the Florida Prepaid College Board.

| Feature | Florida 529 Savings Plan | Florida Prepaid College Plan |

|---|---|---|

| Core Concept | An investment account, similar to a 401(k), where your savings grow based on market performance. | A contract that locks in the future cost of tuition and most fees at Florida’s public colleges and universities. |

| Investment Risk | You bear the market risk. Your account value can go up or down. | No market risk for you. The plan is guaranteed by the State of Florida to cover its obligations. |

| Flexibility & Use | Extremely flexible. Can be used at any eligible college, university, or trade school in the U.S. and abroad for a wide range of expenses. | Less flexible. Designed for Florida public colleges. If used out-of-state, it pays a “transfer value” which may not cover the full cost. |

| Eligible Expenses | Tuition, fees, room & board, books, supplies, computers, and even some K-12 tuition and student loan repayment. | Primarily covers tuition and most mandatory fees. Dormitory plans can be purchased separately. |

| Michael’s Take | Best for families comfortable with market fluctuations who want maximum flexibility and growth potential. This is the superior choice if there’s any chance your child will attend an out-of-state or private college. | Best for risk-averse savers who are certain their child will attend a Florida public university. It offers peace of mind over growth potential. |

Who Is Involved with Florida 529 Plans?

Understanding the key players helps you navigate the system with confidence.

- The Florida Prepaid College Board:

This is the official state agency that administers both the Savings Plan and the Prepaid Plan. - The Account Owner:

That’s you. The parent, grandparent, or family member who opens and controls the account. - The Beneficiary:

This is the future student. Your child or grandchild. You can change the beneficiary to another eligible family member if needed. - The IRS:

The Internal Revenue Service sets the federal tax rules for all 529 plans, including what constitutes a qualified education expense and the penalties for non-qualified withdrawals. - The FAFSA Simplification Act:

This recent federal law changed how assets are treated for financial aid, significantly benefiting families who receive gifts from grandparents.

Why Do Florida 529 Plans Matter More Than Ever in 2025?

Saving for college has always been important, but recent changes have made the strategic use of a 529 plan more critical than ever.

💡 Michael Ryan Money Tip: A Tale of Two Clients

I had two clients, both doctors, who chose different paths. One, a surgeon, loved the certainty of the Prepaid Plan—he wanted tuition locked in, no questions asked. The other, a family physician, was comfortable with market risk and chose the Savings Plan for its flexibility and higher growth potential. There’s no single ‘best’ plan; there’s only the best plan for your family’s specific goals and risk tolerance.

The main driver is the skyrocketing cost of tuition. A 529 plan’s tax-free growth is one of the most powerful tools you have to combat education inflation.

In addition, the SECURE 2.0 Act has introduced a game changing new rule. Starting in 2024, you can roll over up to $35,000 in unused 529 funds into a Roth IRA for the beneficiary, subject to certain conditions. This provides an incredible safety net against the fear of over-saving.

Which Florida College Plan Fits You?

Answer three quick questions to get a personalized recommendation based on my 25 years of experience.

Recommendation: The Florida Prepaid Plan

You're a 'Safety Seeker' like my client Frank. You value predictability and guarantees above all else. The peace of mind from locking in tuition costs makes the Prepaid Plan a strong fit for you.

Recommendation: The "Secure the Core" Hybrid Strategy

You see the value in both safety and growth. Consider using a smaller Prepaid plan to guarantee a tuition floor, then use a 529 Savings Plan for flexibility and to cover all other costs. This is the strategy I recommend most often.

Recommendation: The Florida 529 Savings Plan

You're a 'Growth & Flexibility' planner like my client Stacie. You need a powerful tool that can cover all college costs at any school. The 529 Savings Plan is built for your goals.

How Do You Open and Fund a Florida 529 Plan?

Getting started is simpler than you think. Here’s the process I walked my clients through:

- Choose Your Plan:

Use the comparison table above to decide between the Savings Plan and the Prepaid Plan. This is your most important decision. - Go to the Official Website:

All applications are handled through the official Florida Prepaid College Board website, MyFloridaPrepaid.com. - Gather Your Information:

You’ll need your Social Security number or Taxpayer ID, as well as the same information for the beneficiary you are naming. - Fund the Account:

The Florida 529 Savings Plan has no minimum contribution, so you can start with any amount. You can then set up automatic monthly contributions from your bank account to make saving effortless.

What Are the Risks and Downsides of Florida’s 529 Plans?

While powerful, these plans aren’t without risks and limitations you need to understand.

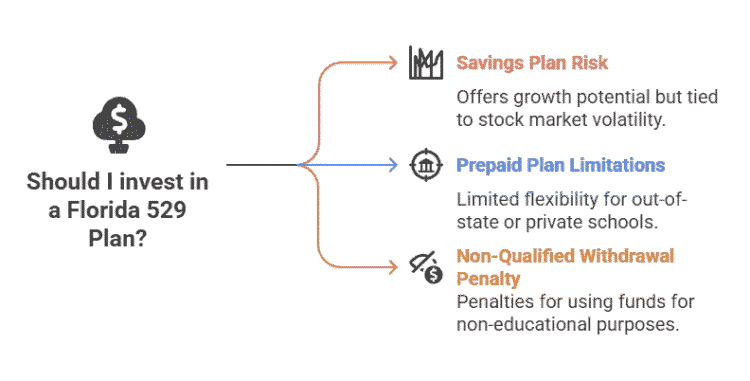

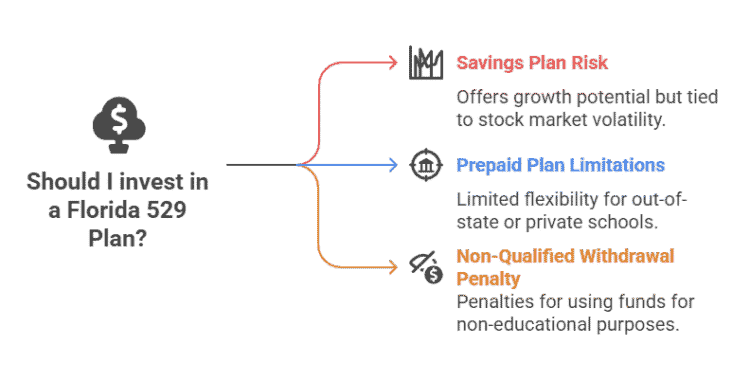

- Savings Plan Risk:

The value of your account is tied to the stock market. While this offers growth potential, your account value could be down when you need the money if you don’t manage your risk appropriately. - Prepaid Plan Limitations:

The biggest risk is the lack of flexibility. If your child chooses a private or out-of-state school, the plan only pays a transfer value, which is the average tuition at Florida’s public universities. This amount could be significantly less than the actual tuition bill, leaving you to cover a large gap. - Non-Qualified Withdrawal Penalty:

If you withdraw money for something other than a qualified education expense, the earnings portion of your withdrawal will be subject to both ordinary income tax and a 10% federal penalty.

Explore deeper topics to build a complete college funding plan. Now, try searching for: Roth IRA for college, financial aid, or student loans.

Frequently Asked Questions (FAQ) About 529 Plans in FL

Q: What happens to my Florida Prepaid plan if my child gets a scholarship?

A: This is one of the best features of the Prepaid Plan. If your child receives a scholarship, you can request a refund equal to the value of that scholarship from your plan, with no penalty. You can also use those funds to pay for other college expenses or transfer the plan to another eligible family member.

Q: Can I lose money in the Florida 529 Savings Plan?

A: Yes. The Savings Plan is an investment account, and its value is subject to market fluctuations. It is possible for the account balance to decrease. This is why choosing an investment portfolio that matches your time horizon is so critical.

Q: What is the new 529 to Roth IRA rollover rule?

A: The SECURE 2.0 Act introduced a powerful new option. You can now roll over a lifetime maximum of $35,000 from a 529 account to a Roth IRA for the same beneficiary. The 529 account must have been open for more than 15 years, and the rollovers are subject to annual Roth IRA contribution limits. This is an excellent way to handle leftover funds and give your child a jumpstart on their retirement savings.

Michael Ryan Money’s Final Take: The Best Plan is the One You Start Today

Choosing between the certainty of the Prepaid Plan and the flexibility of the Savings Plan is a major decision, but don’t let it lead to inaction. For most of the clients I advised, the Florida 529 Savings Plan was the superior choice simply because life is unpredictable. Kids change their minds, families move, and the flexibility to use the funds anywhere for any qualified expense is invaluable.

However, the truly “best” plan is the one you open and start funding. The power of tax-free compound growth is a gift you can only give your child by starting early.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.