You’re living on $994 a month from SSI (or maybe $1,491 if you’re married). The 2026 COLA bump helped, but barely. Then your car breaks down. $800 to fix it. Or your landlord hits you with a surprise $600 repair bill. The panic sets in. You’re not just looking for a loan. You’re looking for a lifeline. But some lifelines are anchors in disguise, built to drag you deeper into debt.

Let’s talk about disability loans for people like you, on disability benefits.

I spent 30 years as a financial planner watching predatory lenders target people on disability. The numbers are brutal. Research shows people with disabilities face poverty rates twice as high as those without disabilities. In some states, over 25% of adults with disabilities live below the poverty line. High-cost lenders know this. They see vulnerability as opportunity.

This guide puts 30 years of experience in your corner. We’ll evaluate every option, from grants to specialized loans, making sure you solve your emergency without creating a new one.

Key Takeaways Ahead

CRITICAL WARNING: How a Loan Can Affect Your SSI Benefits

Before you consider any loan, this is the most important rule you must understand.

If you receive Supplemental Security Income (SSI), you are subject to strict resource limits. As of 2026, the limit remains $2,000 for an individual and $3,000 for a couple. According to the Social Security Administration (SSA.gov), a resource is cash or anything you own that can be turned into cash.

⚠️ Safety Warning:

The money you receive from a loan is not considered income in the month you receive it. However, any loan money you have not spent by the first day of the following month will count as a resource. If that money pushes you over the resource limit, you could lose your monthly SSI benefits.

This does not apply to Social Security Disability Insurance (SSDI) recipients, who do not have resource limits.

The Financial First Aid Kit: Your Safest Path Forward

Instead of a simple list, let’s use a framework I gave all my clients:

The Financial First Aid Kit.

It organizes your options from safest and fastest (Layer 1) to last resort (Layer 3). We always check Layer 1 before even thinking about Layer 2.

- Layer 1: The ‘No-Debt’ Bandages (Grants & Aid)

- Layer 2: The ‘Community Capital’ Splint (Credit Unions & CDFIs)

- Layer 3: The ‘Surgical’ Option (Vetted Personal Loans)

Layer 1: Free Emergency Grants and Financial Assistance for Disability Recipients (2026)

Before taking on debt, always check for grants and local assistance programs. This is money you do not have to pay back.

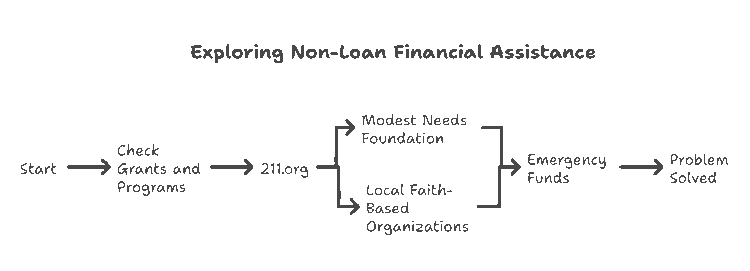

211.org:

This is your best starting point. Run by the United Way, 211.org is a free, confidential service that can connect you to local assistance programs in your area for everything from utility bills and rent to medical costs and food.

You can call “211” on your phone or visit their website. When you call, be sure to ask about specific programs in your city or county, such as the Low Income Home Energy Assistance Program (LIHEAP) for help with heating and cooling bills.

Modest Needs Foundation:

This organization offers small, short-term grants to individuals and families in temporary crisis.

Local Faith-Based Organizations and Charities:

Churches, the Salvation Army, and other local charities often have emergency funds available to help community members.

I once had a client, Jane, who was facing a $500 utility shut-off notice. Instead of a risky loan, we called 211 together. They connected her to a local church’s emergency fund that paid the bill directly. She cried with relief. No new debt, just a problem solved. This path works.

Layer 2: Consider Safer Loan Alternatives

In my practice, this is the step where we find the most empowering solutions for my clients. Options that build financial health rather than destroy it. If grants and local aid are not enough, your next stop should be a credit union or a Community Development Financial Institution (CDFI).

Payday Alternative Loans (PALs) from Credit Unions

Inside the world of ethical finance, Payday Alternative Loans (PALs) are the industry’s best-kept secret for borrowers with shaky credit. According to the National Credit Union Administration (NCUA.gov), PALs have key protections:

- Loan amounts: Typically between $200 and $2,000.

- Repayment terms: Longer terms, from 1 to 12 months.

- Interest rates: Capped at 28% APR, which is significantly lower than the 400%+ APR of payday loans.

In early 2026, I walked a client on SSDI named Carlos through this exact process. He needed $800 for a dental emergency and thought his 580 credit score doomed him. Instead, we found a local credit union offering PAL II, an often-overlooked variant that allows immediate loan access upon joining.

The one-month membership rule for standard PALs isn’t a bug; it’s a feature designed to encourage a banking relationship, not a one-off transaction.

⚠️ Myth Busted: “Credit unions won’t approve someone on disability.”

Reality: Credit unions often serve members that traditional banks reject. Your SSDI or SSI counts as steady income. Many credit unions specialize in serving people with disabilities and offer financial counseling. Navy Federal, Alliant, and Pentagon Federal all have robust PAL programs. The key is finding a credit union with a mission aligned with financial inclusion.

Loans from Community Development Financial Institutions (CDFIs)

CDFIs are mission-driven lenders certified by the U.S. Treasury that provide fair, affordable loans to people in underserved communities. They often have more flexible lending criteria than traditional banks. Major CDFIs serving people on disability in 2026 include Grameen America, LiftFund, Capital Good Fund, and Self-Help Credit Union. You can find a certified CDFI in your area using the official CDFI Fund search tool.

Layer 3: If You Must Get a Personal Loan, Understand the Process

If you cannot secure a PAL or CDFI loan, you may need to apply for a traditional personal loan. Lenders will primarily look at two factors:

Your Income:

Your disability benefits (both SSI and SSDI) absolutely count as income. Lenders want to see a steady, reliable source of funds to ensure you can make payments.

Your Credit History:

A lower credit score will likely result in a higher interest rate. For example, in 2026, a borrower with fair credit (630-689) might see APRs from 18-25%, while a borrower with poor credit (below 630) could face rates of 28-36% or higher on a legitimate personal loan.

Building a positive credit history is crucial, and you can start by reading our guide to credit utilization.

Predatory Loans to Avoid in 2026: Payday, Title, and No-Credit-Check Traps

Now we enter what I call the danger zone. I’ve seen these products devastate families, and I urge you to avoid them at all costs. Welcome to the debt-trap arcade.

Payday Loans:

These aren’t loans; they’re financial quicksand. The Consumer Financial Protection Bureau (CFPB) has data showing nearly 70% of borrowers take out a second payday loan within a month. The business model is the cycle of re-borrowing, what insiders call the “debt treadmill.”

Car Title Loans:

These are even more insidious, leveraging a critical asset—your mobility—against you. I’ve seen clients lose their only means of getting to a doctor’s appointment over a sub-$1,000 loan.

No-Credit-Check Installment Loans:

The danger here isn’t just the high interest rate; it’s the loan’s structure, which is often engineered for default.

What If You Don’t Qualify? Other Paths to Explore

- Negotiate with Creditors:

Call the hospital, utility company, or landlord directly. Explain your situation and ask for a payment plan or a temporary reduction. Many will work with you to avoid collections. - Local Community Action Agencies:

These non-profits often have specific funds for emergency repairs or utility assistance that are separate from 211. Search for “[Your County] Community Action Agency”. - Selling Unused Items:

Platforms like Facebook Marketplace can provide a quick, debt-free source of cash for items you no longer need.

Frequently Asked Questions (FAQ)

Can I get a loan with bad credit?

Yes, but your focus should be squarely on Layer 2: PALs from credit unions and loans from CDFIs. They are designed to serve individuals with non-traditional income and imperfect credit.

What about a co-signer?

I’m asked about co-signers constantly. Here’s my direct advice: treat it like surgery. It can save you, but it’s a serious procedure with risks for everyone involved. I once saw a grandmother co-sign for a $2,000 loan that spiraled, putting her own Social Security at risk of garnishment.

Before you ask someone to co-sign, you must be able to hand them a written budget showing exactly how you’ll make every single payment.

For more on this, read our guide on services like Leap Guarantor.

Can my federal student loans be forgiven due to disability?

Yes. If you have a total and permanent disability, you may be eligible for a Total and Permanent Disability (TPD) Discharge. This is a separate federal process that erases your student loan debt entirely. This is a powerful form of financial relief you should explore before considering any new loans.

Can I get an emergency loan on the same day?

While some online lenders promise same-day funding, these are often the high-risk loans we advise against. The safest options, like a PAL from a credit union, may take a few business days but will save you from potential debt traps. Calling 211 for local aid can sometimes result in same-day assistance.

Are there specific loans for buying medical equipment?

Yes, beyond grants, some CDFIs and non-profits specialize in loans for assistive technology or medical devices. Check with your state’s Assistive Technology Act Program for resources.

Your Final Takeaway: A Path to Financial Safety

When facing a financial crisis on a fixed income, your first move determines everything. Don’t let a moment of panic lead you to a high-cost lender.

Your Financial Safety Path:

🆘 Emergency?

➡️ Step 1: GRANTS (Call 211, Check Charities)

If more is needed…

➡️ Step 2: SAFE LOANS (Credit Union PALs, CDFIs)

Last resort…

➡️ Step 3: CAREFUL LOANS (Vetted Personal Loans)

🚫 AVOID: Payday, Title, & “No-Credit-Check” Loans

Start with the safest options first. By following this path, you protect not only your wallet but also your peace of mind. You have the right to be treated fairly, and now you have the knowledge to demand it.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.