You’ve found it. The perfect apartment. One bedroom, $2,200 a month, 15-minute subway ride to campus. Location? Perfect. Rent? You can swing it. Then you read the fine print on the landlord’s application: “Co-signer required. FICO score 700+. Annual income must be 80 times monthly rent.” That’s $176,000 a year. Your parents either don’t hit that number, or they’re in another country and can’t sign U.S. paperwork. Sound familiar?

This scenario plays out thousands of times a day across America. College kids with zero W-2 history. International grad students on F-1 visas with no U.S. credit file. First-year tech workers pulling down $70,000 in San Francisco or New York (which doesn’t come close to landlords’ 80x income formulas, even though they can absolutely afford the rent). In 2026’s rental market, where vacancy rates in hot neighborhoods sit under 3%, this documentation gap isn’t just frustrating. It’s an automatic rejection.

Until recently, this created a binary outcome: find a parent or close relative willing to co-sign, or walk away from the apartment. But between 2022 and 2026, specialized guarantor companies—operating as insurance underwriters rather than individual co-signers—have built platforms that assess risk algorithmically, issue binding lease-endorsement certificates within hours, and charge applicants a one-time premium instead of requiring a personal relationship.

Among these services, Leap has emerged as the market leader, processing over 50,000 applications annually as of 2026 and maintaining direct API integrations with property management systems like Yardi and RealPage that serve approximately 4 million rental units across the U.S.

As a financial planner who has tracked these products since their 2018 launch, I’ve watched guarantor services convert applications that landlords flagged as “automatic no”—FICO scores between 650–680, debt-to-income ratios above 43%, or foreign credit histories with no U.S. reporting—into approved leases within 18 to 36 hours. The central question for applicants in 2026 is whether the one-time premium (typically $1,400–$2,400 for a 12-month lease on a $2,000/month unit) functions as a legitimate risk-transfer tool or simply extracts fees from people who lack alternatives.

The Contrarian Reality: Why Guarantor Services Expose a Broken System

Okay, real talk. Most articles about Leap won’t tell you this: these services aren’t solving YOUR problem. They’re solving a landlord screening problem that shouldn’t exist in the first place, and making you pay for it.

Here’s the thing. A nurse pulling $72,000 a year can easily cover $1,800/month in rent. That’s 30% of her gross income (the standard HUD recommends). But she gets rejected because landlords demand 80 times the monthly rent in annual income. That means she’d need to earn $144,000. Meanwhile, Verified Market Research shows the guarantor market exploding from $705 million in 2024 to $1.53 billion by 2032. Why? Not because renters became less responsible. Because landlord screening formulas are stuck in 1985.

Think about it. These income multipliers (40x to 80x monthly rent) were created before Experian even existed, when verifying income meant calling someone’s boss. Now we’re in 2026. Banks use Plaid to see your checking account in real time. Property managers can track ACH payments automatically. AI can predict payment behavior with scary accuracy. But landlords still require a renter to earn $160,000 to lease a $2,000 apartment. That’s not risk management. That’s security theater that created a $1.5 billion business opportunity for insurance companies.

Equity advocates have documented how these formulas particularly harm Housing Choice Voucher holders: landlords often require voucher recipients to meet income thresholds based on full market rent rather than their actual payment obligation (typically 30% of income), effectively screening out the very population the voucher program was designed to serve. This practice is now illegal in jurisdictions with source-of-income discrimination protections, yet the underlying philosophy—judging tenants by earnings multiples rather than cash flow analysis—remains standard industry practice.

Here’s what you need to know about Leap: how it works, what it’ll cost you, and whether it’s worth the money.

The Renter’s Dilemma: When Do You Need a Guarantor Service?

In 2026’s rental market, institutional landlords and property management firms aim to cap financial exposure by imposing screening thresholds that many otherwise-qualified applicants cannot meet. Common requirements include a FICO score of at least 650–700, verifiable monthly gross income equal to 40–80 times the monthly rent (meaning a $2,000/month apartment demands proof of $80,000–$160,000 annual income), and a clean eviction record searchable through national tenant-screening databases like TransUnion SmartMove or RentGrow.

If you don’t meet these rental criteria, you need a guarantor. You typically need a service like Leap Guarantor if you are:

- A college undergraduate or graduate student with no full-time employment history, no credit cards, and either a thin credit file (FICO below 650) or no scoreable credit report at all.

- An international graduate student, postdoctoral researcher, or tech professional on an H-1B, F-1, or J-1 visa who holds no U.S. credit file, cannot produce a Social Security Number-linked credit report, and whose only proof of funds is a foreign bank statement or fellowship award letter.

- A first-year professional (software engineer, nurse, consultant, attorney) earning $60,000–$85,000 gross who cannot meet an 80x income threshold for units priced above $1,000/month in high-cost metros, even though the monthly rent represents less than 30% of take-home pay.

- A self-employed freelancer, gig worker, or 1099 contractor (graphic designer, rideshare driver, Etsy seller) whose 2025 Schedule C shows $48,000 net profit but whose month-to-month cash flow varies between $2,500 and $6,500, making it difficult to demonstrate stable income on a standard two-paycheck verification form—a scenario we detail in our guide to money management for freelancers.

💡 Michael Ryan Money Tip

Before paying for a guarantor service, ask the landlord if they would accept a larger security deposit instead (e.g., two months’ rent). Some landlords prefer the simplicity of holding cash over dealing with a third-party insurer. It never hurts to ask, and it could save you hundreds. For more on this, check our guide on what to do if you don’t make 3 times the rent.

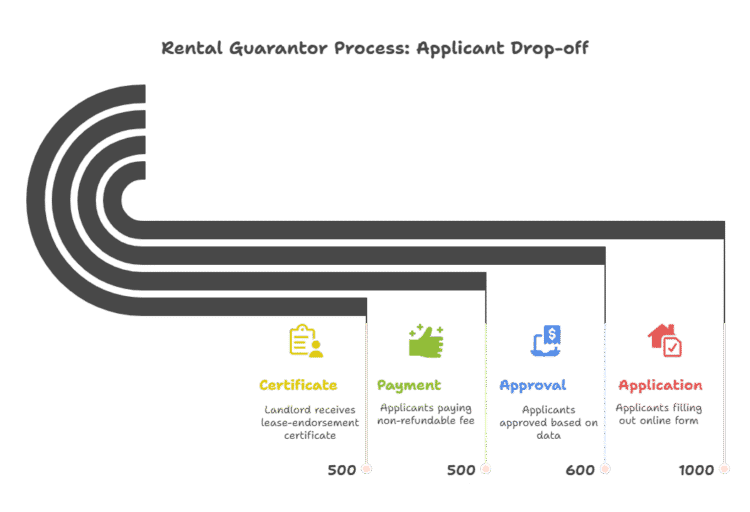

The “Leap of Faith”: How the Rental Guarantor Process Really Unfolds

Leap operates not as a personal co-signer who evaluates your character, but as an actuarial insurer who prices your default risk using proprietary algorithms trained on millions of lease outcomes. In 2026, the typical approval workflow runs through three automated checkpoints, each designed to minimize human delay while maximizing underwriting precision.

Digital Underwriting:

You’ll fill out their online application, which feeds your data into their proprietary decisioning model.

A key point: Leap often integrates directly with property management software like Yardi or RealPage, which is why the approval can feel so seamless.

Last year, I had a client (freelance UX designer, $72K annually) with a FICO score of 668. Just two points under the landlord’s 680 cutoff. The Yardi system flagged her as pre-approved for Leap in 90 seconds. She uploaded two months of Chase statements showing steady $6,000 deposits, and Leap spit out a binding certificate in 22 minutes.

The Risk-Based Fee:

If you’re approved, you’ll be presented with a non-refundable fee.

Here’s an insight: This fee is your personal “risk score” turned into a dollar amount. It’s calculated based on your specific application,

I expect these companies will start offering “good renter discounts” on lease renewals (like car insurance gives you for clean driving records). Pay on time for 12 months, get 15-20% off your next Leap fee.

The Digital Handshake:

Once you pay, Leap issues a Lease-Endorsement Certificate directly to the landlord. This isn’t just a promise; it’s a legally binding insurance document.

Is this process a “black box”? A little. But is it effective at turning a “no” into a “yes” in under an hour? Absolutely.

The True Cost: A Calculated Fee vs. a Relational Favor

The fee from Leap (and others) is a one-time, non-refundable insurance premium. It’s the cost of transferring the landlord’s risk from your parents to a corporation.

Look, this isn’t cheap. A $2,000/month apartment? You’re looking at $1,500 to $2,200 in Leap fees.

But what’s the alternative? Asking a parent to co-sign isn’t free; it just has a different currency. It costs them a hard inquiry on their credit report and adds a potential $24,000 contingent liability to their name that could impact their own ability to get a mortgage.

In mid-2024, I worked with a 26-year-old software engineer in Seattle whose parents held a $420,000 mortgage balance at 6.75% and were actively shopping for refinance quotes. Co-signing their son’s $1,850/month lease would have added a $22,200 annual contingent liability to their debt profile, pushing their back-end debt-to-income ratio from 38% to 42%—just high enough to disqualify them from the best 30-year fixed rates. We chose Leap’s $1,620 premium instead; his parents refinanced three months later at 6.125%, saving roughly $230/month over the life of their loan.

Which cost is truly higher?

The Hidden Asymmetry: Why Guarantor Services Favor Landlords, Not Tenants

Nobody at Leap will tell you this: that $1,620 premium protects the landlord’s cash flow, not your creditworthiness. You still owe every cent of rent plus late fees if you can’t pay. The premium just eliminates the landlord’s risk and legal headaches.

In a traditional default scenario, a landlord must initiate eviction proceedings (average cost: $3,500 in legal fees, 30–90 days to vacate), chase collections, and absorb lost rent during turnover. With Leap’s guarantee, the landlord receives payment within 30 days of default while you remain on the hook for the full balance plus Leap’s recovery fees, which can include 18–24% annual interest on unpaid amounts.

This explains why property management companies increasingly require guarantor services even for applicants with borderline-acceptable credit (FICO 660–690): the premium transfers default risk from the landlord’s P&L to the tenant’s personal balance sheet while converting a potential 90-day vacancy loss into a 30-day insurance claim. For large property managers operating on 6–8% net margins, guarantor requirements function as an insurance policy they don’t pay for—you do.

The Fine Print: Key Risks and What Happens if You Default

Using a guarantor service does not absolve you of your responsibilities. If you fail to pay your rent (rent default), Leap will pay the landlord on your behalf to satisfy the guarantee. However, you will then owe that money directly to Leap.

Failure to repay Leap can result in collections activity and negatively impact your credit history.

It is crucial to understand your rights and responsibilities as a tenant, which you can review on the U.S. Department of Housing and Urban Development (HUD) website.

Is Leap Guarantor Legit? A Look at the Company and Its Alternatives

Yes, Leap is a legitimate company. It is a licensed Leap Insurance Agency, and its policies are underwritten by insurers with strong financial strength ratings from A.M. Best. However, they are not the only player in this space.

Other reputable guarantor services include:

- Insurent: Widely used, particularly in major East Coast cities.

- TheGuarantors: Offers both lease guarantees and security deposit replacement products.

Apartment Guarantor Frequently Asked Questions

Does Leap cover my security deposit?

Typically, no. The standard Leap Guarantor service guarantees your fulfillment of the lease terms (i.e., paying rent). You are usually still responsible for paying the traditional security deposit directly to the landlord. Some providers, like TheGuarantors, offer a separate **security deposit alternative** product for an additional fee.

Can I use a Guarantor for a lease renewal?

Maybe. This depends on the specific policy and the landlord. Some guarantor policies cover only the initial lease term. If you need to renew, you may have to re-apply and potentially pay a new fee. Always clarify this before signing up.

Is a Guarantor a co-signer?

Functionally, yes, but technically, it’s an institutional guarantor. Instead of a person with a high credit score signing your lease, it’s an insurance company backing your lease. This is often preferred by large property management companies as it’s a more formal and reliable financial arrangement.

Bottom Line: Is Leap Worth It?

Leap works. These services have rescued thousands of renters who’d otherwise get locked out of competitive markets. They’re legit alternatives to traditional co-signers for students, international renters, and anyone with thin credit. But you’re paying real money ($1,500 to $2,200 isn’t pocket change) for what amounts to an insurance policy the landlord benefits from more than you do.

Is it worth it? If it’s the only thing standing between you and a safe, desirable apartment in a tough market, then yes. But always explore all your options first.

What to Read Next

Now that you know how to get your application approved, are you prepared for the financial responsibilities of renting?

- ➡️ Read Our Guide: How to Create a Budget That Actually Works

- What If I Don’t Make 3 Times The Rent?

- Disability Loans For People on Disability Benefits

- Is Rapid Address Change Legit or Scam?

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.