On March 12, 2024, I sat across from Karen, who’d just trusted me with her retirement plan for the tenth time. When she blanched at ‘Grid Code G’ on her Equifax printout. It wasn’t just letters; it was her home-equity line in someone else’s hands. Here’s a harsh truth: your credit score isn’t broken. It may be under siege.

Ready to fight back?

Don’t let jargon scare you. Think of Grid Code G as a neon sign flashing ‘debt in progress.’ In my near 30 years of coaching high-net-worth families and folks just starting out, I’ve learned how to turn that neon sign into a road sign pointing straight to resolution.

This isn’t just about a code. It’s about money. Back on October 3, 2022, the CFPB docketed its 150,345th ‘we don’t owe this!’ complaint. The highest monthly spike since 2019. Last month alone, one Maryland family I consulted with reversed a $9,450 Grid G entry after proving a simple billing‐cycle glitch.

What could that kind of money do for your financial plan?

This is your battle plan. We will walk through the four exact steps to validate, dispute, and delete this entry for good.

Key Takeaways Ahead

First, Don’t Panic: What Grid Code G Really Means

Contrary to popular belief, ‘Grid Code G’ isn’t a mysterious penalty from the credit bureaus. It’s Experian’s internal shorthand for “we’ve passed this debt to someone else.”

Think of Grid Code G as just a file-folder label inside Experian’s system. It simply means a collection agency now holds the debt, not your original creditor. Your goal isn’t to fight the “code,” it’s to challenge the “collection account” inside that folder.

I saw it firsthand in November 2023, when Encore Capital (the parent of Midland Credit Management) sent a letter about a $3,200 medical bill in my client Raj’s name. The hospital had sold his debt to them on the auction block for about 4 cents on the dollar.

Now for the surprise question: why would a company buy your debt for pennies yet have the right to demand the full value from you?

Because that’s their business model. And understanding that is the key to beating them.

The Grid Code G is simply the flag on your report that shows this transaction has happened. It means an original creditor (like a hospital, credit card company, or cell phone provider) has given up and sold your account to a third-party collection agency.

The Companies Behind the Code: Who Is Reporting This?

⚠️ Myth Busted: You’re staring at your credit report at a company name like “Midland Credit Management” or “Portfolio Recovery Associates” and thinking, “I’ve never done business with them!” You’re right. You haven’t.

These companies are debt purchasers. They are the most common entities associated with a Grid Code G. They are not the original bank or hospital you owed money to.

(e.g., Capital One, Chase, Verizon)

(e.g., MCM, PRA)

Their entire business is to buy old, written-off debt and then try to collect on it. Knowing you are dealing with a debt purchaser, and not your original creditor, is a critical piece of leverage you will use in the steps below.

Debt purchasers like MCM and PRA handle millions of accounts and often have minimal documentation on hand when they first acquire a debt. This is why sending a debt validation letter immediately is so effective. You are legally forcing them to stop and dig for paperwork they may not easily find.

Your 4-Step Triage Plan to Remove Grid Code G

Alright, enough theory. This is the exact, step-by-step process I use with clients to turn defense into offense. Follow it precisely.

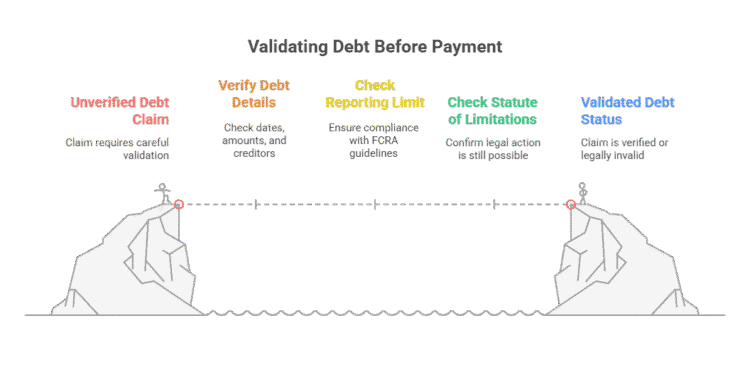

Step 1: Confirm the Debt is Valid (The “Prove It” Step)

Before you do anything else—especially before you even think about paying—your first job is to become a financial detective. My client, Stephanie, was panicked when a Grid Code G blocked her from getting a car loan. Her first instinct was to pay the $1,200 collection to make it go away.

I stopped her cold. “Not so fast,” I said. “First, we make them prove it’s even yours.”

- Check the Dates:

Pull your full credit report from Experian or get your FICO Score. Find the “Date of First Delinquency.” If that date is more than 7 years ago, the account is legally obsolete and must be removed under the Fair Credit Reporting Act (FCRA). - Check the Statute of Limitations:

This is different from the 7-year reporting limit. The statute of limitations is the time limit a collector has to sue you. The debt statute of limitations varies by state (usually 3-6 years). If a debt is past the statute of limitations, they can’t win a judgment against you.

Your First Action Step: Find the entry on all three of your credit reports. Note the original creditor, the date of first delinquency, and the balance.

Step 2: Send a Formal Debt Validation Letter (Your Legal Shield)

This is your single most powerful weapon. Under the Fair Debt Collection Practices Act (FDCPA), you have the legal right to demand a collection agency provide proof that you owe the debt and that they own it. This is not a request; it’s a demand.

You must send this letter within 30 days of the collector’s first contact with you. Doing so forces them to cease all collection activities until they provide validation.

Your First Action Step:

Write a simple debt validation letter. Do not admit the debt is yours. Do not offer to pay. Simply state you are disputing the debt and demand they provide proof of the original signed contract, their authority to collect, and a full accounting.

💡 Michael Ryan Money Tip:

Send this letter via USPS Certified Mail with a return receipt. This is non-negotiable. It costs about $8, and that receipt is your legal proof they received your demand. It’s the best money you’ll ever spend in this fight.

🚀 Next Steps: Want a head start? Don’t leave anything to chance.

Download our free, attorney-reviewed Debt Validation Letter Template to ensure you get it right.

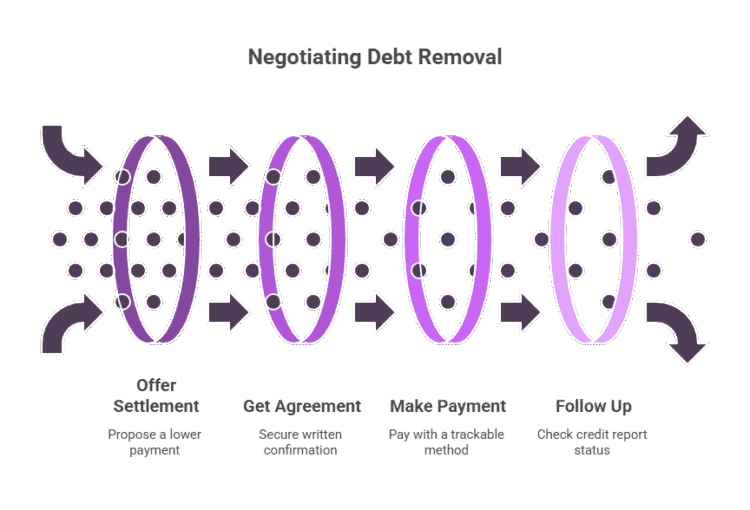

Step 3: Negotiate a “Pay for Delete” (If the Debt is Valid)

Let’s say they send back proof, and the debt is yours. It’s recent, and it’s accurate. Do not just send a check. Paying a collection in full does not remove it from your report; it just changes the status to “Paid Collection,” which still hurts your score.

Your goal is a “pay for delete.”

This is a written negotiation where you offer to pay a certain amount. Often a settlement for less than the full balance. In exchange for their explicit agreement to completely remove the entire collection tradeline from all three credit bureaus.

Here’s the playbook:

- Start Low: Offer to settle for 40% of the balance.

- Get It In Writing: This is the most important rule. Never, ever send a payment until you have a signed letter or email from them agreeing to the specific “pay for delete” terms.

- Pay with a Trackable Method: Use a cashier’s check or a method that doesn’t give them direct access to your bank account.

- Follow Up: Check your credit reports 30-45 days later. If the account isn’t gone, send them a copy of your agreement and your proof of payment.

Step 4: Dispute Directly with the Credit Bureaus

This is your final move if the collection agency plays games. You file a formal dispute with Experian, Equifax, and TransUnion under two conditions:

- They fail to respond to your debt validation letter within the 30-day legal window.

- They send “proof” that is weak or insufficient (e.g., just a spreadsheet printout).

In your dispute, you will state that the furnisher (the collection agency) failed to provide validation of the debt as required by the FDCPA, and therefore the account is unverified and must be removed under the FCRA.

Experian Dispute

experian.com/disputes/

Equifax Dispute

equifax.com/personal/credit-report-services/credit-dispute/

TransUnion Dispute

transunion.com/credit-disputes/dispute-your-credit

By following these four steps, you move from a position of weakness and confusion to one of legal strength and control.

Michael Ryan Money Readers Frequently Asked Questions (FAQ)

What if the collector ignores my debt validation letter?

If they don’t respond within 30 days, they have violated the FDCPA. You should immediately file a dispute with all three credit bureaus, stating that the debt is unverified. Also, file a complaint with the CFPB Consumer Complaint Database.

Does paying the collection automatically remove Grid Code G?

No. Paying the debt only changes the status to “Paid.” The negative collection entry, including the code, remains for up to seven years. The only way to guarantee its removal is with a successful dispute or a written “pay for delete” agreement.

How is the Statute of Limitations different from the 7-year credit reporting limit?

The 7-year reporting limit is set by federal law (the FCRA) and dictates how long most negative items can stay on your credit report. The Statute of Limitations is a state law that dictates how long a creditor has to sue you in court. A debt can be too old to sue you for but still new enough to be on your credit report.

Is Grid Code G the only collection code?

No, each bureau has its own coding system. For example, you might see codes like “CO” for charge-off or other specific collection identifiers. Grid Code G is most famously associated with Experian and major debt purchasers.

Your Next Move: From Grid Code G to Control

So, as we’ve covered, Grid Code G isn’t some universal mark of doom. It’s a specific label, most famously used by Experian, for a collection account that’s been handed off to a major debt purchaser. Knowing this explains the problem; it turns a monster in the dark into a specific opponent with a specific set of rules.

The key takeaway from our battle plan isn’t memorizing codes; it’s mastering the playbook. The debt validation letter is your legal shield. The “pay for delete” negotiation is your strategic leverage. And a direct credit bureau dispute is your final checkmate.

These aren’t just administrative chores; they are your rights under the FDCPA and FCRA. Tackling this collection account is about more than just erasing one negative line item. It’s about proving to yourself, and to the financial world, that you are in control of your financial narrative. This single action is a powerful step in your credit repair journey, directly impacting your credit score and your ability to secure the loans you need for the life you want to build.

You now have the knowledge and the framework to fight back effectively. Your financial journey doesn’t end here; it’s just getting started. Your First Action Step: If you found this battle plan useful, sign up for my weekly ‘Money Minutes’ newsletter. It’s packed with more no-nonsense advice for mastering your credit, building wealth, and cutting through the noise Wall Street loves to create.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.