You get a text message, supposedly from your bank: “Suspicious activity on your account. Click here to verify.” Your heart is pounding. Is this real or a credit card scam? Is your money at risk? That single moment of fear and uncertainty is exactly what credit card scammers are banking on.

Have you just been a victim of a credit card scam? What do you do now? How do you protect yourself?

Let’s be brutally honest: the game has changed. These criminals aren’t just after your card number anymore; they’re after your emotional triggers. According to the 2025 Federal Trade Commission’s latest annual data, consumers reported losing a staggering $12.5 billion to fraud in 2024. That’s a 25% jump from the previous year.

Most people think the biggest danger of credit card fraud is losing money. It’s not. The real cost is your time and the soul-crushing stress of untangling the mess, which can take weeks or months. For over 25 years, I’ve seen smart people fall for these schemes because modern scams aren’t designed to fool a computer; they’re designed to fool a human.

This guide is your defense manual against being defrauding by credit card scammers.

- First, I’m going to calm your biggest fear by showing you how protected you actually are.

- Then, I’ll expose the 7 most common credit card scams by dissecting the psychological tricks they use to work.

- Finally, I’ll give you a rock-solid action plan for both prevention and damage control.

Key Takeaways Ahead

First, The Good News: Your Money is Actually (Mostly) Safe

Before we dive into the credit card scams, let’s get this out of the way.

If a scammer does get your credit card number and makes fraudulent charges, you are almost certainly not responsible for paying for it.

Thanks to strong credit card consumer protection laws and policies, your wallet has a powerful shield.

💡 Michael Ryan Money Tip

The single most important factor for zero liability is speed. The faster you report a lost card or a fraudulent charge to your bank, the stronger your case and the quicker the resolution. Don’t wait even a single day.

- The Law is On Your Side:

The Fair Credit Billing Act (FCBA) is a federal law that legally limits your liability for unauthorized credit card charges to a maximum of $50. - Card Networks Go Further:

The major card networks (Visa, Mastercard, American Express, and Discover) have all implemented “zero liability” policies. This means that as long as you report the fraud in a timely manner, you are responsible for $0 of the fraudulent charges.

This is your safety net. Now, let’s make sure you never have to use it.

The Scammer’s Playbook: How They Bypass Security by Targeting You

Your credit card’s EMV chip and contactless payment features create a powerful digital lock. It’s incredibly difficult for a scammer to break that lock directly. So, they don’t even try. Instead, they focus on tricking you into handing them the key.

This is called social engineering. The art of manipulating human psychology to bypass security. Think of your EMV chip as a strong front door lock. Social engineering is the scammer, dressed as a friendly delivery person, convincing you to open the door and invite them right in.

They do this by exploiting a few core human emotions:

- Fear: “Your account has been compromised!”

- Urgency: “You must act within the next 15 minutes!”

- Authority: “This is Agent Smith from the bank’s fraud department.”

- Greed: “Click here to claim your free $500 gift card!”

Once you understand their playbook, that scammers use a stopwatch because they know their lies can’t survive scrutiny, you can see their plays coming a mile away.

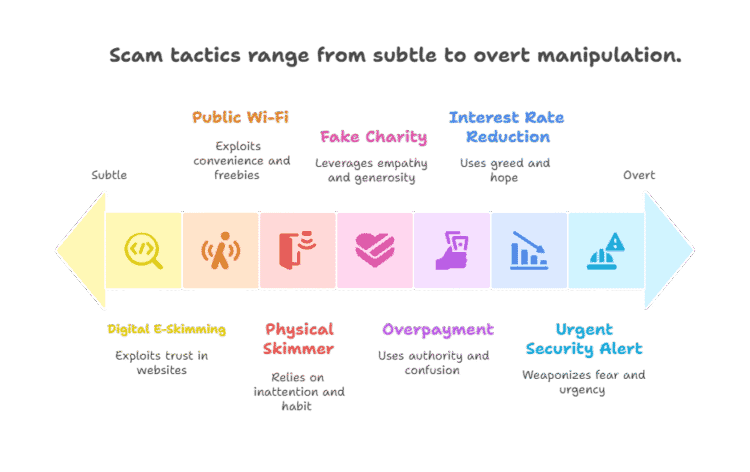

Scam #1: The “Urgent Security Alert” Imposter

This is the most common and effective scam today, hitting you through text, email, or phone calls.

- How it Works: You receive a text message pretending to be from a trusted entity (your bank, Amazon, Best Buy, or even the IRS). It claims there’s a problem with your account, a suspicious charge, or a package that can’t be delivered. The message always contains a link or a phone number for you to “verify” your information.

- The Psychological Trick: This scam weaponizes Fear and Urgency.

- The Variations:

- Smishing: An attack via SMS text message.

- Phishing: An attack via a fraudulent email.

- Vishing: An attack via a voice phone call (often a robocall).

📌 Key Takeaway

Don’t take the bait. Your bank will never text or email you a link to solve a problem. Any legitimate alert will simply advise you to log into your account through their official app or website.

Your Defense Plan:

- Never click the link. Never call the number in the message.

- If you’re concerned the alert might be real, contact the company through an official channel you find yourself. Go to their website directly, use their official app, or call the customer service number on the back of your credit card.

Scam Message Analyzer

Got a suspicious text? Paste it here to see potential red flags.

Scam #2: The Overpayment or “Refund” Con

This scam preys on your honesty and desire to do the right thing.

- How it Works: A scammer will overpay you for an item you’re selling online, or they’ll contact you pretending to be from a company and claim they need to issue you a refund, but first need your card details to process it.

The initial payment was made with a stolen card, so when the real owner disputes it, the money is clawed back from you, but the money you “sent back” is gone forever. - The Psychological Trick: This uses Authority and Confusion.

How To Protect Yourself:

- Never give your credit card number to receive a refund. Legitimate businesses can process refunds back to the original payment method without needing your full card details again.

- Be extremely suspicious of anyone who overpays you and asks for the difference back. This is a massive red flag.

Scam #3: The Physical Skimmer

This is an old-school classic that is still highly effective at gas pumps, ATMs, and point-of-sale terminals.

- How it Works: Scammers place a small, hard-to-detect device (a skimmer) over the real card slot. When you swipe your card, the skimmer reads and stores the data from your magnetic stripe. They often use a tiny hidden camera nearby to record your PIN.

- The Psychological Trick: This scam relies on Inattention and Habit.

How You Can Avoid Credit Card Fraud:

- Before inserting your card, give the card reader a quick wiggle. If it feels loose, flimsy, or has mismatched colors, don’t use it.

- Always cover the keypad with your other hand when entering your PIN. This blocks any hidden cameras.

Scam #4: The Public Wi-Fi “Man-in-the-Middle”

This scam happens when you’re trying to save on cellular data at a coffee shop, hotel, or airport.

- How it Works: A scammer sets up a fake, unsecured Wi-Fi network with a legitimate-sounding name (e.g., “Airport Free WiFi”). When you connect, all of your internet traffic—including credit card numbers and passwords—is routed through their computer.

- The Psychological Trick: This exploits our desire for Convenience and Freebies.

Your Defense Plan:

- Avoid making any financial transactions or logging into sensitive accounts while on public Wi–Fi.

- If you must use public Wi-Fi, use a reputable Virtual Private Network (VPN) to encrypt your connection.

Scam #5: The Fake Charity or Donation Scam

This scam ramps up after natural disasters or during holiday seasons.

- How it Works: Scammers create fake websites or send emails soliciting donations for a cause that tugs at your heartstrings.

- The Psychological Trick: This leverages Empathy and Generosity.

How You Can Avoid Being Scammed

- Never donate through unsolicited links in emails or social media messages.

- Go directly to the organization’s official website yourself. Use tools like Charity Navigator to vet the organization’s legitimacy.

Scam #6: The “Interest Rate Reduction” Robocall

This is a classic form of vishing that targets people with credit card debt.

- How it Works: You receive a pre-recorded robocall promising to drastically lower your credit card interest rates.

- The Psychological Trick: This uses Greed and Hope.

How You Can Avoid Falling For This Trick

- Hang up. Your credit card company will not use a robocall to offer you a better interest rate.

- Call the number on the back of your credit card and speak with the retention department directly if you want to negotiate your rate.

Scam #7: Digital E-Skimming

This is the online version of the physical skimmer, and it’s much harder to spot.

- How it Works: Hackers inject malicious code into the checkout page of a legitimate e-commerce website. When you enter your payment information, the code secretly copies it.

- The Psychological Trick: This exploits your Trust in the websites you shop on.

Your Defense Plan:

- Use a credit card instead of a debit card for online shopping.

- Use digital wallets like Apple Pay, Google Pay, or services like PayPal where available. These services tokenize your card number, so the merchant never sees it.

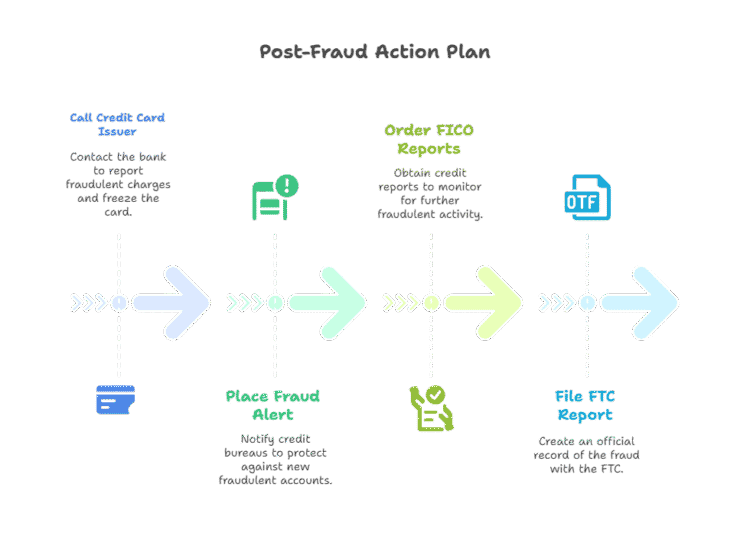

Your Post-Fraud Action Plan: The 3 Calls You MUST Make Immediately

If you realize you’ve been a victim of fraud, take a deep breath. Panic is the enemy. Here is your clear, three-step action plan.

You call the bank first. You place the fraud alert second. You file the FTC report third. In that order. No exceptions.

- Call Your Credit Card Issuer Immediately.

Use the phone number on the back of your physical card. Tell them which charges are fraudulent. They will freeze your card and begin the dispute process. - Place a Free Fraud Alert on Your Credit Report.

Contact one of the three major credit bureaus (Equifax, Experian, or TransUnion) via their website or phone. You can also check your reports for free at AnnualCreditReport.com. A fraud alert makes it harder for a scammer to open new accounts in your name. - Take it a step further: Order your FICO reports immediately.

- File an Official Report with the FTC. Go to IdentityTheft.gov. This creates an official record of the crime, which is essential for clearing your name and helps law enforcement track these criminals.

Building Your “Digital Armor”: 5 Unbreakable Habits to Prevent Credit Card Fraud

The ‘safest’ credit card user isn’t the one who avoids online shopping. It’s the one who assumes every unsolicited message is a threat until proven otherwise. Your best fraud alert is a healthy dose of suspicion.

- Use a Password Manager.

Stop reusing passwords. A password manager creates and stores strong, unique passwords for every site. Reputable options like 1Password or Bitwarden are excellent starting points. - Enable Two-Factor Authentication (2FA) Everywhere.

2FA requires a second code to log in. This is the single best way to protect your accounts. - Check Your Statements Weekly.

Set a 5-minute calendar reminder every Friday to quickly scan your recent transactions online. You’ll spot fraud days after it happens, not weeks. - Be Skeptical by Default.

Treat any unsolicited message about your finances with suspicion. The central lesson is to always initiate contact yourself through official channels. - Use Your Credit Card, Not Your Debit Card.

Its superior fraud protections mean your own cash is never at direct risk during a dispute.

How often do credit card frauds get caught?

The frequency at which credit card frauds get caught varies depending on several factors, such as the type of fraud and how quickly the victim reports the fraudulent activity. However, with the increasing use of advanced fraud detection technologies and security measures, the likelihood of detecting and preventing credit card fraud is improving.

Is credit card fraud a felony?

In most cases, credit card fraud is considered a felony offense. The severity of the crime and the corresponding penalty may vary depending on the amount of money involved, the type of fraud committed, and other factors.

Credit card fraud jail time?

The jail time for credit card fraud varies depending on the severity of the crime, the amount of money involved, and the jurisdiction in which the crime was committed. In some cases, individuals convicted of credit card fraud may face imprisonment for several years, along with fines and other penalties. It’s important to note that credit card fraud is a serious offense and can have severe consequences, both legal and financial.

Adopting these habits moves you from being a potential target to being a well-defended consumer. It’s the smartest way to ensure your money stays your money.

🚀 Next Steps:

Feeling overwhelmed? Download our free “Fraud Victim’s Emergency Action Kit,” which includes a printable checklist, direct phone numbers for major bank fraud departments, and links to the credit bureau alert pages.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.