You see the ads and hear the term all the time: “credit card cash back rewards.” It sounds like free money, but the world of credit cards can feel complex and full of traps.

You’re left wondering: Is this a real benefit? How does it actually work? And how do I choose the right card without getting overwhelmed or falling into debt?

My name is Michael Ryan, and as a former Financial Planner, I’ve helped countless people figure this out before. The good news is that cash back rewards are a real, valuable tool. The key is to understand the system and choose a card that aligns with your life, not the other way around.

This guide is designed to be your clear, simple starting point. It’s not just another list of cards. It’s an educational hub that will help you to make a smart, confident decision.

Want to know what’s in this guide? Click on the Table of Contents below:

Key Takeaways Ahead

What Exactly Are Cash Back Rewards?

At its simplest, cash back is a rebate on your spending. Money back on what you charge to your card. When you use your credit card to make a purchase, the bank gives you a small percentage of that transaction back as a “reward”.

For example, in Q1 2026 (January-March), I’m earning 5% cash back from my Discover card on grocery stores, wholesale clubs, and streaming services[web:228][web:231]. That’s real money back on Netflix, Spotify, YouTube TV—services I’m paying for anyway. And here’s the 2026 shift: streaming services have become a major rotating category across multiple card issuers[web:237], reflecting how our spending has evolved post-pandemic.

A common question I get is, “How can banks afford to do this?” Well, it’s not magic. Every time you swipe your card, the merchant (e.g., the grocery store or gas station) pays a small “interchange fee” to the bank for processing the transaction. The bank simply shares a piece of that fee with you as a thank-you for using their card.

💡 Michael Ryan Money Tip

Think of cash back not as a gift, but as reclaiming your slice of a hidden fee merchants pay on every transaction. By using a debit card, you’re essentially letting the bank keep 100% of that fee. It’s your money—claim it.

You aren’t getting something for nothing; you are simply claiming your small piece of a fee that is already built into the price of the goods you buy.

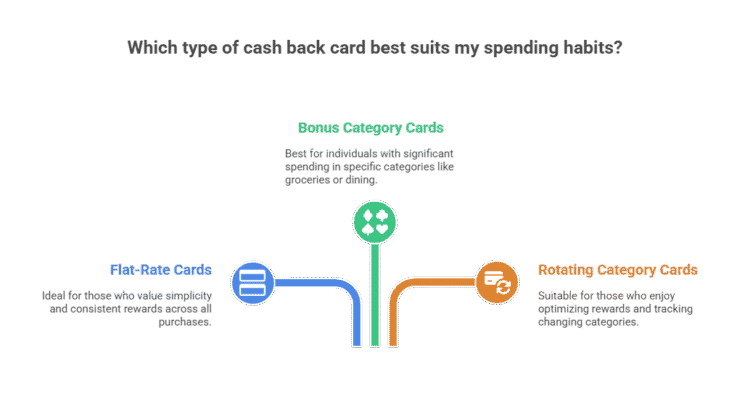

The 3 Main “Flavors” of Cash Back Cards

Not all cash back cards are created equal. They generally fall into one of three categories. Understanding which type fits your personality and spending habits is the most important step.

1. Flat-Rate Cash Back Cards

These are the simplest and most straightforward type of rewards card. They offer one consistent cash back rate. Typically between 1.5% and 2%, on every single purchase. With no exceptions or special categories to track.

- Real-World Example:

The Wells Fargo Active Cash® Card is a top-tier example, offering an unlimited 2% cash back on all purchases. - Who is this for? The Simplifier.

If you value convenience, have varied spending habits, and don’t want to juggle multiple cards or track bonus categories, a flat-rate card is a perfect fit.

Explore the Top Options: See our full guide to the Best Flat-Rate Cash Back Cards.

2. Bonus Category Cash Back Cards

These cards offer a standard base rate (usually 1%) on most purchases but provide a much higher rate (typically 3% to 5%) in specific, fixed spending categories like groceries, dining, gas, or streaming services.

- Real-World Example:

The Blue Cash Preferred® Card from American Express offers a massive 6% cash back at U.S. supermarkets (on up to $6,000 per year in purchases, then 1%). - Who is this for? The Routine Spender.

If a large portion of your monthly budget goes toward one or two key areas like groceries for your family, a bonus category card will almost always yield the highest rewards.

3. Rotating Category Cash Back Cards

These cards are for the more hands-on user. They offer a very high cash back rate, often 5%, in categories that change every three months (each quarter). Common rotating categories include Amazon.com, gas stations, wholesale clubs, or PayPal. The catch? You usually have to “activate” or “enroll” in the new category each quarter.

- Real-World Example:

The Discover Cash Back card I mentioned earlier is a classic example of this model. - Who is this for? The Optimizer.

If you enjoy a little bit of “life hacking,” don’t mind tracking categories, and want to maximize your return on seasonal spending, a rotating card can be incredibly valuable.

How to Choose: Matching a Card to Your Spending DNA

The “best” card doesn’t exist. The best card is the one that gives you the most rewards for the spending you already do.

The most effective way to find it is to become a detective for 15 minutes. Open your bank or credit card statements from the last three months and tally up your spending.

- Where does most of your money go? Is it groceries and gas?

- Is it a wide mix of online shopping, bills, and random expenses?

- Do you spend a lot on dining out or food delivery?

Once you see a clear pattern, you’ll know exactly which “flavor” of card to choose. If 40% of your budget is groceries, a bonus category card is your answer. If your spending is all over the map, a simple 2% flat-rate card is the winner.

I wrote an article that includes an interactive tool to help you decide which cash back credit card is right for you.

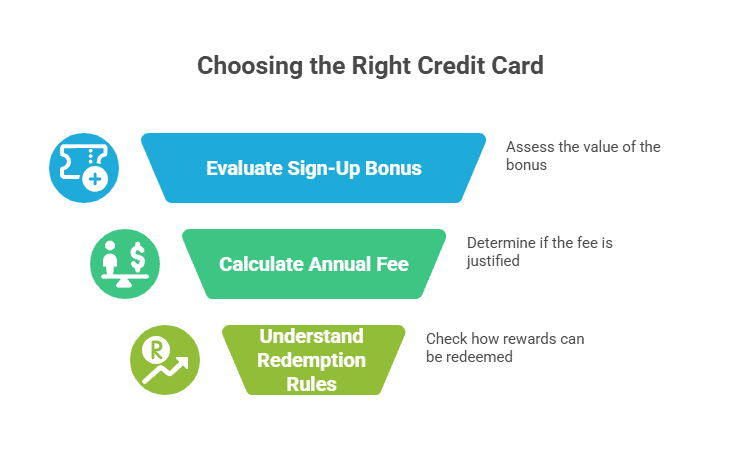

Beyond the Rate: 3 Critical Factors New Cardholders Miss

Remember, I’ve been helping people with their finances for nearly three decades. When it comes to credit card rewards programs – these are the biggest mistakes to avoid:

⚠️ Myth Busted

The biggest sign-up bonus does NOT equal the best card. A huge one-time bonus on a card that doesn’t match your daily spending is a classic trap. Long-term rewards from the right card are always more valuable than a bonus from the wrong one.

The Sign-Up Bonus Trap:

Many cards offer big sign-up bonuses, like “$200 cash back after you spend $1,000 in 3 months.” While attractive, never choose a card for the bonus alone.

The long-term value from a card that matches your spending DNA is always more important than a one-time bonus from a card that doesn’t fit your life.

The Annual Fee Calculation:

Some powerful bonus category cards come with an annual fee. This isn’t automatically a bad thing, but you must do the math.

If a $95 annual fee card gets you an extra $400 in grocery rewards each year compared to a no-fee card, it’s a great deal.

Redemption Rules:

How do you get your cash back? Most modern cards make it easy with options like a direct statement credit (which reduces your bill), a direct deposit to your bank account, or gift cards.

Always check for minimum redemption amounts (e.g., must have at least $25 to cash out).

Answering Your Top Cash Back Rewards Questions (FAQ)

These are the most common questions I’ve received from clients over the years.

Are cash back rewards considered taxable income?

For personal credit cards, the IRS generally considers cash back to be a non-taxable rebate or discount on your purchases, not income. It’s as if you simply paid a lower price for the item. The exception is if you receive a bonus for opening a bank account (which is often considered interest) or for business spending.

Always consult a tax professional for advice specific to your situation.

Is it better to use credit card rewards or cash back?

This depends on your goals. Cash back is simple, predictable, and flexible. “Points” (like Chase Ultimate Rewards® or Amex Membership Rewards®) can potentially offer much higher value, but only if you redeem them for travel by transferring them to airline and hotel partners.

For beginners, cash back is the safer and easier choice.

Which credit card gives the highest cashback?

No single card offers the highest rate on everything. The highest rates are found in specific categories. You can get 5-6% back on categories like groceries or travel with certain cards.

The highest flat-rate cash back available from major issuers is typically 2% to 2.5% on all purchases, with no annual fee.

Anything advertised as “10% cash back” is almost always a temporary promotional offer on a very specific type of spending.

Your Next Step: From Education to Action

So, do you now feel like you understand how cash back works and the main types of cards available? You have a framework to analyze your spending and identify the strategy that fits your life.

Your Action Plan

- Track your spending for 3 months to identify patterns

- Choose a card type that matches your spending habits

- Compare annual fees to ensure the extra rewards justify the cost

- Set up autopay to avoid interest charges

- Activate quarterly categories if using rotating cards

The best cash back card isn’t the one with the highest advertised rate. It’s the one that gives you the most rewards on the purchases you’re already making. Focus on long-term earning potential over flashy sign-up bonuses.

Before you go, remember the single most important rule: to benefit from rewards, you must pay your balance in full every single month. If you carry a balance, the interest you pay will always cost more than the rewards you earn.

You’ve done the foundational work. Your next step is to explore the curated lists of the best real-world cards that match your strategy.

Try searching for: 'best flat-rate cards', 'credit score for Amex', or 'points vs. cash back'.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.