Ever feel like you’re lost in a complex “Financial Maze” when it comes to your paychecks, taxes, and deductions? You’re not just imagining it. Many clients I’ve guided over my 30 years as a financial planner initially guess their actual annual earnings. Navigating through this maze can be daunting, but utilizing tools like financial planning calculators can significantly simplify the process. These calculators offer a clearer picture of your financial situation, helping you make more informed decisions about budgeting and saving. With the right guidance and resources, it’s possible to turn confusion into clarity.

This lack of clarity around total annual income severely limits effective financial planning. Stifling your ability to budget properly, plan for retirement, qualify for loans, and reach other crucial financial goals. According to the Bureau of Labor Statistics (BLS), income reporting can have significant variations, impacting national statistics and individual financial assessments.

Lost in the “Financial Maze”? Your Annual Income Clarity Starts NOW. But here’s the good news: with the right approach and insights, this maze can be navigated.

This isn’t just another article defining terms; it’s an in-depth guide to give you control & help you to calculate your annual income step-by-step, accurately.

We’ll outline the key problems that result from not having a clear understanding of total earnings and offer a comprehensive, easy-to-follow solution.

Equipped with our Michael Ryan Money Gross & Net Annual Income Calculator (featured prominently below!) and the roadmap in this article, you’ll cut through the complexity. Gaining an understanding of your yearly earnings will provide smarter budgeting, investing, tax planning, and the confident setting of both short and long-term financial goals.

So let’s get to the finish line of your Financial Maze!

Your Instant Clarity Tool: The Michael Ryan Money Annual Income Calculator

No more number crunching headaches! Get an instant picture of your earnings. This is the first step to truly calculate annual income effectively.

Gross & Net Annual Income Calculator

Calculations are estimates. Your actual gross and net income may vary based on bonuses, overtime, specific deductions, and tax filing details.

See an issue or have a suggestion? We'd love to hear from you!

This tool can also be a great first step before diving into more complex financial planning, such as understanding your Net Worth and How to Calculate It. By using this tool, you can gain a clearer picture of your current financial situation, which will empower you to make informed decisions moving forward. Additionally, I provide calculators to help you calculate your net worth quickly, providing you with valuable insights into your assets and liabilities.

How to Use Our Income Calculator Like a Pro (It’s Easier Than You Think!)

Understanding your annual income is key to managing your finances. This calculator helps you see both your Gross Income (before taxes) and estimate your Net Income (take-home pay). Here’s how to use it:

- Select Your Pay Type:

- First, choose how your pay is primarily structured. Select either “Annual Salary” or “Hourly Rate.” The correct input box will appear below.

- Enter Your Pay Rate:

- If you selected “Annual Salary,” enter your total yearly salary before any deductions.

- If you selected “Hourly Rate,” enter your standard hourly wage.

- Enter Your Work Schedule:

- Standard Hours Per Week: Input the usual number of hours you work per week (e.g., 40).

- Weeks Worked Per Year: Enter the number of weeks you typically work in a year. Usually, this is 52. Michael’s Insider Tip: Only reduce this number if you have significant periods of unpaid time off. Paid vacation/holidays count as worked weeks for this calculation to accurately calculate annual income!

- (Optional) Estimate Your Net Income:

- If you want to see an estimate of your take-home pay after taxes, enter your Estimated Effective Tax Rate (%) in the optional field.

- What is Effective Tax Rate? This isn’t just your highest tax bracket. It’s your total income taxes (Federal, State, Local combined) paid throughout the year, divided by your total taxable income, expressed as a percentage. You might find this on your previous tax return or use online estimators like the official IRS Tax Withholding Estimator. If unsure, you can leave this blank, and the calculator will only show your Gross Income.

- Important Caveat: This provides only a rough estimate. It doesn’t account for specific deductions like health insurance, 401k/IRA contributions, or tax credits, which also reduce your take-home pay. It’s a crucial starting point, but for detailed planning, consider these other factors.

Understanding Your Calculator Results: Gross, Net & What They Mean for You

The calculator will automatically show you:

- Gross Income Section:

- Gross Annual Income: Your total earnings for the year before any taxes or deductions. This is the number lenders often look at and a key figure when you calculate annual income.

- Equivalent Gross Hourly Rate: Your annual salary converted to an hourly rate, or your entered hourly rate (based on your inputs).

- Estimated Net Income Section (Only if you entered a tax rate):

- Estimated Total Annual Tax: The approximate amount of income tax based on the effective rate you entered.

- Estimated Net Annual Income: Your approximate annual income after the estimated taxes (your estimated take-home pay for the year). This is your budgeting superpower!

- Equivalent Net Hourly Rate: Your estimated hourly take-home pay after taxes.

Use this calculator to get a clearer picture of your earnings! Or if you need help calculating your MAGI for IRMAA surcharges Remember that the Net Income figures are estimates, and your actual take-home pay will depend on your specific tax situation and other paycheck deductions.

TL;DR Quick Video Summary of The Article

Unlock your true earning power! This quick guide to our Annual Income Calculator article explains gross income, net pay, and household income calculation for precise financial planning and budgeting

Ready to master these income calculation methods? Ready to understand the free Annual Income Calculator for your specific salary or hourly wages? Keep reading and find your financial clarity today.

Gross vs. Net Income: The Million-Dollar Difference in Your Financial Reality

At its core, calculating your annual income involves summing up all earnings. But distinguishing between gross annual income and net annual income is crucial. The former represents your total earnings before deductions, while the latter reflects what you actually take home. This distinction lays the foundation for all effective financial planning. (Gross Income vs. Net Income).

- Gross Annual Income: This is your “headline” number – the total amount you earn before taxes, retirement contributions, healthcare premiums, and other deductions are taken out. Financial institutions often use this to assess loan eligibility.

- Net Annual Income (Take-Home Pay): This is the money that actually lands in your bank account. It’s your gross income minus all those deductions. This is the figure you must use for realistic budgeting.

- Michael’s “Bad Advice” Buster:

I’ve seen so many people proudly state their gross income when discussing their finances, only to be perpetually confused why they feel broke. The Aha! Moment is realizing that your Net Income dictates your lifestyle and savings potential, not the gross. Budgeting with your gross income is like planning a gourmet meal based on the grocery store’s entire inventory before you’ve paid for your cart! - Insight: Gross income is your potential. Net income is your reality. Plan with reality.

Hourly Hustle to Yearly Haul: Calculating Annual Income from Variable & Gig Work

For those earning an hourly wage, the annual income calculation typically entails multiplying your hourly rate by the number of hours worked per week, and then by 52.

Example: $25/hour × 40 hours/week × 52 weeks = $52,000 Gross Annual Income.

- But what if your hours aren’t that neat? Or what if you’re part of the growing gig economy?

- This method highlights the variability based on full-time vs. part-time status and emphasizes the need to account for overtime, holidays, and unpaid time off when you calculate annual income.

Michael’s “Real World” Methods for Irregular & Multiple Income Streams

When your income isn’t a predictable salary, like for many of my entrepreneurial clients or those with thriving side hustles, you need more sophisticated ways to calculate annual income. These approaches are similar to guidelines used by institutions like USDA Rural Development for assessing variable income:

- The “Look Back & Average” Method (for inconsistent income):

- Compile all income sources: wages, freelance payments, investment returns, etc.

- Gather income statements for the past 3-12 months (more if highly seasonal).

- Calculate your average monthly gross income.

- Multiply by 12.

- Client Scenario:

Let’s talk about ‘Freelance Fiona.’ Her project income was all over the map – $8k one month, $2k the next. The simple weekly formula told her nothing. We averaged her last 6 months of actual earnings, which was $4,500/month.

This gave her a realistic $54,000 projected gross annual income, a figure solid enough to help her confidently apply for a business line of credit she needed.

- The Year-to-Date (YTD) Projection (for mid-year checks):

- Take your total gross earnings from your latest paystub or income summary.

- Divide by the number of pay periods passed so far this year.

- Multiply by the total number of pay periods in a year (e.g., 26 for bi-weekly, 12 for monthly).

- Aha! Moment: Many underestimate the power of their “small” side hustles until they annualize the YTD earnings!

- Combining Streams (the norm for many!): If you have a W2 job AND freelance income, calculate annual income for each stream separately using the best method, then sum them for your total gross. Don’t forget investment income or other regular payments!

Unmasking Your Household Income: It’s More Than Just Your Paycheck in the Annual Calculation

For many critical financial decisions, think qualifying for a mortgage, applying for financial aid, or simply getting a true picture of your family’s financial strength, you need to calculate annual household income.

- What is Annual Household Income? T

his encompasses the total gross income of all household members aged 15 and older (as per U.S. Census Bureau definitions, though specific programs may vary). This includes wages, self-employment income, rental income, investment income, Social Security benefits, pension income, and unemployment compensation (Household Income Definition). - Michael’s Key Clarification & Why It Matters:

Who counts as ‘household’ can be tricky. For Census data, it’s generally everyone residing together. However, for specific programs like the Affordable Care Act (ACA) subsidies, the definition is often tied to your tax dependents (Healthcare.gov – Income & Household Info). Always verify the specific definition for your purpose!

An accurate calculation is essential for loan applications, benefit eligibility, and shared family financial goals. - The Calculation Steps:

- Determine the gross annual income for each eligible household member using the appropriate methods discussed above.

- Add all these individual gross annual incomes together. This is your total gross household income.

- Median vs. Average – A Quick Insight:

The 2023 U.S. median household income was $80,610. “Median” is the middle point – half earn more, half less. “Average” household income is often higher ($114,500 in 2023) because it’s skewed by very high earners. Knowing your household’s number helps you understand your financial standing in a broader context.

Don’t Forget These! Factoring in Deductions, Taxes & “Hidden” Income for a True Annual Picture

To truly calculate annual income that reflects your financial reality, especially your net income, you must account for deductions and all income sources.

- Common Deductions from Gross Pay:

- Taxes: Federal income tax, State income tax (if applicable), Local income tax (if applicable), Social Security, and Medicare (FICA).

- Pre-tax Contributions: 401(k)/403(b) retirement savings, traditional IRA contributions (if eligible for deduction), Health Savings Account (HSA) contributions, some health insurance premiums.

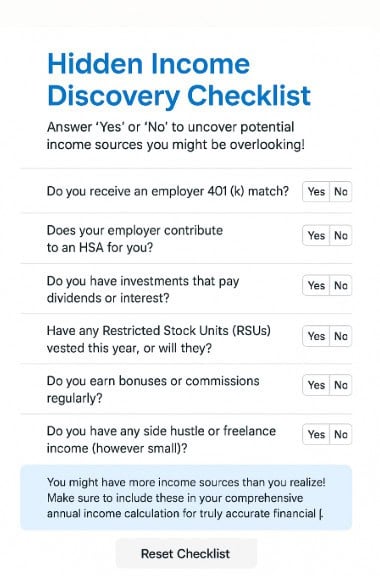

- “Hidden” Income Sources Often Overlooked (but part of your total financial picture):

- Employer 401(k)/Retirement Match: This isn’t on your W2 as taxable income, but it’s vital “free money” that boosts your total compensation and future net worth.

- Employer HSA Contributions: Tax-advantaged money that helps cover medical costs.

- Investment Income: Dividends, interest, capital gains. These are taxable income!

- Bonuses, Commissions, Tips: Crucial to track for an accurate annual total.

- RSUs & Stock Options: Michael’s Critical Warning for Tech & Corporate Employees:

Vested RSUs are taxable income for that year. I’ve seen too many clients get a nasty tax surprise because they didn’t factor this into their estimated payments or overall income picture when they tried to calculate annual income.

Your salary is the main course, but the appetizers, side dishes, and even the ‘free’ breadsticks (like an employer match) all contribute to your total financial feast.

Your Next Steps: From Income Clarity to Financial Conquest in 2025

Determining your exact annual income is foundational. Without clarity around your gross pay, deductions, and final take-home amount, you operate in that problematic Financial Maze, unable to effectively budget, save, invest, or plan long-term. Fortunately, this guide and our calculator have equipped you to finally gain control.

- Leverage Your Accurate Annual Income Calculation To:

- Budget with Unprecedented Precision: Allocate your net income effectively.

- Set Achievable Financial Goals: Know what’s truly possible for savings, investments, and debt payoff.

- Qualify for Loans More Confidently: Approach lenders with precise gross income figures.

- Optimize Your Tax Strategy: Understand your potential tax burden and identify savings opportunities.

- (For official guidance, always refer to resources like the IRS – Tax Planning Information).

- Make Smarter Investment Decisions: Align your investment capacity with your true income.

- Michael Ryan’s Final Word:

For decades, the most significant breakthroughs I’ve witnessed with clients began with this single step: achieving crystal clarity on their income. When you truly know what you earn, the fear and confusion dissipate. You stop wandering and start making intentional, powerful moves.

The fog around “What do I actually earn each year?” has lifted. With your new expertise to calculate annual income, feel confident taking those intentional steps toward the financial future you desire!

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.