Did a student loan suddenly vanish from your credit report? Or are you trying to remove one? Before you celebrate or panic, let’s be crystal clear: this is one of the most misunderstood topics in personal finance, and the wrong move can damage your credit for years.

I’ve spent almost three decades guiding people through their credit journeys. I’ve seen the relief when an erroneous default is deleted. And the deep regret when a positive, 10-year-old account is closed unnecessarily, tanking a credit score just before a mortgage application.

This guide will give you what others don’t: a clear, no-fluff explanation of why loans disappear, the real impact on your score, and a strategic framework for what to do next.

Key Insights You’ll Find Inside:

- The #1 Reason Loans Vanish: Learn why a loan servicer transfer can make a loan temporarily disappear and why you shouldn’t panic when it happens.

- The Credit Score Myth: Uncover the truth about your length of credit history and why removing an accurate, paid-off loan can actually harm your FICO® Score. A mistake many people make.

- Fixing Defaults & Blemishes: Discover how the federal “Fresh Start” program offers a powerful shortcut to remove a default, and learn the advanced tactic of using a “Goodwill Letter” for single late payments.

Key Takeaways Ahead

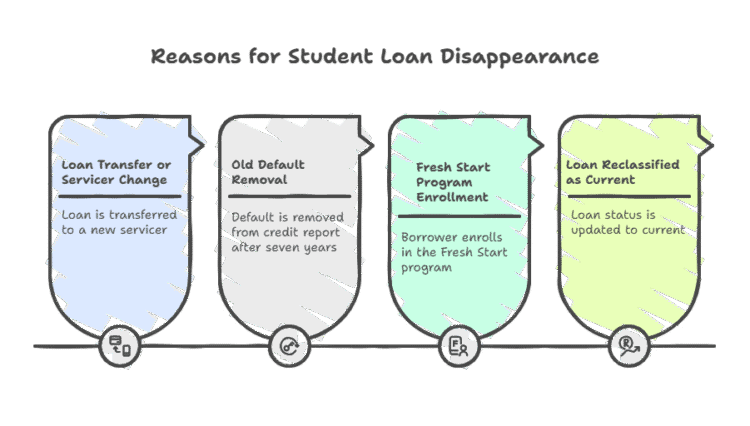

Why Did My Student Loan Disappear? The 3 Core Reasons

If a loan vanished without you doing anything, it’s almost always one of these three reasons.

Loan Transfer or Servicer Change:

This is the most common and least worrisome reason. If your loan was sold or transferred from one servicer (e.g., Nelnet) to another (e.g., MOHELA), the old account will show as “Closed” or “Transferred.” The new servicer will then report a new account.

There might be a 30-60 day lag where it seems to have disappeared, but rest assured, it will reappear.

It’s a Very Old Default:

Under the Fair Credit Reporting Act (FCRA), most negative information, including a student loan default, must be removed after seven years from the date of the first missed payment. If your loan went into default in 2018, it’s likely scheduled to fall off your report around now.

Crucial point: This only removes it from your credit report. The debt itself is still owed, and the government can still collect via wage garnishment or tax refund offset.

The “Fresh Start” Program (For Federal Loans):

This is a game-changer. The Department of Education’s “Fresh Start” initiative is a temporary program designed to help borrowers with defaulted federal loans. When you enroll, your loans are reclassified as “current,” and the record of default is deleted from your credit report. I helped a client enroll in late 2023; the change appeared on her credit report within two months.

This is the single most powerful tool available right now for fixing a federal student loan default.

The Real Impact: Why “Removing” a Loan Can Backfire

Let’s debunk a huge myth. You don’t want to remove an accurate student loan from your credit report, especially one with a long history of on-time payments.

💡 Expert Insight:

According to credit bureau Experian, “Closing an account can cause your credit scores to drop… it lowers your overall credit age [and] it can increase your credit utilization ratio.”

Think of it this way: 15% of your FICO® Score is based on the Length of Your Credit History. An old student loan acts as a powerful anchor, proving you can manage credit responsibly over time.

Removing it is like demolishing your house’s foundation to make the lawn look bigger. To understand how your balances affect your score, check out our complete guide to credit utilization.

Credit Utilization Calculator & Worksheet

Enter your credit card balances and limits to see your utilization ratios.

See an issue or have a suggestion? We'd love to hear from you!

- The Goal IS: To remove inaccurate negative information (e.g., a payment marked late when you paid on time).

- The Goal IS NOT: To erase accurate accounts, positive payment history, or legitimate debts.

Related Reading:

- Student Loan Forgiveness Center Calls Scam

- Build Your Credit Score From Scratch!

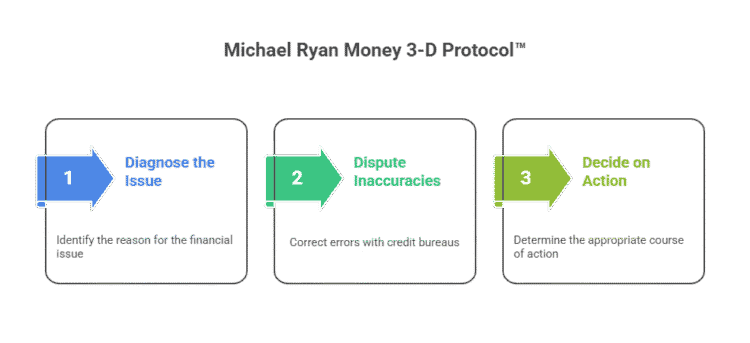

The Michael Ryan Money 3-D Protocol™: Your Action Plan

Instead of panicking, use this framework to decide your next move.

1. DIAGNOSE: Why Is It Gone (or Why Do You Want It Gone)?

- Did it disappear on its own? Review your report. Do you see a “Transferred” status? Was it an old default? You may not need to do anything.

- Is there an error? Is a payment wrongly marked as late? Is the balance incorrect? Is an account showing in default when you’re in the Fresh Start program? This is your target.

2. DISPUTE: Correcting Inaccuracies

If you’ve identified a genuine error, you have the right under the FCRA to dispute it with all three credit bureaus (Equifax, Experian, TransUnion). You can do this online through their websites.

Provide a clear explanation and upload any proof you have (e.g., a bank statement showing the payment was made). They have 30 days to investigate.

3. DECIDE: Know When to Leave It Alone

- If the loan is accurate and in good standing: Leave it. It’s helping you.

- If it’s an old, paid-off loan: Leave it. It’s a positive historical record that helps your credit age.

- If you got out of default via Fresh Start: Monitor your report to ensure the default status is deleted. Then it’s time to build a new, positive history with a proven financial plan.

My Prediction:

As we move past the post-pandemic administrative forbearance period, lenders will more heavily scrutinize the age and stability of credit histories. The long-term, positive data from a student loan will become an even more valuable asset, making the idea of removing it obsolete.

FAQs

Why did my student loans disappear from my credit report?

Your student loans may disappear from your credit report if they are in forbearance or deferment. It may also be due to a mistake made by your loan servicer.

Can all student loans be removed from a credit report?

Unfortunately, not all student loans can be removed from a credit report. It largely depends on the specific circumstances and whether there are errors on the credit report or a lender is willing to negotiate.

Will removing student loans from my credit report make my credit score go up?

Yes! Removing negative marks, such as missed payments or defaults, from your credit report can increase your credit score.

Can removing student loans from my credit report hurt my credit score?

It’s possible, as removing a loan from your credit report can impact your credit history. However, the potential benefits of removing the loan may outweigh this risk.

How long does it take for negative marks to fall off a credit report?

Most negative marks, including missed payments and defaults, will fall off a credit report after seven years.

Is it better to remove student loans from my credit report or pay them off?

Ideally, it’s best to pay off your student loans and keep them on your credit report as a positive mark. However, if you’re struggling to make payments and your credit score is being negatively impacted, removing the loans from your credit report may be a good option to consider.

Remember, your financial future is in your hands. Removing student loans from your credit report can be a game changer, but it’s important to weigh the potential benefits and drawbacks before pursuing this option. With careful consideration and smart financial planning, you can achieve the financial freedom you deserve.

Final Takeaway: Be a Credit Historian, Not a Demolition Crew

Your credit report is your financial story. The goal is not to tear out chapters but to make sure the story is told accurately. A student loan, managed well, is one of the best character references you can have.

Protect your positive history, dispute only genuine errors, and you will build a score that opens doors for years to come.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.