The average 403(b) balance hit $125,400 in Q2 2025—up 8.7% in one quarter. That’s what compounding does when you’re contributing consistently. But most educators and nonprofit workers don’t realize a 5% increase in contributions over 30 years can add $600,000+ to their retirement balance. The 2026 contribution limit jumped to $24,500 (up $1,000 from 2025), meaning there’s more room to grow tax-deferred savings—if you’re maximizing the numbers.

What is a 403(b) Calculator and Why Do You Need One?

A 403(b) calculator is a tool that estimates your future retirement savings and income from a 403b plan, based on factors like contributions, employer matches, investment returns, and time. It helps you plan and optimize your retirement strategy.

This planning tool is essential for employees of public schools, non-profits, and certain churches who have access to 403(b) retirement plans. It projects your 403b account balance at retirement.

403(b) Retirement Savings Calculator

Project a potential 403(b) balance using payroll contributions, employer matching, investment expenses, inflation, and current contribution rules.

Projected 403(b) Accumulation

Projected Balance by Age

First-year contribution check

Important cautions

Projection assumptions

Many people underestimate how small changes in their 403(b) contributions can impact their long-term savings; this tool helps you visualize that. The IRS provides guidelines for 403(b) plans, and this calculator helps ensure you stay within those contribution limits.

Retirement Savings Comparison

Understanding the Basics of a 403(b) Plan

Watch this quick slide show by pressing play below to get a better understanding of what a 403b is all about

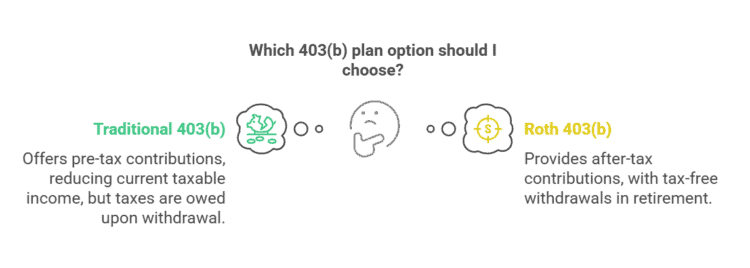

What is a 403(b) plan?

A 403(b) plan is a tax-advantaged retirement savings plan offered to employees of public schools, 501(c)(3) non-profit organizations, and certain religious institutions. This plan allows eligible employees to make pre-tax or Roth contributions.

Similar to a 401(k) plan for private-sector employees, a 403(b) offers tax benefits to encourage retirement saving. It is often called a tax-sheltered annuity (TSA) plan.

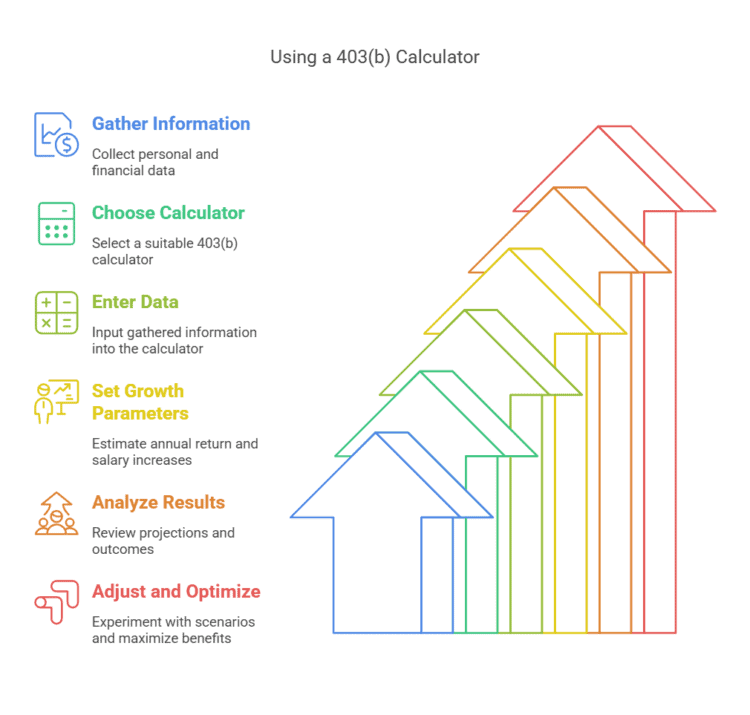

Step-by-Step Guide to Using a 403(b) Calculator

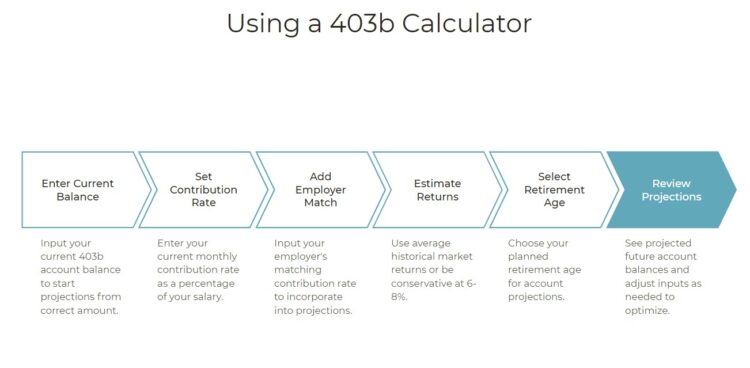

Step 1: Gather Your Information

Before you start, gather the following information:

- Your current age

- Your current annual salary

- Your existing 403(b) balance (if any)

- Your employer’s match structure (e.g., 50% match on the first 6% of salary)

- The annual contribution limits for 403(b) plans (see the IRS website for the most up-to-date information).

Step 2: Choose a 403(b) Calculator

Many reputable websites offer free 403(b) calculators. Obviously mine is the best, but… Here are some other popular options include:

Step 3: Enter Your Data Accurately

Carefully input all the information you gathered in Step 1 into the calculator. Double-check your entries to ensure accuracy.

Step 4: Set Growth Parameters

Most calculators will ask you to estimate:

- Annual Rate of Return: A conservative assumption for balanced portfolios is typically 5-6%. This represents the average annual growth you expect from your investments.

- Annual Salary Increases: A default of 2% is often used, but you can adjust this if you expect significant promotions or raises.

Step 5: Analyze the Results

The calculator will generate projections, including:

- Projected Balance at Retirement Age: The estimated total value of your 403(b) account when you retire.

- Estimated Monthly Income: An estimate of how much monthly income your 403(b) could provide in retirement (often based on the 4% rule, which suggests withdrawing 4% of your balance each year).

- Total Contributions: The sum of your contributions and your employer’s contributions over time.

Step 6: Adjust and Optimize

- Scenario Planning: Experiment with different inputs. What happens if you increase your contribution rate? What if you retire later? What if your investments perform better or worse than expected?

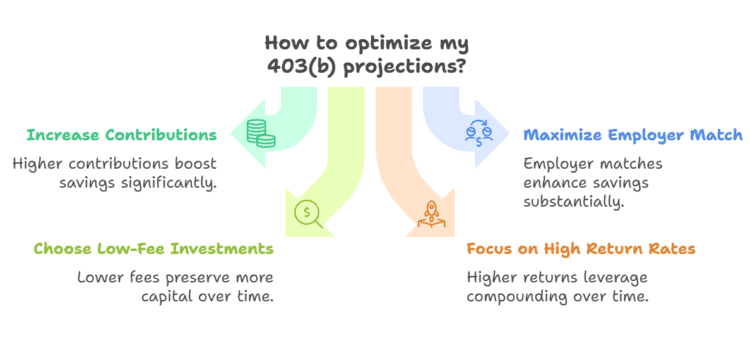

- Maximize Employer Match: If your employer offers a match, contribute at least enough to get the full match. It’s essentially free money.

- Consider Fees: Be aware of any fees associated with your 403(b) plan, as they can impact your overall returns.

Key Factors Impacting Your 403(b) Projections

These factors interact to determine your final balance. Understanding how these variables influence your 403b account balance is crucial for effective retirement planning.

For instance, a higher contribution rate and employer match will significantly boost your projected savings.

Common Mistakes Using 403(b) Calculators (and How to Avoid Them)

Common mistakes when using 403(b) calculators include using unrealistic return assumptions, ignoring inflation, forgetting the employer match, entering inaccurate data, and not updating the calculations regularly. These errors can lead to inaccurate retirement projections.

Avoiding these pitfalls is crucial for accurate financial planning and ensuring you have a realistic estimate of your future 403b account balance. Remember, a retirement calculator is only as good as the data entered.

Investment Strategies for Your 403(b) Plan (Brief Overview)

While specific investment advice is beyond the scope of this article, consider aligning your 403(b) investments with your risk tolerance and time horizon.

Diversification across different asset classes is a generally recommended strategy.

Common 403(b) investment options include target-date funds, mutual funds, and annuities. Consult with a financial advisor for personalized guidance.

Choosing the right investments can feel overwhelming. Studies consistently show the benefits of diversification in reducing portfolio risk.

Key 403(b) Calculation Takeaways:

In summary, a 403(b) calculator is an essential tool for planning a secure retirement. By understanding key inputs and making realistic assumptions, you can effectively use this tool to optimize your savings. Remember to regularly review and adjust your plan to stay on track.

What is a 403(b) retirement savings calculator, and how can it help maximize my retirement funds?

A 403(b) retirement savings calculator estimates your retirement savings growth. By inputting current savings, contributions, and expected returns, you can adjust your plan to maximize funds.

These calculators model various scenarios, considering factors like employer match and annual salary, to help you optimize your 403(b) contributions.

Can I use a 403(b) savings calculator to estimate my retirement income?

Yes, a 403(b) savings calculator can estimate your retirement income by considering factors like current savings, expected returns, and retirement age. These scenarios are hypothetical, but provide valuable planning insight.

Remember that actual rates of return may vary, and these projections are not guarantees. However, they offer a starting point for your retirement plan.

Always validate results with a certified financial planner, especially when coordinating 403(b)s with IRAs/HSAs.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.