For years, I sat with successful couples; doctors, business owners, executives. Who all shared a common, urgent fear: the 2026 estate tax “sunset.” They were rushing to create complex A/B Trusts, worried that the high federal estate tax exemption was about to be cut in half.

But the game has completely changed.

On July 4, 2025, the “One Big Beautiful Bill Act” (OBBBA) was signed into law, making the high estate tax exemption permanent and even increasing it. The ticking clock is gone. For most families, this is fantastic news. But it makes the choice of a proper estate plan more critical than ever.

An A/B trust, once a necessity, might now be a costly mistake for your family.

This guide will give you the clear, no-fluff comparison you need to navigate this new landscape and protect your family’s future.

📌 Key Takeaways: Estate Planning After OBBBA

- The 2026 “Sunset” is Cancelled: The OBBBA of 2025 eliminated the scheduled reduction in the estate tax exemption.

- Exemption Increased and Permanent: The federal exemption is now a permanent $15 million per person starting in 2026 (adjusted for inflation), up from $13.99 million in 2025.

- “Portability” is the New Default: With a permanent $30 million exemption for married couples, portability is the simplest and most tax-efficient strategy for the vast majority of estates.

- A/B Trusts Are Now for Control, Not Taxes: The #1 reason to still consider an A/B trust is for specific non-tax goals, like protecting assets in a blended family or from creditors.

What’s Inside This Guide

The New Law: What Actually Happened in 2025?

Instead of the federal estate tax exemption dropping to around $7 million per person in 2026, the new OBBBA law did the opposite.

📊 Quick Stat: The New 2026 Exemption

The “One Big Beautiful Bill Act” permanently increased the federal estate and gift tax exemption to $15 million per individual ($30 million for married couples) starting in 2026, with annual inflation adjustments. The scheduled “sunset” that would have cut the exemption was eliminated entirely.

For high-net-worth families, this removes the urgent deadline that drove so much planning and makes strategies like portability even more powerful.

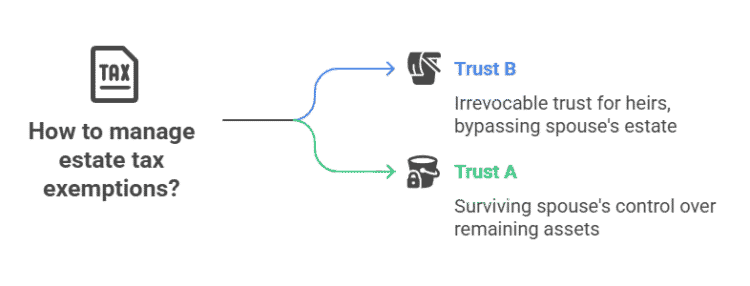

What is an A/B Trust in Simple Terms?

An A/B trust, also known as a bypass trust or credit shelter trust, is a joint trust for a married couple that automatically splits into two separate trusts when the first spouse passes away.

🔍 Explained Simply: The “Two Buckets” Analogy for A/B Trusts

Imagine your and your spouse’s estate tax exemptions are two empty buckets. When the first spouse passes, an A/B trust pours their exemption amount into “Bucket B” for the kids, which is then sealed and protected. The rest goes into “Bucket A” for the surviving spouse. This ensures the first spouse’s entire “bucket” is used and shielded from future taxes, no matter what.

Trust B (The Bypass Trust):

This trust is irrevocable and is funded with assets from the deceased spouse’s estate, up to the federal exemption. It “bypasses” the surviving spouse’s estate and is earmarked for the ultimate heirs (usually the children).

Trust A (The Survivor’s Trust):

This trust holds the remaining assets. The surviving spouse typically has full control over this trust during their lifetime.

The Great Debate: A/B Trust vs. Portability in the New Tax World

The OBBBA made the high exemption permanent. Portability, the rule that allows a surviving spouse to use their deceased spouse’s unused exemption, has now become the dominant strategy.

Here is the central decision you and your advisors will face.

| Factor | A/B Trust (Bypass Trust) | Portability |

|---|---|---|

| Simplicity & Cost | Complex and expensive. Requires ongoing administration, a separate tax ID for Trust B, and annual tax filings (Form 1041). | Much simpler and cheaper. Requires filing a Form 706 after the first death to elect portability, but no ongoing trust administration. |

| Asset Control | High Control. The first spouse to die dictates exactly where the assets in Trust B go. Protects assets from the surviving spouse’s future creditors or a potential remarriage. | Low Control. The surviving spouse inherits the assets outright and has total control. They could remarry and leave the assets to a new spouse. |

| Capital Gains Tax | Potential Drawback. Assets in Trust B get a “step-up in basis” at the first death, but **do not** get a second step-up at the survivor’s death. This can create a large capital gains tax bill for your heirs. | Major Advantage. All assets are owned by the surviving spouse and receive a second **step-up in basis** at their death, which can wipe out a lifetime of capital gains for your heirs. |

| Best For… | Blended families, couples with state estate tax concerns, or those prioritizing ironclad asset protection and control over tax simplicity. | Couples whose primary goal is federal estate tax efficiency and minimizing future capital gains tax for their heirs. This is the new default for most. |

Why an A/B Trust Still Matters: The Non-Tax Benefits

In this new era of high, permanent exemptions, the best arguments for an A/B trust are no longer about federal taxes.

- Protecting Heirs in Blended Families:

This is the #1 reason I still suggest people consider A/B trusts. It ensures that the children from a first marriage will inherit their share, regardless of what the surviving spouse decides to do later in life. - Creditor Protection:

Assets placed in the irrevocable Trust B are generally shielded from the surviving spouse’s future creditors, lawsuits, or bankruptcy. - State Estate Tax Planning:

Several states have their own estate tax with a much lower exemption, and many of these states do not recognize portability. In states like Massachusetts or Oregon, an A/B trust may still be essential for saving on state taxes.

Ready to win at estate planning?

Get one clear money move each week—timing tips, tax traps to avoid, and proven playbooks you can use in minutes.

Join thousands of readers just like you.

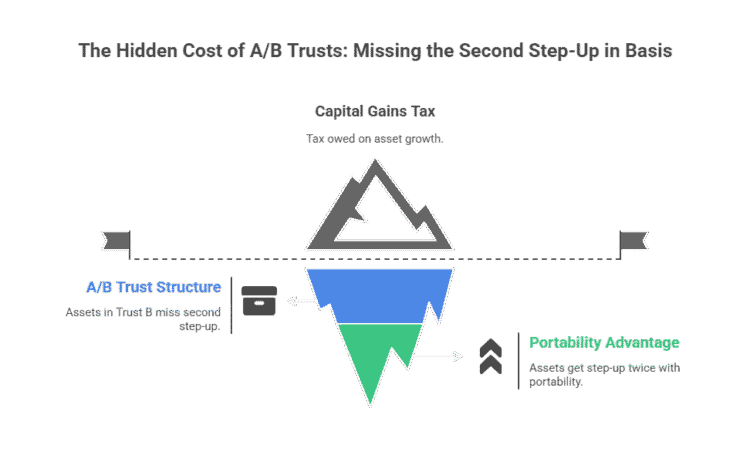

The Hidden Cost of an A/B Trust: Losing the Second Step-Up in Basis

This is the critical trade-off that is now more important than ever. When you inherit an asset, its “cost basis” for tax purposes steps up to its fair market value at the date of death, erasing the capital gains tax liability up to that point.

- With Portability, all assets get this step-up twice. Once at the first death and again at the second.

- With an A/B Trust, the assets in Trust B get a step-up at the first death, but because they are not part of the surviving spouse’s estate, they do not get that second step-up.

💡 Michael Ryan Money Tip: A Real-World Example

Imagine a stock portfolio worth $5 million goes into Trust B. It grows to $9 million by the time the surviving spouse passes away. Your kids inherit it, and if they sell, they will owe capital gains tax on the $4 million of growth. With portability, that same portfolio would have received a second step-up to $9 million, and the capital gains tax would have been zero. With estate taxes off the table for most, avoiding this capital gains hit is now the bigger financial win.

Explore deeper estate planning topics. Now, try searching for: living trust cost, special needs trust, or contesting a will.

For the Surviving Spouse: Your First Steps After a Loved One Passes

If your spouse has passed away and you’ve discovered you are the trustee of an A/B trust, the responsibility can feel immense. Take a deep breath. Here are your first three calls to make.

- Locate the Trust Documents:

Find the original, signed estate planning documents. They are your roadmap. - Contact the Estate Planning Attorney:

The lawyer who drafted the trust is your most important ally. They will guide you through the legal process of formally dividing the trust. - Do Not Co-mingle Assets:

This is critical. You must get a new Tax ID number (EIN) from the IRS for Trust B and open a new, separate bank account in the name of Trust B. All of its assets, income, and expenses must be kept completely separate from your personal assets and those in Trust A.

A/B Trust Frequently Asked Questions (FAQ)

Q: What is the federal estate tax exemption for 2026?

A: Thanks to the “One Big Beautiful Bill Act,” the federal estate tax exemption increases to $15 Million per person ( $30 million for a married couple) starting in 2026. This high exemption is now permanent and will be adjusted for inflation annually.

Q: How much does an A/B trust cost to set up?

A: While costs vary, you can learn more about what to expect by reading our guide on how much a living trust costs to set up. You must also budget for ongoing annual costs for accounting and tax filing for Trust B.

Q: Can retirement accounts like a 401(k) or IRA go into an A/B trust?

A: This is an advanced strategy. Naming a trust as the beneficiary of an IRA or 401(k) is complex and has major tax implications under the SECURE Act’s 10-year rule. It must be done with extreme care by a specialist attorney to avoid accelerating taxes.

Michael Ryan Money’s Final Take: Control vs. Simplicity in a New Era

The permanent, high estate tax exemption is a watershed moment for financial planning. The urgent, tax-driven need for A/B trusts is over for the vast majority of families. Today, the simplicity and superior capital gains treatment of portability make it the default and best choice for most.

However, if your primary goal is not just saving taxes but ensuring ironclad control over your legacy—especially in cases of blended families or concerns about future creditors—the A/B trust remains a powerful, relevant tool. The key is to understand the trade-offs in this new environment: you are now choosing between control and tax simplicity. Choose wisely.

Disclaimer: This guide is for educational purposes and reflects the law as of the “One Big Beautiful Bill Act” of July 2025. It does not constitute legal or tax advice. Please consult with a qualified estate planning attorney and a CPA.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.