As a security and fraud investigator who teaches White-Collar Crime, I’ve seen the aftermath. Deed & home title fraud isn’t a technical problem, but a human one. It’s the violation of having your safest space, your home stolen from under you with nothing but a pen and a lie.

For most Americans, a home is more than a place to live. It’s a cornerstone of financial stability and personal achievement. But what if, without your knowledge, someone forged your name, filed false documents, and legally stole your home?

Welcome to the disturbing world of home title theft, a growing form of mortgage fraud that has left countless victims in legal and financial limbo.

In this guide, we’ll go beyond the headlines and dissect how these criminals think, so you can build a fortress around your most valuable asset.

Unlock the Hidden Risks & Rewards of Home Title Security

What Is Mortgage & Home Title Theft?

Home title theft, also known as deed fraud or real estate title fraud, occurs when a criminal unlawfully transfers the title of your home by forging your signature on legal documents and recording the fake deed with your local county recorder’s office. From that point on, it may appear as though you no longer own your property.

The goals of title thieves include:

- Stealing homes outright, particularly if they are vacant or mortgage-free

- Taking out home equity loans or lines of credit using your property as collateral and vanishing with the money

Expert Update (2025): This isn’t a theoretical risk. According to the FBI’s latest data, real estate fraud losses topped $475 million in 2023. From my experience, this crime often targets seniors or those with significant home equity, making proactive monitoring more critical than ever.

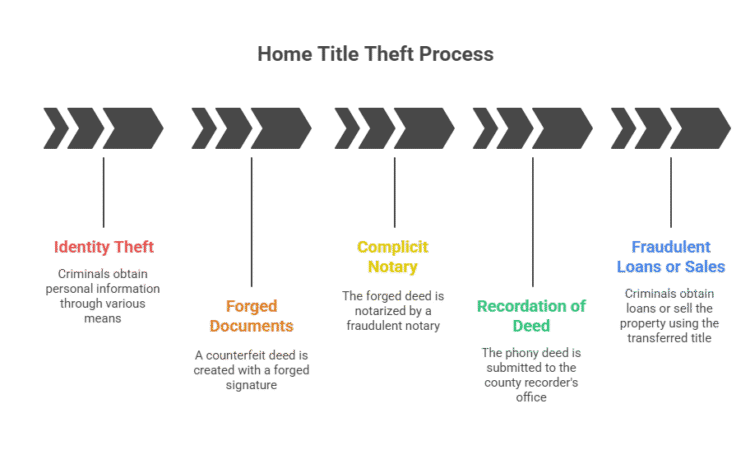

How the Home Title Scam Works: A Breakdown

Home title theft is sophisticated, but the scam follows a relatively predictable pattern:

- Identity Theft:

Criminals gain access to your personal information through phishing emails, social media, data breaches, or even stolen mail. - Forged Documents:

A counterfeit deed is drafted and includes a forged version of your signature. - Complicit or Fake Notary:

The forged deed is notarized either by a fraudulent notary or one unaware of the scam. - Recordation of the Deed:

The phony deed is submitted to the county recorder’s office, which typically does not verify the identity of those submitting documents. - Fraudulent Loans or Sales: Once the title appears transferred, criminals may:

- Obtain loans using the property as collateral

- Sell the property to unsuspecting buyers

💡 Michael Ryan Money Tip: Thieves Exploit Inattention, Not Weak Locks

After nearly 3 decades as a planner, I’ve learned that title thieves don’t pick locks; they exploit inattention. Most of my clients check their 401(k) statements weekly, but they haven’t looked at their property deed since the day they closed. Criminals know this. They target the “quietest” assets, mortgage-free homes of seniors or vacant vacation rentals. Why? Because the lack of monthly bank statements means the fraud can go undetected for months.

High-Risk Targets Include:

- Elderly homeowners

- Vacancy or seasonal homes

- Mortgage-free properties

- Second homes and rental properties

🛡️ What’s Your Home Title Security Score? A 5-Point Expert Checklist

Take this simple quiz to see how protected your most valuable asset really is:

Home Title Security ScoreWhat’s Your Home Title Security Score?

Title theft is a real threat, but how vulnerable are you really? Answer 5 quick questions to get your personalized security score and an expert action plan.

Victims’ Stories: Real-Life Consequences

Linda from Florida, a retiree who owned her home outright for over 30 years, returned from a visit to family only to discover a “For Sale” sign in her yard. Someone had fraudulently sold her home and walked away with over $400,000.

Thomas in California, a small business owner, received a foreclosure notice for a loan he never took out. By the time he uncovered the scam, his credit had been ruined, and he had to fight a 14-month legal battle to reclaim his property.

A Brooklyn homeowner, whose brownstone had been in his family for generations, lost ownership after a fraudster forged a deed, using it to sell the property to a developer for $750,000. The elderly homeowner had to sue to get it back at great personal and financial cost.

Why Certain States Are Hit Harder

Fraudsters tend to operate in areas where the conditions make title theft easier and more lucrative. States most affected include:

- Florida: High number of retirees and vacant vacation homes

- California: Expensive real estate attracts fraud; large immigrant population may be unfamiliar with U.S. title laws

- Texas: Booming real estate market with high turnover

- New York: Dense urban areas with high-value homes and many elderly owners

- Arizona: Seasonal homes and snowbird residents are often vacant for long stretches

These states share certain risk factors:

- High property values

- Absentee ownership

- Elderly homeowners

- Easily accessible public property records

How to Spot the Warning Signs

Title theft often goes undetected until major damage is done. Be alert for:

- Mail from banks or lenders you’ve never dealt with

- Foreclosure notices or property tax bills you weren’t expecting

- Utility bills that suddenly stop arriving

- A dip in your credit score from unexplained inquiries

- Notification of a deed change (if you’re enrolled in monitoring)

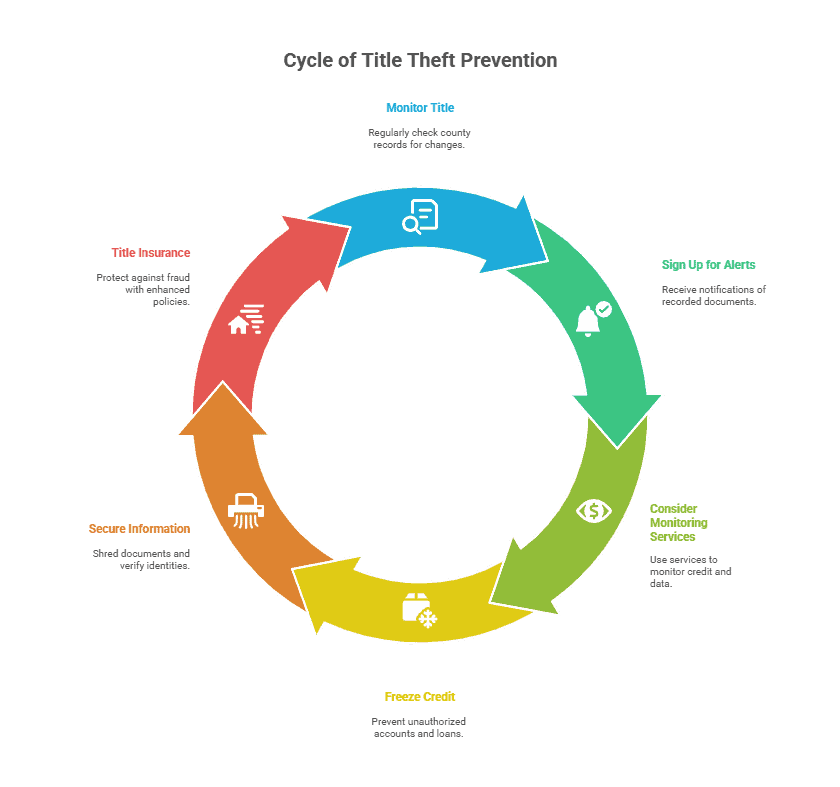

How to Protect Yourself from Title Theft

- Monitor Your Title:

Periodically check county records for any changes to your deed. - Sign Up for Property Alerts:

Many county recorder’s offices offer free alert systems that notify you if documents are recorded against your property. - Consider Paid Monitoring Services:

- tor your credit and personal data to reduce risk of identity theft, which is the gateway to title fraud.

- Freeze Your Credit:

Prevent unauthorized accounts or loans from being opened in your name. - Secure Sensitive Information:

Shred personal documents and verify the identity of anyone requesting personal details. - Title Insurance:

Though it may not cover fraud after purchase, some enhanced title policies do offer protection. Ask your insurer for details.

🤔 The Michael Ryan Money’s Verdict: Are Paid Title Monitoring Services Worth It?

For 90% of my clients, the free property alert system offered by your county is a powerful and sufficient first line of defense. It will notify you the moment a new document is filed, which is the critical event.

A paid service like Home Title Lock is a smart investment if:

- You live in a high-risk state and own multiple properties.

- You are an absentee owner (e.g., rentals, long-term vacationer).

- You simply want the peace of mind of an insured, managed service.

My advice: Start with the free county alert. If you fall into a high-risk category, then a paid service is a reasonable and affordable layer of extra security.

Master Your Finances, One Skill at a Time

Enjoying these protective strategies? Get more actionable money moves like this delivered straight to your inbox.

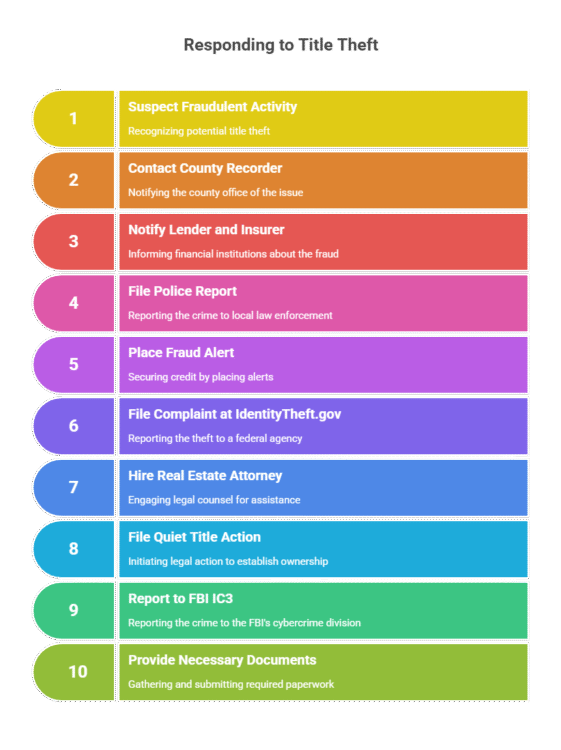

Responding to Title Theft: What to Do if You’re a Victim

If you suspect or confirm fraudulent activity:

Act Immediately:

- Contact your county recorder’s office

- Notify your mortgage lender and title insurance company

- File a police report and keep a copy

- Place a fraud alert or freeze on your credit

- File a complaint at IdentityTheft.gov

Begin Legal Action:

- Hire a real estate attorney to challenge the fraudulent deed

- File a quiet title action to legally establish rightful ownership

- Report the crime to:

- Your local police

- Your state Attorney General’s office

- The FBI’s Internet Crime Complaint Center (IC3)

You’ll Need to Provide:

- A copy of your original deed

- Government-issued ID

- Fraudulent documents

- Any communications or notices related to the fraud

Can someone really steal my house without me knowing?

Yes. Criminals don’t need your keys or to be physically present. By forging your signature on a fraudulent deed and filing it with the county recorder, they can illegally transfer the legal title of your property into their name, often without any initial notification to you.

Is title insurance the same as a “title lock” service?

No. Title insurance protects you against ownership claims or title defects from the past (before you purchased the home). It does not protect against fraud that occurs after you own the property. Paid title lock services simply monitor your property records for new filings, a service most counties now offer for free.

How can I check if my home’s title is in my name?

You can check your property’s title and ownership records for free. Simply visit your county recorder’s, clerk’s, or assessor’s office website and search the public property records database using your name o

Explore next steps like identity theft recovery, preventing wire transfer fraud during real estate deals, or how to update your estate plan after title changes. Now, try searching for topics such as ‘real estate scam prevention,’ ‘recovering from financial fraud,’ or ‘estate planning for homeowners.’

Your Next Steps for Protecting Your Home’s Title: Michael Ryan’s Parting Comments

Ultimately, protecting your home from title fraud isn’t about buying a complicated service; it’s about practicing simple, proactive awareness. You now know the free, effective steps to monitor your property records and freeze your credit. The two most powerful shields you have against this devastating crime.

After years of helping clients secure their futures, I can assure you that the peace of mind that comes from these small, one-time actions is immeasurable. You’ve turned your most valuable asset into a secure fortress.

Don’t let your financial diligence end here. Keep scrolling to discover more strategies for protecting your assets and building wealth. And for more of my experience-backed insights on navigating the financial world, sign up for my weekly newsletter..

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.