Rebuild credit by slashing your utilization ratio—it’s the single fastest path to a better credit score.Ever felt like your credit score is a black box, rigged against you? You’re not alone. The national average FICO score dropped to 702 in 2026 [cite: Experian, January 2026], the steepest decline since the Great Recession. With millions feeling the squeeze from resumed student loan payments and high credit card balances.

But forget the jargon for a second. Your credit utilization ratio, the percentage of available credit you use, is simply the number that screams “risk” or “responsibility” to a lender.

I’ve seen a single percentage point in this number be the difference between a mortgage approval and a denial.

This isn’t just another list of generic tips. This is a myth-busting, step-by-step blueprint for 2026, built on decades of experience and informed by critical new changes. Like the removal of medical debt and the inclusion of Buy Now, Pay Later (BNPL) data in your score. Let’s get it right.

Key Takeaways: Your 60-Second Credit Utilization Action Plan

- The 30% Rule is Obsolete:

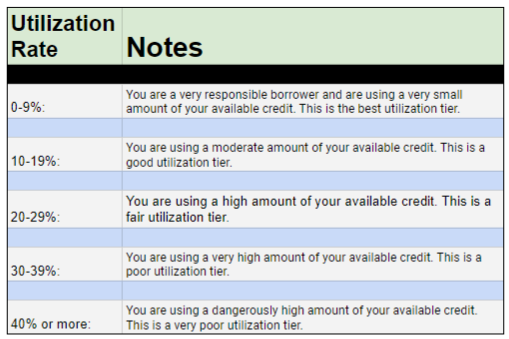

For the highest scores, aim for a credit utilization ratio under 10%. Consumers with perfect credit scores average around 6% utilization. - Payment History is King:

Your track record of on-time payments makes up 35% of your FICO score. Setting up autopay for at least the minimum is non-negotiable. - Timing is Everything:

Your balance is typically reported to the credit bureaus on your statement closing date, not your payment due date. Pay your balance before the statement date for the biggest score impact. - Leverage New Data:

You can now boost your score with alternative data. Services like Experian Boost and rent reporting can add your on-time utility and rent payments to your credit file. - Never Close Old Cards:

Closing an old credit card hurts your score by increasing your overall utilization ratio and shortening the average age of your credit history.

Key Takeaways Ahead

The 2026 Credit Reality Check: What’s Changed This Past Year?

The credit landscape is shifting under our feet. Here are the market forces you need to understand:

- Student Loan Delinquencies:

With COVID-19 forbearance over, late payments on student loans are now being reported again, pulling down scores. - Medical Debt Removal:

As of March 17, 2025, a new CFPB (Consumer Financial Protection Bureau) rule mandates that paid medical collections be removed from credit reports, offering a potential score boost for millions. This was later reversed and overturned by the courts! - Buy Now, Pay Later (BNPL) Integration:

Starting in Fall 2025, FICO began incorporating BNPL loan data into its scoring models. Responsible use can build credit, but multiple BNPL accounts opened quickly could be flagged as risky behavior. - Alternative Data is Mainstream:

VantageScore 4.0, now used in some mortgage applications, can include rent and utility payment history, giving you new ways to build a positive record.

Phase 1: Your 30-Day Foundation & Assessment

Step 1: Get Your Credit Reports (For Free)

Before you can fix the problem, you need to see it clearly. Go to AnnualCreditReport.com, the only federally authorized source, and pull your full credit reports from all three major credit bureaus: Experian, Equifax, and TransUnion.

You are entitled to a free report from each bureau every week.

Step 2: Dispute Errors Strategically

Carefully review each report for inaccuracies. According to a Consumer Reports study, over a third of consumers find errors in credit reports. Look for incorrect balances, accounts that aren’t yours, or late payments you made on time.

📉 Bad Advice to Ignore

Avoid credit repair companies that promise to remove accurate negative information. This is illegal under the **Credit Repair Organizations Act (CROA)**. They often flood bureaus with frivolous disputes that can backfire. You can dispute legitimate errors yourself for free through the credit bureaus’ online portals.

Phase 2: Mastering Payment History (The 35% Factor)

Your payment history is the heavyweight champion of your credit score, accounting for a massive 35% of your FICO score. One 30-day late payment can drop an otherwise good score by over 100 points.

Your payment history is the heavyweight champion of your credit score, accounting for a massive 35% of your FICO score. One 30-day late payment can drop an otherwise good score by over 100 points.

Your Action Plan:

- Set Up Autopay:

Log in to every single one of your credit accounts today and set up automatic payments for at least the minimum due. This is your ultimate safety net. - Align Due Dates:

Call your creditors and ask them to move your payment due dates to a day or two after you get paid. This simple logistical change prevents “accidental” late payments.

Credit Utilization Mastery (Why 10% is the New 30%)

This is the second most important factor, making up 30% of your FICO score.

It’s also the fastest way to see a significant score increase.

The Statement Date vs. The Due Date

This is the secret weapon. Most people think their balance is reported on the due date. Wrong.

Most card issuers report whatever your balance is on the statement closing date.

💡 Michael Ryan Money Tip

To slash your reported utilization, make a payment *before* your statement closing date. For example, if your statement closes on the 20th and your due date is the 15th of the next month, paying down the balance on the 18th will ensure a low (or zero) balance is reported to the bureaus, even if you used the card all month.

Advanced Utilization Strategies

- Request Credit Limit Increases:

Every 6-12 months, request a credit limit increase on your existing cards. A higher limit instantly lowers your utilization ratio, as long as you don’t increase your spending. A soft-pull request (which doesn’t affect your score) is preferable to a hard-pull. - Become an Authorized User:

If you have a trusted family member with a long history of on-time payments and a low utilization ratio on their card, ask to become an authorized user. Their good history will be added to your credit file, often providing a quick boost.

Credit Rebuilding Myths Busted: The Truth vs. The “Hacks”

⚠️ Myth Busted: “You should keep a small balance to build credit.”

Reality: This is completely false and costs you money in interest. Paying your statement balance in full every month demonstrates perfect credit management and is the most powerful way to build a strong score over time.

⚠️ Myth Busted: “Closing old credit cards will help my score.”

Reality: This is one of the worst mistakes you can make. Closing a card, especially an old one, does two negative things: it reduces your total available credit (instantly increasing your utilization ratio) and it shortens your **credit age** (15% of your score).

⚠️ Myth Busted: “Zero utilization is the best.”

Reality: While a 0% reported balance is great, some scoring models, like certain versions of FICO, may actually give slightly fewer points for 0% utilization across all cards versus having one card report a very small balance (e.g., $5). This shows you are actively using credit responsibly. This advanced technique is known as **AZEO (All Zero Except One)**.

Advanced Credit Utilization Strategies: The Pro-Level Moves for 2026

Leverage Alternative Credit Data

If you have a thin credit file, this is a game-changer.

- Rent Reporting:

Services can add your on-time rent payments to your credit reports. VantageScore data shows this can cause “large, statistically significant increases” in scores. - Experian Boost:

This free service connects to your bank account and adds on-time utility, cell phone, and streaming service payments to your Experian credit file.

Optimize Your Credit Mix (10% of Your Score)

Lenders like to see that you can responsibly manage different types of debt. A healthy credit mix includes both revolving credit (like credit cards) and installment loans (like an auto loan, mortgage, or a credit-builder loan).

Action Plan by Credit Score Range: Your Personalized Roadmap

Scores Below 580 (Poor Credit)

- Get a Secured Credit Card: This is your top priority. You provide a small security deposit (e.g., $200) which becomes your credit limit. It’s the safest way to start building a positive payment history.

- Add a Credit-Builder Loan: Open a small credit-builder loan from a local credit union.

- Focus Only on Payments: For the first 6-12 months, your only job is to make every single payment on time. Don’t worry about utilization yet.

Scores 580-669 (Fair Credit)

- Optimize Utilization: Now, your focus shifts. Get all credit card balances below 30%, with a target of under 10%.

- Request Limit Increases: Ask for credit limit increases on your existing cards.

- Become an Authorized User: If possible, get added to a trusted family member’s card.

Scores 670+ (Good to Excellent Credit)

- Aim for Perfection: Implement the multiple payment and AZEO strategies to keep your reported utilization in the low single digits.

- Leverage Your Score: Now is the time to shop for the best rates on mortgages or auto loans, as your strong credit gives you negotiating power.

Credit Utilization Frequently Asked Questions (FAQ)

What is the fastest way to improve my credit score?

The fastest way is to pay down your credit card balances to get your credit utilization ratio below 10%. This can improve your score in as little as 30-45 days, a strategy detailed in our guide on the 15/3 credit hack.

Does closing a credit card hurt your score?

Yes, in almost all cases. It increases your utilization and reduces your credit age. The only time to consider closing a card is if it has a high annual fee and you are not getting value from it.

How often should I pay my credit card bill?

You are only required to pay once per month before the due date. However, for score optimization, making a payment before your statement closing date is the key to lowering your reported utilization.

What is the difference between a FICO score and VantageScore?

They are two different credit scoring models created by competing companies. While both use similar data from your credit reports, they weigh factors differently. FICO is more widely used by lenders, especially for mortgages, while VantageScore is often seen on free credit monitoring sites.

For a deeper dive, see our guide on FICO vs. VantageScore: What’s the Difference?.

Can requesting a credit limit increase hurt my credit score?

It depends. A soft pull inquiry (where the card issuer doesn’t check your credit) won’t affect your score at all. However, a hard pull inquiry may temporarily lower your score by a few points. The good news: the positive impact of a higher credit limit (lower utilization ratio) typically outweighs the small dip from the inquiry. After 6-12 months, the inquiry falls off, but the higher limit benefit remains.

How long does it take to see credit score improvements from lower utilization?

You can see improvements within 30-45 days after your new lower balance is reported to the credit bureaus. Most credit issuers report balances on your statement closing date, so if you pay down your balance before that date, the improvement can appear on your next score update. However, significant improvements typically take 2-3 billing cycles to be fully reflected. Your payment history and other factors take longer to improve (months to years), but utilization changes are one of the fastest wins.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.