Have you ever asked yourself, “Can I have a Roth IRA and a 401(k)?” If so, you’re asking the right question, but it’s only half the story. After nearly 3 decades as a financial planner, I’ve found the real question isn’t if you can have both, but in what order you should fund them to build wealth the fastest.

The good news is, yes, you can absolutely contribute to both a Roth IRA and a 401(k) in the same year. The challenge is dealing with terms like ‘company match‘ and ‘tax brackets‘ to create a strategy that works for you.

This guide is my playbook. We’ll simplify the rules, compare the accounts head-to-head, and I’ll give you the exact, step-by-step contribution strategy I’ve used with hundreds of clients to build tax-free wealth.

Quick Links: Choosing Between a Roth 401k or Roth IRA

Key Takeaways: The 60-Second Explainer of Roth IRA & 401k

- Dual Contribution is Allowed:

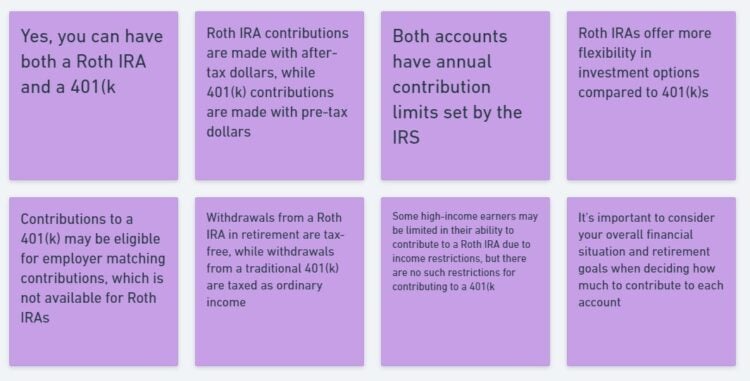

Yes, you can contribute to both a Roth 401(k) and a Roth IRA in the same year, as long as you meet the eligibility rules for each. Their contribution limits are separate. - Top Priority:

Always contribute enough to your 401(k) (Roth or Traditional) to get the full employer match. It’s a 100% return on your money and the best deal in finance. - Roth IRA’s Superpower:

Flexibility. You can withdraw your contributions (not earnings) at any time, tax- and penalty-free, making it a powerful emergency fund. It also has no Required Minimum Distributions (RMDs) for the original owner. - Roth 401(k)’s Superpower:

High contribution limits. For 2026, you can save up to $24,500 (plus an $8,000 catch-up if you’re 50 or older), which is more than three times the IRA limit. - The Optimal Strategy:

For most people, the best approach is a sequence: 1) Contribute to your 401(k) up to the employer match. 2) Fully fund your Roth IRA. 3) Return to your 401(k) to contribute any additional savings up to the maximum.

The Contribution Priority Rule: Where to Put Your First Dollar

Let’s cut right to the chase. The most common question I get is, “After my employer match, where should my next dollar go?” For most people, the answer follows a simple but powerful hierarchy.

💡 Michael Ryan Money Tip: The Optimal Contribution Flowchart

- Secure the Match: Contribute to your 401(k) (Roth or Traditional) just enough to get 100% of your employer’s matching funds. Not doing this is like turning down a raise.

- Max the Roth IRA: Shift your focus and contribute up to the annual maximum in a Roth IRA. This secures your flexible emergency fund and gives you access to better, lower-cost investments.

- Return to the 401(k): If you still have money to save after maxing out your Roth IRA, go back to your 401(k) and contribute up to its much higher limit to maximize your tax-advantaged savings.

Head-to-Head Comparison: Roth 401(k) vs. Roth IRA for 2026

Both accounts are funded with after-tax dollars, meaning you get no upfront tax deduction, but in exchange, your qualified withdrawals in retirement are 100% tax-free. However, the rules governing them are quite different.

| Feature / Aspect | Roth IRA | Roth 401(k) |

|---|---|---|

| 2026 Contribution Limit | $7,500 (+$1,100 catch-up if 50+) | $24,500 (+$8,000 catch-up if 50+) |

| Income Limits (MAGI) | Yes (Phase-out starts ~$153k single) | No income limits |

| Employer Match | Not applicable | Yes (Match is always pre-tax) |

| Investment Choices | Nearly unlimited (stocks, bonds, ETFs, etc.) | Limited to your plan’s menu (usually 10-20 funds) |

| Contribution Withdrawals | Can be withdrawn anytime, tax- and penalty-free | Governed by plan rules; often restricted |

| Required Minimum Distributions (RMDs) | No RMDs for the original owner | No RMDs (per SECURE 2.0 Act) |

Investment Options: The Battle of Choice vs. Simplicity

One of the most significant differences lies in your investment freedom.

Roth 401(k):

Your investment options are limited to the menu of funds selected by your employer. This is simple, but you might be stuck with a small selection of high-fee, underperforming funds.

Roth IRA:

You have access to a nearly unlimited universe of investments. You can open an account at a low-cost brokerage like Vanguard or Fidelity and buy individual stocks, thousands of ETFs, bonds, REITs for real estate exposure, or even alternative investments.

📌 Key Takeaway

The average 401(k) plan has fees that are nearly double that of a self-directed IRA. If your employer’s 401(k) plan is expensive, prioritizing a low-cost Roth IRA after getting your match becomes an even smarter financial move for your long-term asset allocation.

Withdrawal Rules & Flexibility: Accessing Your Money

This is where the Roth IRA truly shines, especially before retirement.

The Roth IRA’s “Secret” Emergency Fund

You can withdraw your direct contributions (not earnings) from a Roth IRA at any time, for any reason, without taxes or penalties. This makes it a uniquely flexible account that can double as a powerful emergency fund.

The 5-Year Rule

For withdrawals of earnings to be qualified (tax and penalty-free), you must be at least 59½ years old AND your first Roth IRA must have been open for five years. This 5-year rule is a critical piece of Roth IRA withdrawal planning.

Roth 401(k) Rollovers

What happens to your Roth 401(k) when you leave your job? You can, and often should, roll it over into your Roth IRA. This consolidates your accounts, expands your investment choices, and ensures you avoid any plan-specific administrative fees.

Advanced Strategies for High Earners: The Backdoor Roth Playbook

What if your Modified Adjusted Gross Income (MAGI) is too high to contribute to a Roth IRA directly? This is where the Backdoor Roth IRA comes in.

Special Considerations: Self-Employed and Pre-Retirees

For the Self-Employed: The Solo 401(k)

If you’re an entrepreneur or freelancer, you can open a Solo 401(k). This powerful account allows you to act as both “employee” and “employer,” contributing up to the employee maximum ($24,500 in 2026) plus a percentage of your business profits. Most Solo 401k plan providers now offer a Roth option, giving you the same high contribution limits as a corporate plan.

For Pre-Retirees (Age 50+): The Catch-Up Contribution

The IRS allows those age 50 and over to make additional “catch-up” contributions. For 2026, that’s an extra $8,000 for a 401(k) and $1,100 for an IRA. A new rule from the SECURE 2.0 Act, effective in 2026, mandates that if you earn over $150,0000, your 401(k) catch-up contributions must be made on a Roth (after-tax) basis.

Frequently Asked Questions (FAQ)

Should I max out my Roth IRA or Roth 401(k) first?

After contributing enough to your 401(k) to get the full employer match, most financial planners recommend prioritizing the Roth IRA. Its superior flexibility, wider investment choices, and freedom from RMDs make it an incredibly powerful tool for your personal finances.

Is my employer’s 401(k) match also Roth (tax-free)?

No. This is a critical point many miss. Employer matching funds are always deposited on a pre-tax basis. This means you will have two pots of money in your 401(k): your Roth contributions (tax-free) and your employer’s traditional contributions (taxable upon withdrawal)

What if my income is too high to contribute to a Roth IRA?

If your MAGI is above the income limits for a Roth IRA, you cannot contribute directly. Your options are to contribute the maximum to your Roth 401(k) and/or execute the Backdoor Roth IRA strategy.

Can I contribute to both a Roth 401(k) and a Roth IRA in the same year?

Yes, absolutely. The contribution limits are separate. As long as you meet the income requirements for the Roth IRA, you can contribute to both accounts simultaneously.

Now, try searching for: Roth 5-Year Rule, Backdoor Roth IRA, RMD Rules.

My Final Verdict & Your Action Plan

The decision between a Roth 401(k) and a Roth IRA isn’t about choosing a “winner.” It’s about using the right tool for the right job in the right order. By following the simple priority rule. Match first, then IRA, then 401(k). You capture the best of both worlds: the free money from your employer, the flexibility and choice of the IRA, and the high contribution limits of the 401(k).

Additional Sources used in this article

- IRS guidelines on Retirement plan contribution limits

- Details on Roth IRA rules from the Securities and Exchange Commission

- Best practices for saving for retirement – AARP guidelines

- Retirement Plans FAQs Regarding IRAs: IRS

- Roth IRA: IRS

- Is the Distribution From My Roth Account Taxable? | Internal Revenue Service

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.