In my 25+ years as a planner, I’ve seen more families financially crippled by what was not in their homeowner’s policy than by stock market crashes. Not only do I live in South Florida, but so do many of my clients. So unfortunately, I know more than most about Homeowners Insurance policies, and what to look out for.

I’ll never forget “the Millers,” a client couple whose kitchen was destroyed in a grease fire. They thought their policy had them covered. But they were about to make a $30,000 mistake by cashing the first check from the adjuster. Not realizing it was for the Actual Cash Value (the garage-sale price) of their 15-year-old cabinets, not the full Replacement Cost to buy new ones.

This guide isn’t about defining insurance; it’s a playbook, built from decades of client crises, to ensure you’re not just ‘covered,’ but truly protected.

🤔 Things to Ponder

When I started as a planner, I realized clients didn’t just want to know what a policy was; they wanted to know what the different parts meant in plain English and how to avoid getting taken advantage of after a disaster. This guide is built to answer that core question: “Will my insurance actually work when I need it most?”

Key Takeaways Ahead

What is Homeowners Insurance? (The 30-Second Explanation)

Homeowners insurance is a property-casualty contract that transfers catastrophic financial risk—structure damage from fire or wind, personal liability from injuries on your property—from you to an insurer in exchange for premiums calculated using ISO (Insurance Services Office) rating models, your CLUE claims history report, and zip-code loss ratios. Here’s the reality most agents won’t tell you: In 2025, the average HO-3 policy costs $2,377 annually nationwide, but in high-risk states like Florida ($6,000+), Louisiana ($4,500+), and Colorado ($3,200+), climate-driven losses have pushed premiums to historic highs while major carriers like State Farm and Allstate have stopped writing new policies entirely in some markets.

The critical difference between a policy that works and one that leaves you financially devastated comes down to understanding three concepts most homeowners get wrong: replacement cost vs. actual cash value, coverage limits vs. sub-limits, and which perils are actually covered. Let’s break down exactly what you’re paying for.

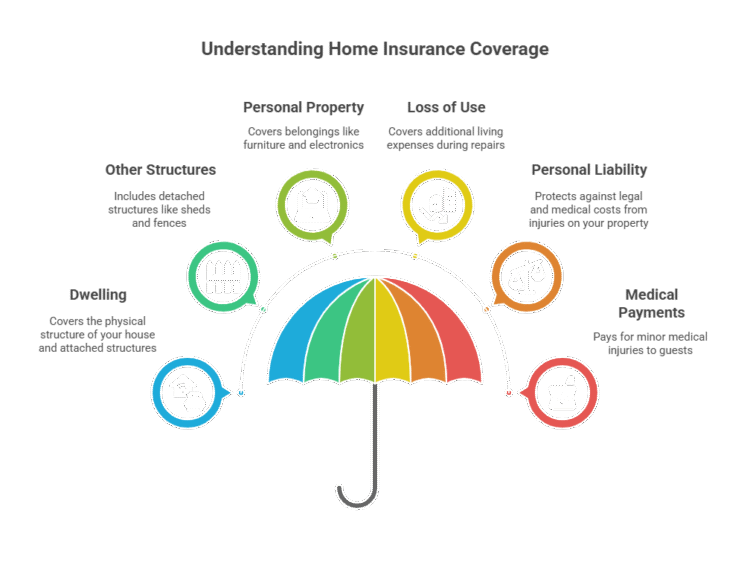

Understanding Your Policy: The 6 Core Types of Homeowners Insurance Coverage

Every standard homeowners insurance policy (often called an HO-3 policy) is built on six fundamental pillars of coverage. Understanding these is non-negotiable.

💡 Michael Ryan Money Tip

Don’t just glance at your policy’s declaration page. Read the definitions for each coverage type. These six sections are the DNA of your financial protection, and knowing what they mean is the first step to ensuring you have a policy that will actually work when you need it.

Homeowners Insurance Coverage Types

| Coverage Type | What It Covers | Michael Ryan’s Expert Take |

|---|---|---|

| A: Dwelling | The physical structure of your house and attached structures (like a garage). | Your dwelling coverage amount should be based on the cost to rebuild, not your home’s market value. Call a local contractor and ask for the current per-square-foot build cost in your zip code. Anything less is gambling. |

| B: Other Structures | Detached structures on your property, like a shed, fence, or guest house. | This is usually set at 10% of your dwelling coverage. If you’ve built a high-end workshop or a detached office, you will likely need to increase this limit. |

| C: Personal Property | Your belongings—furniture, electronics, clothing, etc.—from covered perils. | This is where insurers get you with sub-limits. A standard policy might cap jewelry theft at $2,500. If you have a $15,000 engagement ring, you need a separate “scheduled personal property” rider to be fully covered. |

| D: Loss of Use (ALE) | Your Additional Living Expenses (ALE) if your home is uninhabitable during repairs. | This covers costs like hotel bills and restaurant meals above your normal spending. With post-disaster repair delays common, ensure your limit is at least 20-30% of your dwelling coverage. |

| E: Personal Liability | Legal and medical costs if someone is injured on your property and you’re found liable. |

The standard $100k liability is a joke in 2025. Your liability coverage should, at a minimum, equal your calculable net worth. If your net worth is over $500k, you need a separate Umbrella Liability Policy. Think of it as a secondary liability policy that kicks in after your primary homeowners and auto insurance limits are exhausted. A $1 million umbrella policy can cost as little as $20-$30 per month and is the most cost-effective way to protect your assets from a major lawsuit. |

| F: Medical Payments | Pays for minor medical injuries for guests on your property, regardless of fault. | This is “goodwill” coverage. It’s meant to quickly pay for a minor incident (like a friend tripping on a step) to avoid a larger liability claim. A $5,000 limit is typical. |

Beyond the Obvious: The Inflation-Proofing Endorsement

In today’s high-inflation environment, even setting the right rebuild cost isn’t enough. Construction material and labor costs can surge between the day you buy your policy and the day you file a claim. That’s why the single most important endorsement you can add in 2025 is ‘Extended Replacement Cost.’

This provides an extra 25% or 50% buffer on top of your dwelling coverage. If your home is insured for $400,000, this endorsement gives you up to $500,000 for a rebuild—a critical cushion against inflation that most homeowners don’t know exists.

HO-1 to HO-8: Choosing the Right Homeowners Insurance Policy Form

While the HO-3 is the most common, several other policy “forms” exist for different living situations. Knowing the difference is key to not over or under-insuring.

Homeowners Insurance Policy Forms

| Policy Form | Who It’s For | Key Feature |

|---|---|---|

| HO-3 (Special Form) | Most homeowners | Provides “open peril” coverage for your dwelling and “named peril” for personal property. This is the industry standard. |

| HO-5 (Comprehensive) | Owners of high-value homes | The gold standard. Provides “open peril” coverage for both your dwelling and your personal property for maximum protection. |

| HO-4 (Contents Form) | Renters | Covers personal property and liability, but not the building itself. Commonly known as renters insurance. |

| HO-6 (Unit-Owners Form) | Condo Owners | Covers the interior of your unit (“walls-in”), your personal property, and liability. Your condo association’s policy covers the building exterior. |

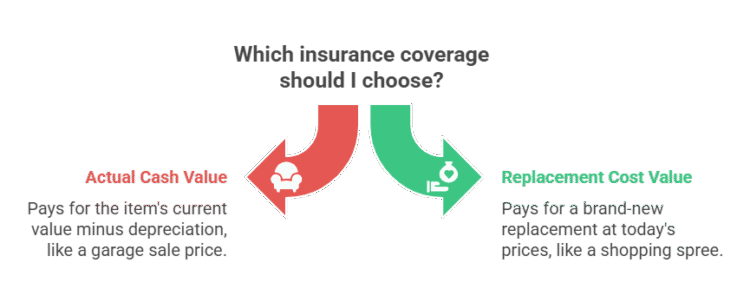

Replacement Cost vs. Actual Cash Value: The $30,000 Mistake

This is the single most important, and most misunderstood, concept in your entire policy. Getting this wrong can be financially devastating.

Actual Cash Value (ACV):

This coverage pays you for the value of your damaged item minus depreciation. Think of it as the “garage sale” price. Your 10-year-old sofa may have cost $2,000, but its ACV might only be $200.

Replacement Cost Value (RCV):

This coverage pays you the full amount required to replace the damaged item with a brand-new, similar item at today’s prices. It’s the “shopping spree” coverage.

🔍 Explained SimplyWith Actual Cash Value, you get a check for what your old stuff was worth. With Replacement Cost Value, you get a check for what new stuff will cost. Always opt for RCV for your dwelling and, ideally, for your personal property; the small extra premium is worth every penny.

📘 Client Story

Conversely, I had a client whose home was a total loss in a wildfire. Because they had paid a few extra dollars a month for guaranteed Replacement Cost Value, they received a check for the full amount to rebuild their home at today’s inflated construction costs. It was a lifeline that allowed them to fully recover without draining their retirement savings.

What Homeowners Insurance Does Not Cover: Common Exclusions

Your policy is not a magic shield against everything. Standard policies almost always exclude:

- Floods:

Damage from flooding requires a separate policy, typically from the National Flood Insurance Program (NFIP). - Earthquakes:

This also requires a separate policy or endorsement. - Maintenance Issues:

Damage from wear and tear, mold, termite infestations, or a leaky faucet is considered your responsibility. - Sewer Backup:

Damage from a backed-up sewer or drain line is often excluded unless you add a specific “water backup” endorsement.

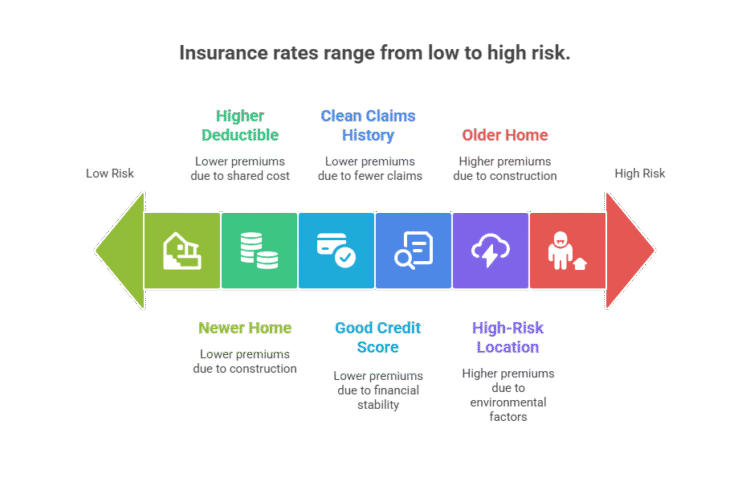

How Insurance Companies Determine Your Rates in 2025

Insurers are in the business of risk management, and their rates are determined by a complex algorithm that assesses how likely you are to file a claim. Key factors include:

- Location:

High-risk areas for hurricanes, wildfires, or crime will have higher rates. - Construction & Age of Home:

A newer, masonry home will be cheaper to insure than an older, wood-frame one. - Your Deductible:

A higher deductible (the amount you pay out-of-pocket on a claim) will lower your premium. - Your Credit-Based Insurance Score:

In most states, insurers use a score similar to your credit score to predict risk. AA practice explained by the National Association of Insurance Commissioners (NAIC), to predict risk. - Your Claims History (The CLUE Report):

- This is the one most people don’t know about. Insurers share your claims history through a database called the CLUE (Comprehensive Loss Underwriting Exchange) report.

💡 Michael Ryan Money Tip

Don’t just shop for the lowest price. A cheap policy from a financially unstable company is worthless in a widespread disaster. Before you buy, check an insurer’s financial strength rating from a service like AM Best. A rating of “A” or higher indicates a company has an excellent ability to pay its claims.

Everyone thinks a low deductible is better. This is a psychological trap. Filing a minor $1,500 claim could raise your premiums by 10-20% for years via your CLUE report, costing you far more than the original claim. My advice: Set your deductible as high as you can comfortably afford to pay from your emergency fund. Your insurance is for catastrophes, not inconveniences.

⚠️ The 2025 Insurance Market Crisis Nobody’s Talking About

Here’s what your agent won’t tell you: Between Hurricane Ian ($112B in losses), the Maui wildfires ($5.5B), and back-to-back atmospheric rivers in California, insurance companies paid out record catastrophic losses in 2023-2024. The result? State Farm and Allstate stopped writing new policies in Florida and California—not because of regulation, but because actuarial models show those markets are now mathematically unprofitable at current premium levels.

If you’re in a high-risk zip code and your carrier non-renews you, your only option may be your state’s “insurer of last resort” (Citizens Property Insurance in Florida, FAIR Plan in California)—which typically costs 2-3x more with significantly reduced coverage limits. Translation: The time to audit your policy and confirm your carrier’s AM Best financial strength rating isn’t after the next disaster—it’s right now.

How to File a Homeowners Insurance Claim (And Not Get Lowballed)

- Document Everything Immediately:

Take dozens of photos and videos of the damage before you move anything. - Contact Your Insurer Promptly:

Call the claims number on your policy to get the process started. - Mitigate Further Damage:

If you have a hole in your roof, put a tarp over it. These reasonable costs are usually reimbursable. - Keep a Detailed Log:

Document every conversation with your adjuster, including the date, time, and what was discussed. - Get Independent Estimates:

Do not rely solely on the adjuster’s contractor. Get at least two independent quotes for repairs. For more on this, see our guide on home insurance claim adjuster tactics.

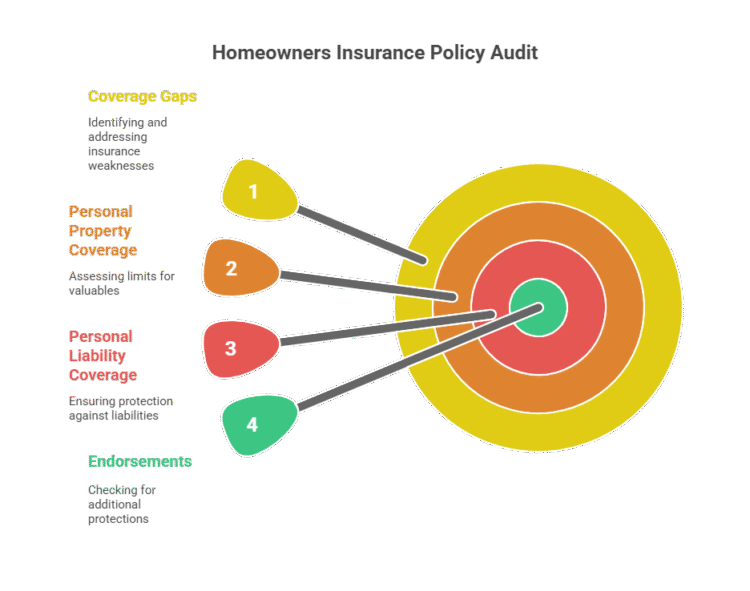

How To Audit Your Own Policy In 10 Minutes

Stop reading and pull out your policy’s declaration page right now. Let’s find the weak spots.

Your 10-Minute Policy Weakness Audit

- Check Box C (Personal Property):

Find the “Special Limits of Liability.” Do you see a low number for Jewelry, Electronics, or Business Property? If you own items worth more than that limit, you have a major coverage gap. - Check Box E (Personal Liability):

Is this number lower than your total net worth? If yes, you are underinsured. - Find the “Endorsements” Section:

Do you see the words “Replacement Cost for Personal Property” and “Water Backup Coverage”? If not, you likely have the cheaper (and less effective) Actual Cash Value coverage and are exposed to one of the most common and costly types of home damage

Frequently Asked Questions about Homeowners Coverage

Does homeowners insurance cover dog bites?

Yes, the liability portion of your policy typically covers dog bites. However, some insurers exclude certain breeds or may non-renew your policy after a bite claim.

How much homeowners insurance do I need?

You need enough dwelling coverage to completely rebuild your home, enough liability coverage to protect your net worth, and enough personal property coverage to replace your belongings.

- My Prediction for 2027:

The future of homeowners insurance isn’t just about covering events; it’s about preventing them.

Expect insurers to offer significant premium reductions for installing IoT (Internet of Things) devices like automatic water shut-off valves and smart smoke detectors that are directly linked to their monitoring systems.

Final Verdict: Your Home’s Financial Fortress

Your homeowners insurance policy is one of the most important financial documents you will ever own. It’s not a commodity to be shopped for on price alone; it’s a fortress for catastrophes. By understanding these core concepts, you can move from feeling overwhelmed to empowered, ready to build a policy that truly protects your family and your future.

Disclaimer: This article is for informational purposes only and is not insurance or financial advice. Consult with a qualified, licensed insurance professional to discuss your specific needs.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.