I once had a new client, a sharp young engineer, who was proud of the “great deal” he got on his auto insurance. But when we dug into his policy, we found he was paying nearly $800 extra per year because he believed the myth of “full auto coverage“. A marketing term that left him dangerously exposed.

He learned the hard way that when it comes to auto insurance, what you think you know is often more expensive than what you don’t. The world of auto insurance is deliberately confusing, filled with half-truths and outdated advice.

In this definitive guide, we will systematically debunk the most common car insurance myths using hard data from sources like the Insurance Information Institute (III) and the NAIC. You’ll get the evidence-based facts you need to be a smarter shopper and a more confident policyholder.

Key Takeaways: Car Insurance Myths vs. Reality

- Insurance Follows the Car, Not the Driver:

If you lend your car to a friend and they cause an accident, it’s your insurance policy that takes the primary hit, putting your rates at risk. - Your Car’s Color is Irrelevant:

Insurers care about your car’s make, model, repair costs, and safety record (its VIN tells them everything)—not its paint job. The myth that red cars cost more is completely false. - “Full Coverage” is a Mythical Beast:

“Full coverage” is not an actual policy. It’s a slang term for a combination of Liability, Collision, and Comprehensive coverages, which still leaves significant gaps like rental reimbursement and GAP insurance. - Credit Scores Are a Powerful, and Legal, Rating Factor:

In most states, your credit-based insurance score is a major factor in determining your premium. Data shows it’s a strong predictor of future claims.

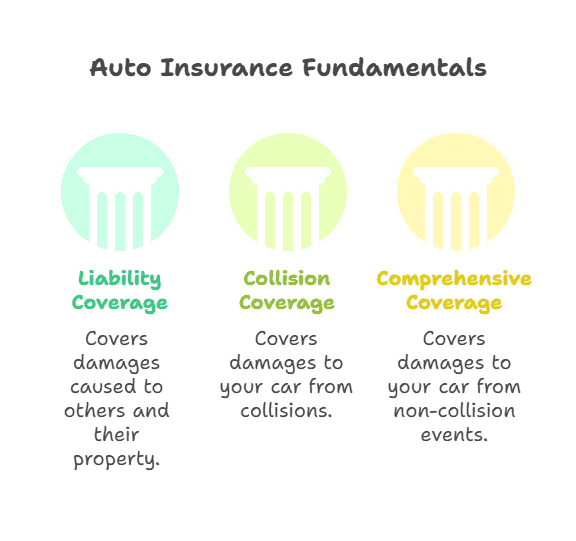

Auto Insurance 101: The 3 Core Coverages You Must Understand

Before we bust the myths, let’s get the fundamentals right. Most policies are built on three core coverage types. These coverage types ensure that individuals are adequately protected from unexpected events. To navigate these options effectively, it’s essential to consult a comprehensive insurance guide 2026 that elaborates on the distinctions and benefits of each type.

- Liability Coverage:

This covers damage you cause to other people and their property. It does nothing for you or your car. This is the coverage that is legally required by nearly every state. - Collision Coverage:

This covers damage to your car from a collision with another object (a car, a pole, a wall). This is what pays to fix or replace your car if you cause an accident. - Comprehensive Coverage:

This covers damage to your car from “other than collision” events. Think of it as bad luck insurance: theft, vandalism, hail, fire, or hitting a deer.

Myths About You, the Driver

Your personal characteristics are a huge part of the insurance premium equation. Let’s separate the facts from the fiction.

Myth #1: Older Drivers Always Pay More

- The Reality:

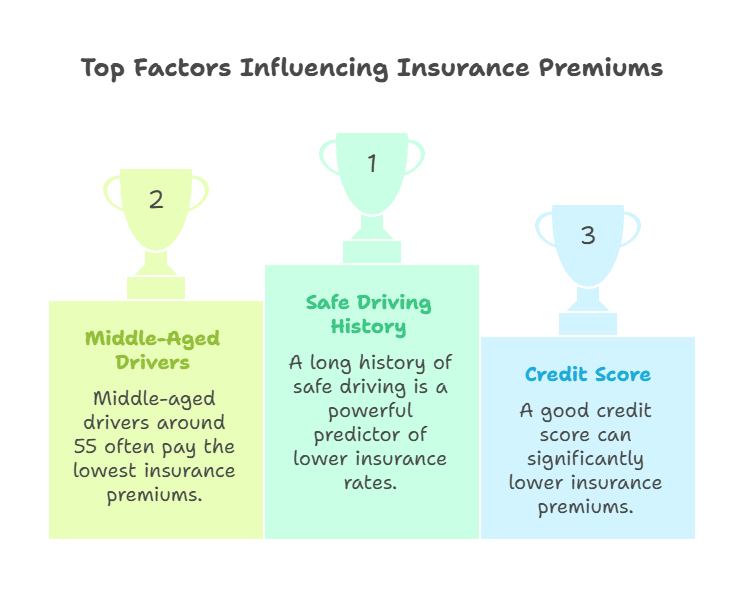

Middle-aged drivers (around 55) often pay the lowest premiums. While rates can increase for drivers over 75, most seniors benefit from decades of experience, a clean claims history, and lower annual mileage, leading to more favorable rates. - The Real Reason Why:

Insurance is a game of statistics. While age can correlate with certain risks, a long history of safe driving is a far more powerful predictor, and insurers reward that proven track record.

Myth #2: Your Credit Score Shouldn’t Affect Your Insurance Rate

- The Reality:

A Consumer Federation of America report found drivers with poor credit can pay over twice as much. Only 3 states: California, Hawaii, and Massachusetts currently ban this practice. - The Real Reason Why:

Insurers aren’t judging your character; they’re analyzing data. Decades of actuarial research show a strong statistical correlation between how a person manages their financial obligations (their credit) and their likelihood of filing a future claim. It’s a frustrating reality, but it’s a statistically proven one.

Myths About Your Car

From its color to its age, your vehicle is surrounded by insurance myths. Let’s clear them up.

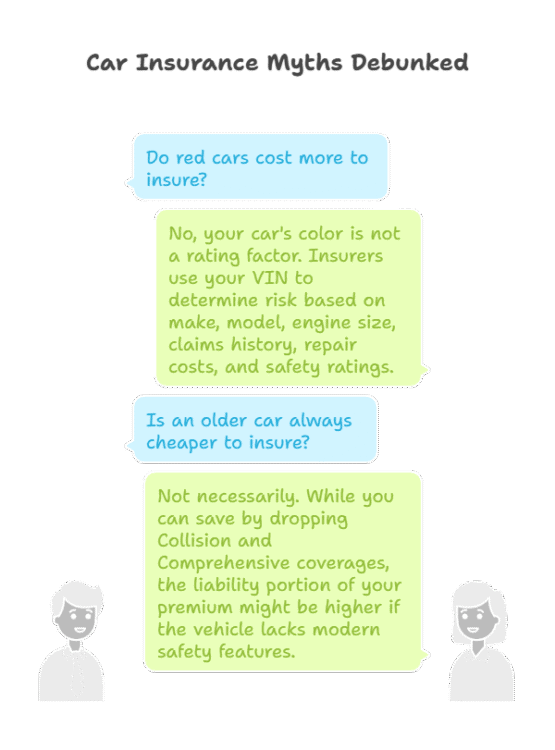

Myth #3: Red Cars Cost More to Insure

- The Reality:

This is 100% false. Your car’s color is not a rating factor. - The Real Reason Why:

Insurers use your Vehicle Identification Number (VIN) to determine risk. The VIN tells them the make, model, engine size, and, most importantly, provides access to data on that specific model’s claims history, average repair costs, and safety ratings from organizations like the Insurance Institute for Highway Safety (IIHS).

A boring grey car with a high theft rate will cost more to insure than a bright red one with excellent safety ratings.

Myth #4: An Older Car is Always Cheaper to Insure

- The Reality:

Not necessarily. While you can save by dropping Collision and Comprehensive coverages, the liability portion of your premium might be higher if the vehicle lacks modern safety features (like automatic emergency braking) that are proven to reduce accidents.

Myths About Your Policy & Coverage

This is where misconceptions can become truly expensive. Understanding what your policy actually covers is critical.

Myth #5: “Full Coverage” Means Everything is Covered

- The Reality:

“Full coverage” is not a real insurance product. It’s slang for a policy that bundles Liability, Collision, and Comprehensive.

Even with all three, you are likely not covered for rental car reimbursement, roadside assistance, or GAP insurance.

Myth #6: My Insurance Covers Me in Any Car I Drive

- The Reality:

Generally, insurance follows the car, not the driver. If you borrow a friend’s car and cause an accident, their auto insurance is the primary policy that must respond first.

Your insurance would only act as secondary coverage if the damages exceed their policy limits. This is a critical concept of “insurable interest.”

Myth #7: State Minimum Liability Coverage is Enough

- The Reality:

State minimums are dangerously low. A serious accident could easily exceed these limits, leaving you personally responsible for hundreds of thousands of dollars. The Federal Trade Commission (FTC) advises consumers to assess their assets to determine adequate coverage.

I advised my clients to carry a minimum of $100,000/$300,000 in bodily injury liability.

Emerging Myths for 2026 & Beyond: EVs, AI, and Telematics

As technology changes, so do the myths. Here’s what you need to know for the modern era.

Myth #8: Electric Vehicles (EVs) Are Always Cheaper to Insure

- The Reality:

While you save on gas, EV insurance can be more expensive.

Their high-tech components, especially battery packs, are extremely costly to repair after an accident, driving up the price of collision and comprehensive coverage.

Myth #9: Using Telematics (Usage-Based Insurance) Will Only Raise My Rates

- The Reality:

This is a common fear, but data shows the opposite. Usage-Based Insurance (UBI) programs, like Progressive’s Snapshot, reward safe driving habits (smooth braking, low mileage) with significant discounts.

They provide a more accurate risk assessment, allowing good drivers to pay less.

Frequently Asked Questions About Car Insurance

What is the difference between collision and comprehensive coverage?

Collision coverage pays for damage to your car from a collision with another object (like a car or pole). Comprehensive pays for damage from “other than collision” events, such as theft, vandalism, hail, or hitting an animal.

Does my insurance cover a rental car?

Typically, no. Rental car reimbursement is an optional add-on. However, your standard liability and comprehensive/collision coverages often do extend to a car you are renting, so you may not need to buy the expensive policy at the rental counter.

How can I lower my auto premium right now?

The fastest ways to potentially lower your car insurance premium are to increase your deductible, ask your agent for a list of all available discounts (like for bundling home and auto), and enroll in a usage-based insurance (telematics) program if you are a safe driver.

Conclusion: Your Action Plan for Smarter Car Insurance Shopping

Believing car insurance myths can cost you dearly. By focusing on the evidence-based factors that actually drive rates—your driving record, your vehicle’s safety profile, your credit-based insurance score, and your coverage limits. You can take control. Your next move? Pull out your current policy and review it against these myths.

A 15-minute review today could save you thousands tomorrow.

More resources For You

- “Understanding No-Fault Insurance by State”

- Resource: NAIC No-Fault Laws

- “How Traffic Tickets Affect Insurance Premiums”

- Resource: DMV.org traffic violation impacts

- “Comprehensive vs Collision Insurance Explained”

- Resource: U.S. Department of Transportation

- “Insurance Discounts: Fact vs Myth”

- Resource: Insurance Information Institute

- “The Role of Credit Scores in Car Insurance Rates”

- Resource: Consumer.govcredit basics

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.