You’ve been generous your whole life. In retirement, you continue to support the charities you care about, writing a check for a few thousand dollars each year. You feel good about it, and you assume your generosity is at least giving you a bit of a break on your taxes. But when you look at your tax return, nothing seems to change.

Worse, you just got a letter saying your Medicare premiums are going up due to IRMAA.

What’s going on? You’ve just stumbled into one of the most significant, yet poorly understood, consequences of the 2017 tax law changes.

As a financial planner for almost 30 years, this is a conversation I have constantly.

The hard truth is this: for the vast majority of retirees, your checkbook donations now provide zero federal tax benefit. You are getting no credit for your generosity. But there is a way to change that. The Qualified Charitable Distribution (QCD) is not just a different way to give; it’s a strategically superior tool designed to give you the tax benefit you deserve and protect you from IRMAA.

⚡ Key Takeaways

- The Standard Deduction Changed Everything: Since the standard deduction was nearly doubled, over 90% of retirees no longer itemize. If you don’t itemize, your cash donations do not reduce your taxable income at all.

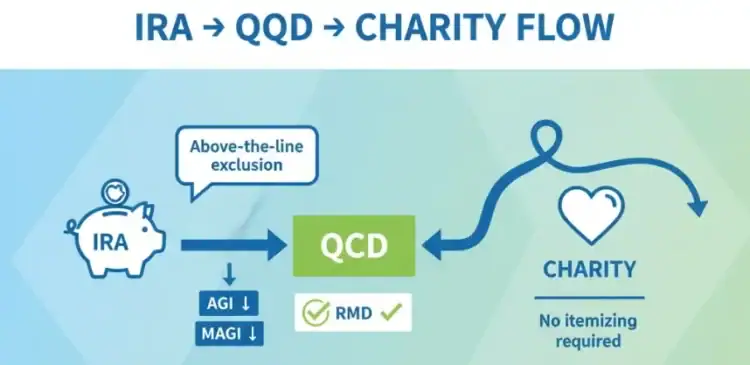

- Deduction vs. Exclusion: A standard donation is a “below-the-line” deduction, which only helps if you itemize. A QCD is an “above-the-line” exclusion, meaning the money never even appears on your income statement. This is a far more powerful benefit.

- QCDs Directly Lower Your MAGI: Because a QCD reduces your Adjusted Gross Income (AGI), it also reduces your Modified Adjusted Gross Income (MAGI) on a dollar-for-dollar basis. This is the key to avoiding IRMAA.

- A QCD Can Save You Money Even if a Cash Gift Wouldn’t: A QCD provides a direct income reduction that can save you thousands in taxes and Medicare premiums, a benefit you simply cannot get from a cash donation if you take the standard deduction.

Key Takeaways Ahead

The Problem: How the Standard Deduction Made Your Cash Donations Tax-Irrelevant

Prior to 2018, many clients “itemized” their deductions. You could add up your charitable gifts, mortgage interest, state and local taxes, and if the total was more than the standard deduction, you’d list them all out to lower your tax bill. However, the Tax Cuts and Jobs Act of 2017 dramatically increased the standard deduction.

The 2026 standard deduction rises to $32,200 for married filing jointly, $16,100 for single or married filing separately, and $24,150 for head For the official 2026 standard deduction amounts, see IRS Rev. Proc. 2024-40.of household; seniors 65+ get an extra $1,650 per qualifying spouse or $2,050 if single/head of household.

🧮 The Hard Math of a Non-Itemizer

Your Adjusted Gross Income (AGI) is calculated before you choose to take the standard or itemized deduction.

Since IRMAA is based on your MAGI (which starts with AGI), your cash donation does absolutely nothing to lower the income used for the IRMAA calculation. For the official rules, see IRS Publication 526, Charitable Contributions.

The Solution: How a QCD Bypasses the Standard Deduction Problem

A Qualified Charitable Distribution (QCD) is a direct transfer of funds from your IRA (if you are age 70½ or older) to a qualified charity. You never touch the money. Because of this, the IRS allows you to exclude that amount from your gross income. It’s not a deduction; it’s as if the income never existed in the first place.

This “above-the-line” adjustment is the secret weapon. It reduces your AGI directly, which in turn reduces your MAGI. It’s the only way for a non-itemizing retiree to get a tax benefit for their charitable giving, and it’s a critical part of any effective QCD IRMAA strategy.

📘 Client Story: The Couple Who Gave Smarter, Not More

I had clients, Jim and Betty, both 75. Their income from Social Security and RMDs gave them an AGI of $222,000. They gave $5,000 to their alma mater via check and took the standard deduction. Their MAGI was still $222,000, pushing them just over the 2024 IRMAA threshold of $218,000 for married filing jointly (which determines 2026 Medicare premiums).

The “Before” Scenario (Cash Gift):

AGI/MAGI: $222,000

Tax Benefit from Donation: $0 (they took the standard deduction)

IRMAA Surcharge for 2026: ~$1,950 ($81.20/month × 2 people × 12 months)

I had them switch their strategy. The next year, they made the same $5,000 donation as a QCD.

The “After” Scenario (QCD):

AGI/MAGI: $217,000 ($222,000 – $5,000 QCD)

Tax Benefit from Donation: $1,100 (avoided 22% tax on that part of their RMD)

IRMAA Surcharge for 2026: $0

By simply changing the source of the donation, they saved a combined $3,100 in taxes and pre

💡 Make Your Generosity Count (And Save Thousands)

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Learn the power of above-the-line deductions.

- → See how QCDs can eliminate IRMAA.

- → Get proven tax-saving retirement strategies.

💡 Stop wasting deductions & keep more of your retirement income

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Turn donations into real tax savings with timing and QCDs

- → Cut taxes on withdrawals and RMDs the smart way

- → Use year-by-year thresholds to avoid costly bracket creep

Get tax‑smart giving and retirement withdrawal tactics delivered straight to your inbox each week.

📬 No spam. Unsubscribe.

Head-to-Head: QCD vs. Standard Deduction

For retirees, the choice is clear. A QCD is superior in almost every way for managing the income that triggers Medicare surcharges.

Quick comparison: This table shows how a Qualified Charitable Distribution (QCD) stacks up against a regular cash donation for non‑itemizers. The key insight: QCDs can reduce AGI, satisfy RMDs, and help manage Medicare IRMAA, while typical cash gifts don’t move AGI and won’t help if you take the standard deduction.

| Feature | Qualified Charitable Distribution (QCD) | Cash Donation (Non‑Itemizer) | Impact | Notes |

|---|---|---|---|---|

| Reduces Your AGI/MAGI? | Yes. Dollar‑for‑dollar exclusion from income. | No. Has zero impact on AGI. | AGI ↓ | Helps with AGI‑based thresholds. |

| Requires Itemizing? | No. Available whether you itemize or not. | Yes. Benefit only applies if you itemize. | Itemize? → No/Yes | Standard deduction users favor QCDs. |

| Satisfies Your RMD? | Yes. Fulfills RMD obligation tax‑free. | No. Full taxable RMD still required. | RMD: ✓ / ✗ | Coordinate before taking other RMDs. |

| Helps Avoid IRMAA? | Yes. Lower AGI/MAGI can reduce IRMAA risk. | No. Does not affect AGI/MAGI. | IRMAA: ✓ / ✗ | Useful for Medicare surcharge planning. |

| Tip: For maximum impact, send QCDs directly from the IRA custodian to the qualified charity. For cash gifts to matter tax‑wise, donations must be large enough to beat the standard deduction and other itemized thresholds. | ||||

Action step: If you don’t itemize, prioritize QCDs for charitable giving and plan RMD timing early; cash gifts alone won’t lower AGI. Review your AGI, IRMAA exposure, and RMD schedule before year‑end.

Frequently Asked Questions

Can I still claim a deduction for the amount I gave via a QCD?

No, and you don’t need to. This would be “double-dipping.” The benefit of a QCD is that the income is excluded from your return entirely, which is more valuable than a deduction. You cannot both exclude the income and deduct the contribution.

What is the deadline for making a QCD for a given tax year?

The QCD must be processed and leave your IRA account by December 31st of the tax year. It’s wise to initiate the transfer with your IRA custodian no later than early December to ensure it is completed on time.

What if my RMD is larger than my charitable gift?

That’s a common scenario. If your RMD is $20,000 and you make a $5,000 QCD, that $5,000 is excluded from income. You are still required to withdraw the remaining $15,000 of your RMD, which will be taxed as ordinary income.

The QCD simply satisfies the first $5,000 of your RMD tax-free.

What are the 2026 IRMAA brackets and how does the two-year lookback work?

Your 2026 Medicare Part B and Part D premiums are based on your Modified Adjusted Gross Income (MAGI) from 2024 (the two-year lookback). The 2026 IRMAA brackets for married filing jointly are: $218,000 or less (standard premium of $202.90/month); $218,001-$274,000 (total $284.10/month); $274,001-$342,000 (total $405.80/month); $342,001-$410,000 (total $527.50/month); $410,001-$749,999 (total $649.20/month); and $750,000+ (total $689.90/month). For single filers, the brackets are half these amounts ($109,000, $137,000, $171,000, $205,000, $500,000+). This is why QCDs are so valuable – they reduce your 2024 MAGI before IRMAA is calculated for 2026. Source: CMS 2026 Medicare Parts A & B Premiums and Deductibles.

Make Your Generosity Count in 2026: Switch from Checks to QCDs

Bottom line: If you don’t itemize, checks don’t cut taxes, QCDs do. Shift gifts from your checkbook to your IRA, exclude the income “above the line,” and lower AGI, MAGI, and potential IRMAA.

Next steps:

- Confirm eligibility: Age 70½+, qualified 501(c)(3), direct transfer only. The 2026 annual QCD limit is $111,000 per person ($222,000 for married couples filing jointly).

- Sequence correctly: Do QCDs before any taxable RMDs each year.

- Call your custodian: Set up the payee and send funds directly to the charity.

- Document it: Keep the charity receipt; report the 1099‑R with QCD notation at tax time.

Michael Ryan Pro tips:

- Annual timing: Initiate by early December to hit the 12/31 cutoff.

- Coordinate: Map QCD amounts to IRMAA brackets and your RMD.

- Mix strategies: Use QCDs for recurring gifts; use appreciated securities in years you’ll itemize.

- One move, two wins: satisfy RMDs and keep premiums and taxes in check.

Note: This content is for informational and educational purposes only and should not be considered financial, legal, or tax advice. Please consult a qualified professional for guidance specific to your situation.