You deposited a check and now you’re hitting ‘refresh’ on your banking app every five minutes? That frustrating gap between seeing a check in your ledger balance and having the funds in your available balance is a universal source of financial anxiety.

So, how long does it take for a check deposit to clear?

As a financial planner for nearly 30 years, I’ve helped thousands of clients navigate the “Clearinghouse Gap.”

I’m not just going to give you a generic two-day timeline. I’m going to pull back the curtain on the Expedited Funds Availability Act (EFAA) and show you why “available” money is often a dangerous illusion.

💡 The “48-Hour Rule” Explained Simply

For most standard U.S. checks, your money moves on a federal Regulation CC clock:

- • Next Business Day: The first $225 of your deposit is legally required to be available.

- • Second Business Day: The remaining balance is typically released to your account.

- • High-Trust Checks: Treasury or Cashier’s checks usually clear in one business day.

⚠️ The Planner’s Warning: “Available” funds are NOT “Cleared” funds. Banks front you the money as a courtesy while the MICR line is verified. If the check bounces on day 5, the bank will claw that money back.

Keep reading to find the 7 Red Flags that trigger an automatic 7-day hold on your cash.

💡 Michael Ryan Money Tip: The Quick Answer You’re Looking For

For most standard U.S. checks, you can expect the following:

- Next Business Day: The first $225 of your deposit should be available.

- Second Business Day: The remaining amount of the check is typically made available.

However, this timeline can change.

Factors like the check amount, your account history, and the type of check can lead to longer holds. Keep reading to understand why these delays happen and how to protect yourself.

Key Takeaways Ahead

Now, try searching for: Regulation CC hold times, Mobile deposit limits 2026, or Bounced check fees.

The Funds Availability Illusion: Why “Available” Isn’t “Cleared”

Here is the real deal: A check is not money. It is a legal instrument. A promise of payment.

When you deposit a check, your bank is essentially fronting you the cash on good faith while the MICR line (the magnetic ink numbers at the bottom) is routed through the Federal Reserve Bank (FRB) system to the Drawee Bank (the bank the money comes from).

This system is governed by Regulation CC (Reg CC). It forces banks to give you access to your money quickly, but it does not guarantee the check is good.

- The $225 Rule: Reg CC mandates that the first $225 of most deposits must be available by the next business day. [cite: Federal Reserve Board, Jan 2026]

- Check 21 Impact: The Check Clearing for the 21st Century Act allows banks to use digital images, but “Settlement” still happens in overnight batches.

- The Return Path: An issuing bank has a legal window to “Return” a check for Non-Sufficient Funds (NSF) even after the money appears in your account.

Check Clearing for the 21st Century Act

The Official Check Clearing Timeline (Reg CC Standards)

The “Standard Clearing Window” is determined by the level of risk the bank associates with the Payee and the Testator of the check.

- Next Business Day: Typically applies to high-trust instruments like U.S. Treasury checks, Cashier’s checks, and Postal Money Orders.

- Second Business Day: The standard for local Personal/Business checks. If you deposit $1,000 on Tuesday, the first $225 is available Wednesday, and the remaining $775 is available Thursday.

- The “Shadow Hold”: If you deposit after the bank’s Cutoff Time (often 2:00 PM for Mobile Check Deposits), the clock doesn’t start until the following business day.

<div class=”callout-box resource”>

<strong>💡 Advisor Tip: The Weekend Trap</strong>

<p>Banks only count <strong>Business Days</strong> (Monday-Friday, excluding Federal holidays). If you deposit a check at 4:00 PM on a Friday, your bank doesn’t even “see” it until Monday morning. That two-day wait just became a five-day ordeal.</p>

</div>

Available vs. Cleared: The $10,000 “Aha!” Moment

This is the most misunderstood concept in modern banking. Available balance is what the bank lets you spend. Cleared funds (Settlement) is when the money has actually moved from the Drawee Bank to your bank.

I had a client, a freelance graphic designer, who deposited a $10,000 check on a Tuesday.

By Thursday, the bank made the funds “available.” She used the money to pay her estimated quarterly taxes.

On Monday, the check “Returned” because the client’s account was fraudulent.

The Result: The bank clawed back the $10,000, her tax payment bounced, and she was hit with Overdraft Fees. This taught her the “Golden Rule” of banking: Never spend large, non-routine deposits until you’ve waited 5-7 business days for the settlement cycle to close.

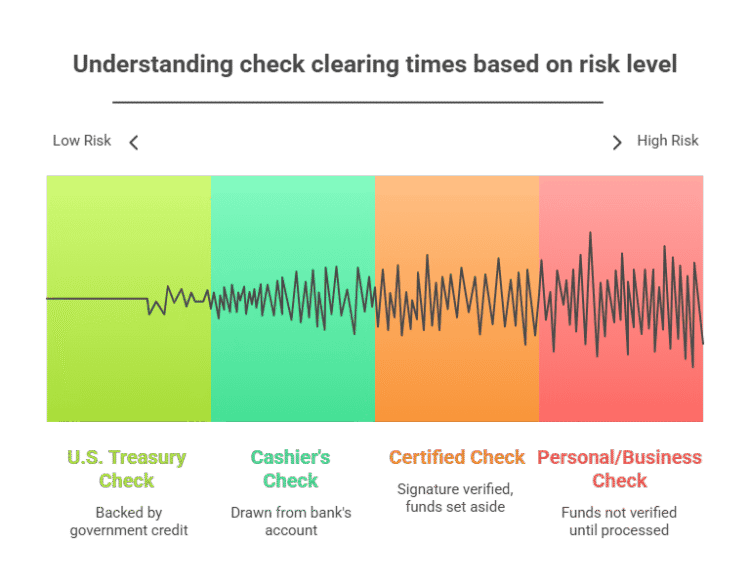

U.S. Treasury Check

Clears: Next Business Day

Why? Backed by the U.S. government. The lowest risk possible.

Cashier’s Check

Clears: Next Business Day

Why? Funds are drawn from the bank’s own account. The bank has already verified the funds exist.

Certified Check

Clears: 1-2 Business Days

Why? The bank has certified the payer’s signature and that funds were set aside from their account.

Personal/Business Check

Clears: 1-2 Business Days (Standard)

Why? A promise from an individual or company. Funds are not verified until processed. Highest risk.

💡 Avoid Bounced Checks & Bank Traps

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Spot automated "shadow holds" early

- → Master the federal $225 rule

- → Sidestep $10k overdraft disasters

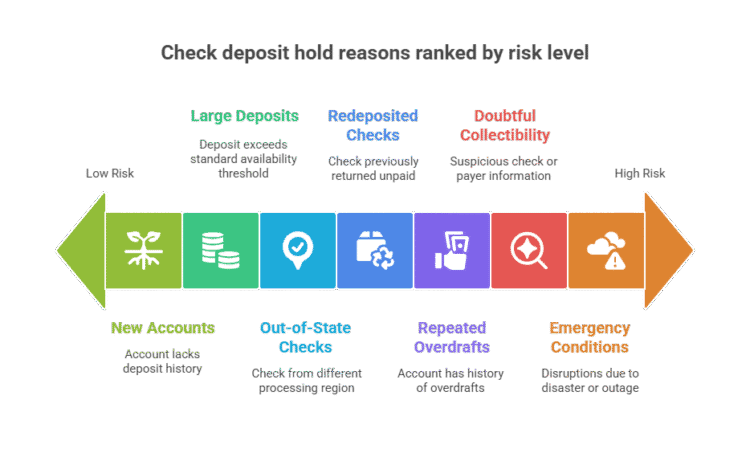

7 "Exception Holds" That Trigger a 7-Day Wait

Under Regulation CC, banks have the legal right to place an "Extended Hold" (usually 7 business days) if they flag one of these Red Flags:

Use this red flag table to understand when banks may extend check holds under Regulation CC exceptions, especially for large deposits, new accounts, repeated overdrafts, and out-of-country items. It highlights common technical triggers and why they happen, so you can anticipate delays and avoid liquidity surprises on significant check deposits.

| Red Flag | Technical Trigger | Why It Happens |

|---|---|---|

| Large Deposit | Amounts over $5,525 | Triggers a manual liquidity review because Regulation CC allows extended holds on large deposits above this threshold. |

| New Account | Open < 30 days | No “history of trust” exists yet, so banks can place longer exception holds on check deposits into new accounts. |

| Repeated Overdrafts | 6+ NSF events in 6 months | The account qualifies as “repeatedly overdrawn,” so the bank treats you as a high-risk endorser and may extend holds. |

| Redeposited Check | Previous “return” flag | A prior unpaid return creates a higher probability of a second NSF event, so banks use the redeposited-check exception. |

| Doubtful Collectibility | MICR mismatch or stale date | Anomalies in the check image give the bank reasonable cause to doubt collectibility under Regulation CC. |

| Emergency Conditions | Fed system outages | Natural disasters, communication failures, or cyber-attacks can legally justify longer check holds until systems recover. |

| Out-of-Country | Non-U.S. drawee bank | Foreign checks must clear through an international clearinghouse, which is slower and increases the risk of nonpayment. |

Review these red flags before depositing large or unusual checks so you can plan your cash flow, ask better questions at the branch, and avoid unexpected multi-day holds on critical funds.

The Hierarchy of Trust: Check Types Ranked by Speed

Not all Instruments are cleared equally. Your bank uses a risk-weighted model to determine how much of your "Available Balance" they are willing to risk.

1. The Gold Standard (Next Day)

- U.S. Treasury Checks: Backed by the full faith of the government.

- Cashier's Checks: Drawn on the bank's own ledger.

- Federal Reserve Bank Checks: Zero-risk settlement.

2. High Trust (1-2 Days)

- Certified Checks: The bank has already "Certified" that the funds are set aside.

- Direct Deposit (ACH): Moves through the Automated Clearing House with pre-verified data.

▶ What about a direct deposit? You can read more about direct deposit in my recent article Why Is My Direct Deposit Late?

Deposit Method

- In-Person with a Teller:

This is often the fastest. A teller can sometimes spot issues with a check immediately. - ATM:

These deposits are generally reliable, but be very aware of the ATM's cutoff time for same-day processing. - Mobile Check Deposit:

Incredibly convenient, but subject to strict cutoff times and deposit limits. You simply endorse the check, open your mobile banking app, and take pictures of the front and back. The check image is then sent for processing. You can learn more about this in our guide to Chase Mobile Check Deposits.

If you are looking for info on specific banks:

- Bank of America Cutoff and Check Clearing Policy

- Wells Fargo Check Clearing Policy and FAQs

- Chase Bank Check Clearing Time

- Funds Availability at Citi Bank

- Venmo Payment Not Showing Up In Bank Account

- Chime Direct Deposi

3. High Risk (2-7 Days)

- Personal/Business Checks: A simple promise from one person to another.

- Money Orders (Non-Postal): Can be easily altered or forged.

- Starter Checks: No printed name/address often triggers Doubtful Collectibility algorithms.

[check_parts_explorer]

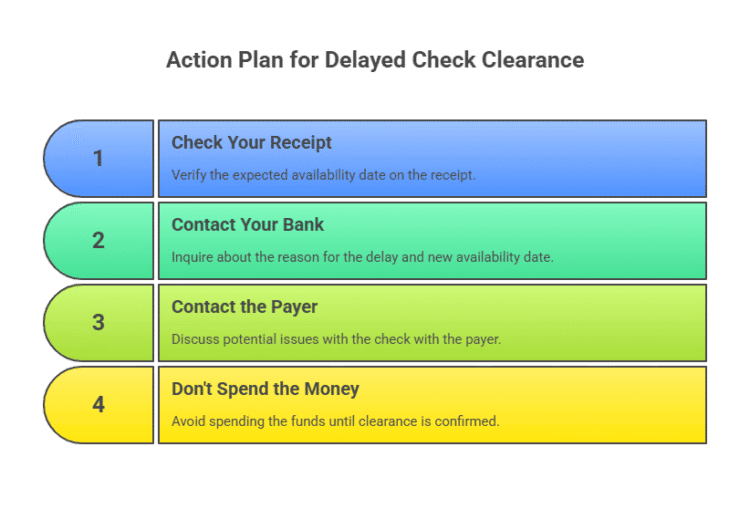

What to Do If Your Check is Held Too Long

If your deposit is stuck in "Pending" purgatory, follow this 3-P Viability Protocol:

- Paperwork: Check your Deposit Receipt. Does it state a "Funds Availability Date"? If so, the bank has likely applied a Regulation CC Exception Hold.

- Phone: Call the Operations Department (not just a teller). Ask if there is a MICR line error or an issue with the Indorsement.

- Payer: Contact the person who wrote the check. Ask them to confirm with their bank that the funds have been "Debited" from their account.

In 2026, the speed of banking is a paradox. Your phone captures the image in a second, but the Clearinghouse Interbank Payments System (CHIPS) and the Federal Reserve still operate on a legacy batch-processing schedule.

Don't let "Available Funds" trick you into spending money that hasn't fully Settled. Protect your Ledger Balance by treating every large check as a 7-day commitment.

What This Means for You

If you need cash immediately:

Always deposit in-person with a teller and ask for an "Immediate Availability" override.

If you are a business owner:

Switch to ACH Transfers or Zelle for any payment over $5,000. These bypass the Reg CC hold cycle entirely. [See: Why Is My Direct Deposit Late?]

💡 Avoid Bounced Checks & Bank Traps

One clear financial move each week — straight from 28 years of seeing what goes wrong.

- → Spot automated "shadow holds" early

- → Master the federal $225 rule

- → Sidestep $10k overdraft disasters

Frequently Asked Questions

Can a bank hold a check longer than 7 days?

Yes, in "Emergency Conditions" or if the bank can prove a high probability of fraud. However, they must provide you with a written Hold Notice explaining the reason.

Why did my bank only give me $225?

This is the Reg CC Next-Day Availability requirement. The bank is fulfilling their legal minimum while they wait for the remaining funds to settle through the clearinghouse.

Does mobile deposit take longer than an ATM?

Often, yes. Mobile apps use automated Optical Character Recognition (OCR). If the lighting is poor or the MICR numbers are blurry, the check is diverted for human review, adding 24-48 hours. [See: Chase Mobile Check Deposits Guide]

What happens if I spend a check that later bounces?

You are legally responsible. The bank will reverse the deposit, and if your balance goes negative, you will be hit with an unpaid item fee and potential overdraft charges.

The Bottom Line on Check Clearing

Here is the deal: Available funds are a customer service feature, not a legal guarantee. Under the Expedited Funds Availability Act (EFAA), your bank is required to give you access to your money, but they are essentially giving you an unsecured loan while the MICR data settles in the background. If you spend "Available" money on a Tuesday and the check "Returns" on a Friday, you are the one left holding the bill.

In 2026, don’t let the speed of a mobile check deposit fool you. Your phone captures the image in a second, but the Federal Reserve's batch-processing system still moves at a legacy pace. Protect your ledger balance by treating every non-routine check as a 7-day commitment.

What This Means for You

- If you’re living paycheck to paycheck: Never spend a deposited check to cover a critical bill (like rent or a car payment) until at least three business days have passed.

- If you’re a business owner: The $5,525 "Large Deposit" threshold is your primary enemy. If you receive a payment larger than this, expect a 7-day hold and plan your payroll accordingly.

- If you need immediate cash: Always deposit in-person with a teller. Automated systems (ATM and Mobile) are significantly more likely to trigger Doubtful Collectibility algorithms.

Next Steps

- Check your receipt immediately: Look for the "Scheduled Availability Date." This is your only official notice of a Regulation CC Exception Hold.

- Verify the "Return Window": For checks over $10,000, call your bank's operations department on Day 4 to confirm the Final Settlement has occurred.

- Upgrade your payment tech: If you’re tired of the "Clearinghouse Gap," switch to direct deposit (ACH) or Zelle for high-value transfers. These bypass the paper check hold cycle entirely.

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.