Closing a joint bank account should be simple, but it rarely is. It’s an act tangled up in emotion, trust, and fear. In my nearly 30 years as a financial planner, I’ve seen joint accounts become a major source of conflict during divorces, business breakups, and family disputes.

I once helped a client untangle a joint business account where her ex-partner was deliberately over drafting it to cause her financial pain. She needed a clear, legal path to protect herself. And she needed it fast.

This isn’t just a “how-to” guide. This is a playbook for your financial self-defense, which I call The Michael Ryan Money Financial Decoupling Framework:

- Secure Your Exit

- Detangle the Connections

- Execute the Closure

- Verify the Separation.

We’ll cover the standard process of closing joint bank accounts. But more importantly, we’ll also tackle the difficult scenarios:

- What to do when the other person is uncooperative

- How to understand your legal responsibilities

- And the immediate steps you can take to protect the funds in the account today.

The Hard Truth: You Usually Can’t Just ‘Remove a Name’ From a Joint bank Account

Let’s debunk the biggest myth right away. In my nearly three decades as a financial planner, I’ve seen dozens of clients cling to the hope that they can just ‘remove a name‘ from a joint account.

I had a case in late 2023 where a client spent weeks arguing with her bank, believing she could edit the account like a social media profile. It’s a dead end.

A joint bank account is a rigid legal contract. Cemented by a signature card.

I predict that by 2027, biometric identity verification might make ‘ownership transfers‘ possible. But today, in 2025, it’s a fantasy. The only real path forward is total account closure.

Why are you trying to patch a sinking ship instead of getting into a new one?

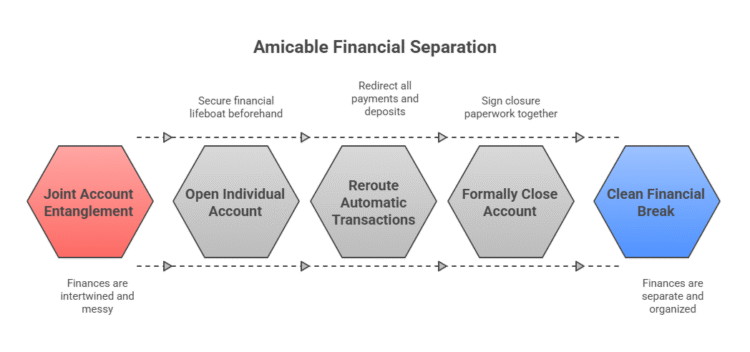

The Standard Solution: The Financial Decoupling Framework

This is the ideal path—the amicable separation. It requires communication and cooperation. Follow these steps precisely for a clean break.

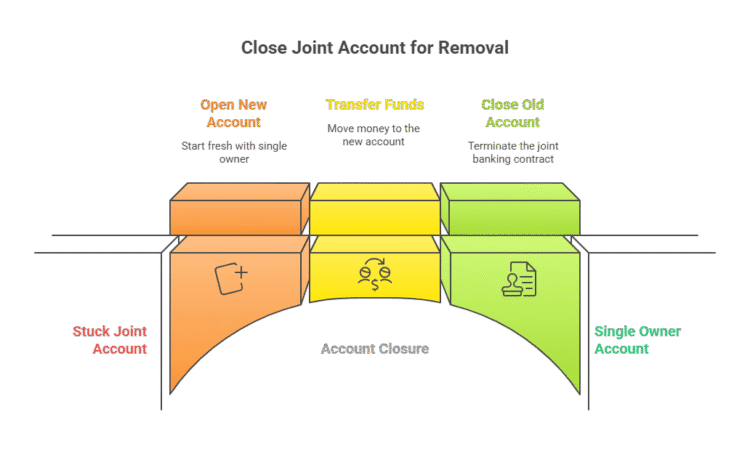

Step 1: Secure Your Exit (Open a New Account FIRST)

This is non-negotiable. Before you even mention closing the joint account, secure your own financial lifeboat. Go to your bank or a new one and open a new, individual checking account. This ensures you have a safe place to transfer your portion of the funds and a new account number to redirect your paycheck and other direct deposits without any interruption. This is a foundational step in our guide to getting your personal finances in order.

Step 2: Detangle the Connections (Reroute Automatic Transactions)

Create a list of every automatic bank payment and direct deposit linked to the jointly owned account. This includes:

- Direct Deposits: Your paycheck, Social Security benefits, or any other income.

- Automatic Withdrawals: Mortgage/rent, utility bills, insurance premiums, credit card payments, and subscriptions (Netflix, Spotify, etc.).

Redirect all of these to your new individual account. This step is critical to prevent bounced payments or accidental overdrafts on the joint account, which you are still legally responsible for.

Step 3: Execute the Closure (Agree on Funds & Formally Close)

With the balance at zero, it’s time for the final step. A step that often feels needlessly archaic.

As of my last major bank policy review in Q2 2025, most institutions still demand that all parties sign a physical closure form, often requiring notarization. This isn’t just policy; it’s a liability shield for the bank.

I had a client whose partner was overseas; we had to navigate the complex world of embassy notarization. A process that took three weeks and cost over $100. Don’t just assume you can walk in; call your branch and ask for the specific name of their ‘Account Closure Form’ and their exact signature requirements.

Are they living in the digital age, or are you going to need to find a notary public?

If you are more of a visual or audio learner, watch the below YouTube video on closing jointly owned accounts name removal.

The Difficult Scenario: What If a Partner Is Uncooperative?

The moment your account co-owner refuses to sign, you are no longer in a customer service issue. You are now in a legal standoff.

Your first call, which you should make today, is to your bank’s fraud or disputes department, not the general helpline. Request an immediate “two-to-sign” restriction or a full account freeze. Reference the fact that the account is now ‘in dispute’. This is critical terminology.

I saw a case in 2022 where a simple freeze request was ignored. But when the client stated the account was ‘in legal dispute pending divorce,‘ the bank acted within an hour.

The next step isn’t a suggestion; it’s a requirement: engage a family law attorney. A strongly worded letter from a lawyer can often break the stalemate far faster than endless, stressful phone calls.

💡 Michael Ryan Money Tip

Even if your bank allows one person to close the account, as the CFPB notes many do, acting unilaterally can have serious legal consequences in a divorce. Freezing the account is often a safer first move than draining it.

Understanding Your Legal Liability (The Scary Part)

This is the part everyone needs to understand. When you sign that signature card for a joint account, you are typically agreeing to “joint and several liability.”

This liability also applies to accounts that are “Joint Tenants with Rights of Survivorship” (JTWROS). While that term primarily deals with what happens when one owner dies (the other inherits the funds), it doesn’t change the liability rules while both owners are alive.

Closing a Jointly Owned Bank Account: Frequently Asked Reader Questions

What if my ex refuses to sign the closure paperwork?

If the bank requires both signatures and one party refuses, you have entered a legal dispute. Your first step should be to request a freeze or “two-signature” rule on the account from the bank. Your next step is to consult with a legal professional. In some cases, a court order may be necessary to force the closure and distribute the assets.

Am I liable for overdrafts my partner creates after we’ve separated?

Yes. Until the account is formally closed, you are likely 100% responsible for any debts or overdraft fees incurred on the account, regardless of who created them. This is why swift, decisive action to freeze or close the account is crucial for your financial protection.

How do I protect the money in the account from being taken by the other person right now?

You have two main options, but both have risks. First, you can withdraw your portion of the funds (e.g., 50%), but this could be seen as improper in a legal dispute like a divorce. The safer, more legally sound option is to immediately contact the bank and request a freeze or a “two-signatures-required” flag on all transactions, which protects the funds while you determine the next steps.

Final Word from Michael Ryan Money

Untangling shared finances is always stressful, but it’s a necessary step toward financial independence and security. Remember the key principles: you must close the jointly owned bank account, not just remove a name. And you are fully liable until it’s closed.

Communicate where possible, but don’t hesitate to take protective measures like freezing the account if the situation becomes hostile. By following a clear, methodical process, you can navigate this difficult transition and protect your financial future.

What to Read Next

Closing a joint account is often the first step in a larger financial reorganization. Now that you have a plan for this account, it’s time to build your own safety net.

➡️ Read Our Guide: How to Build an Emergency Fund Fast and Why It’s Your #1 Priority

- Sharing the article with your friends on social media – and like and follow us there as well.

- Sign up for the FREE personal finance newsletter, and never miss anything again.

- Take a look around the site for other articles that you may enjoy.

Note: The content provided in this article is for informational purposes only and should not be considered as financial or legal advice. Consult with a professional advisor or accountant for personalized guidance.